The Fed will try to soothe mortgage rates after bond bloodbath 🏠📈🩸

Week Ahead

TABLE OF CONTENTS

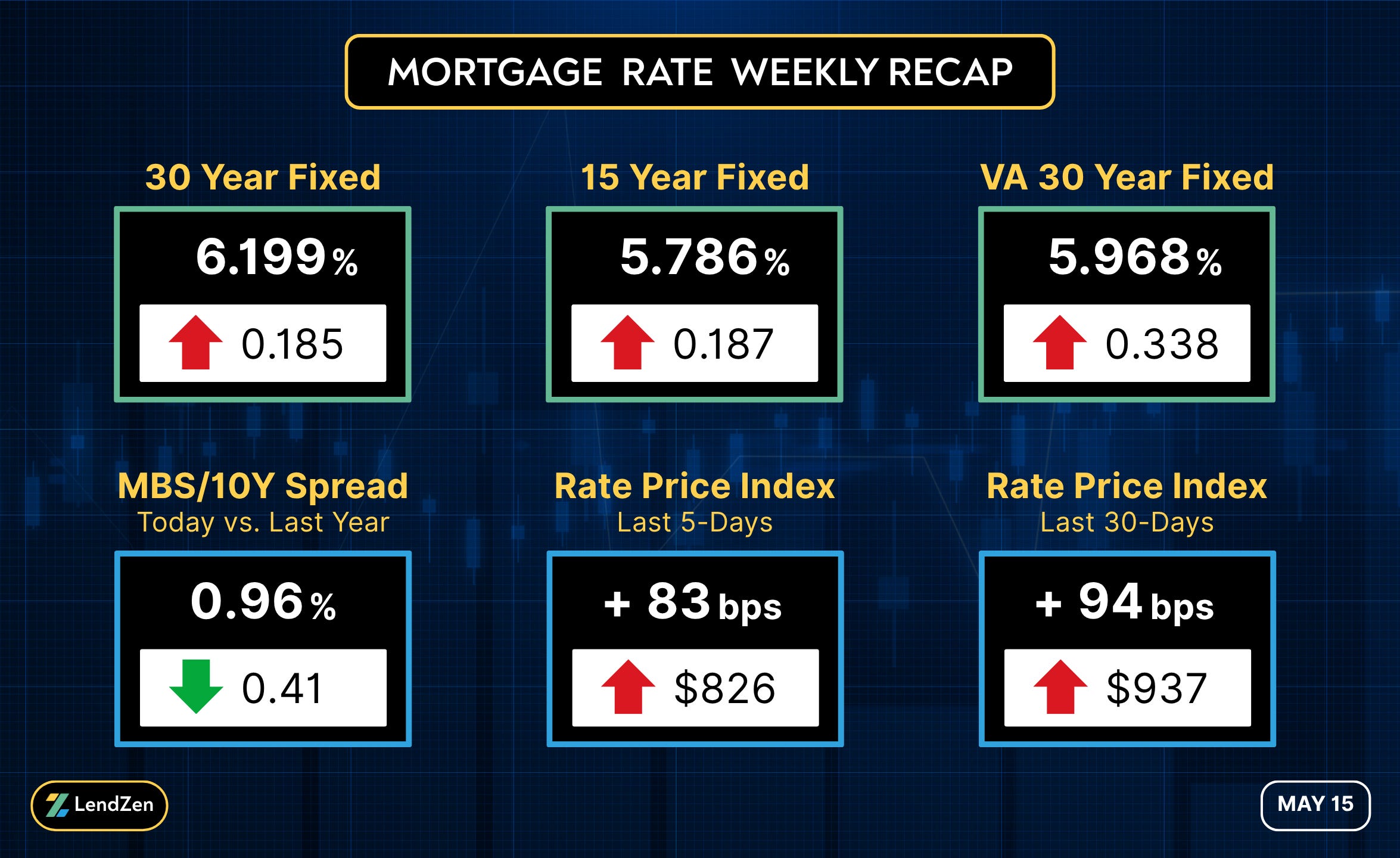

RATE RECAP ⏪

--------------

The +/- shown in the Rate Price Index represents how the pricing of mortgage rates changed during the time series.

Learn more and explore additional time series at the LendZen Index Substack.

WEEK AHEAD 🗓️

----------------

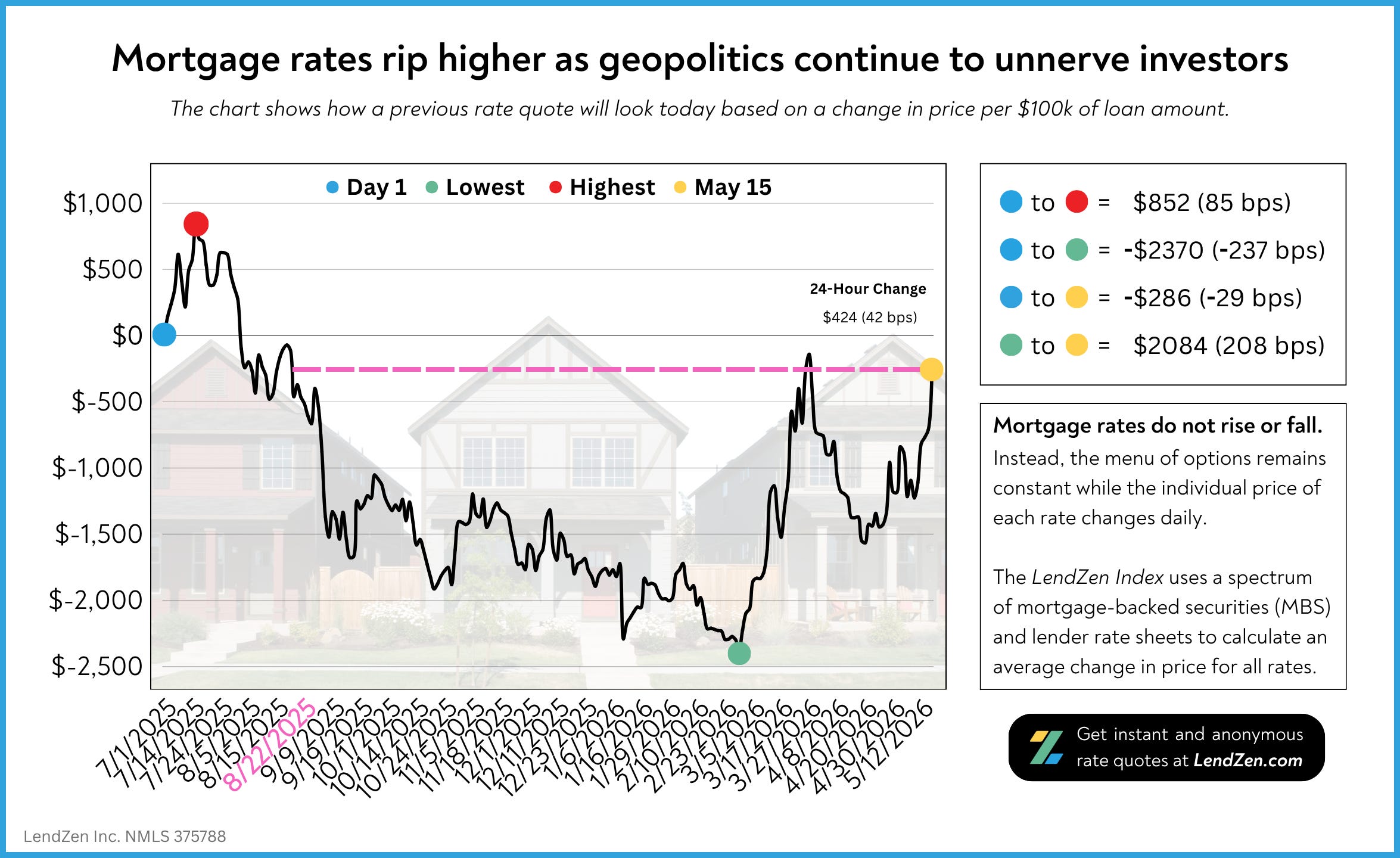

The bond market successfully navigated the previous week’s onslaught of labor market data.

The same cannot be said for this week’s inflation reports, which included hotter than expected prints in both the Producers Price Index and the Consumer Price Index.

This would have done damage on its own, but investors are showing greater fatigue when it comes to the Iran conflict.

Although the tone coming out of the meeting between Trump and Xi Jinping (China) didn’t necessarily hurt, it didn’t help either, especially after DJT sternly rejected the latest Iran peace deal.

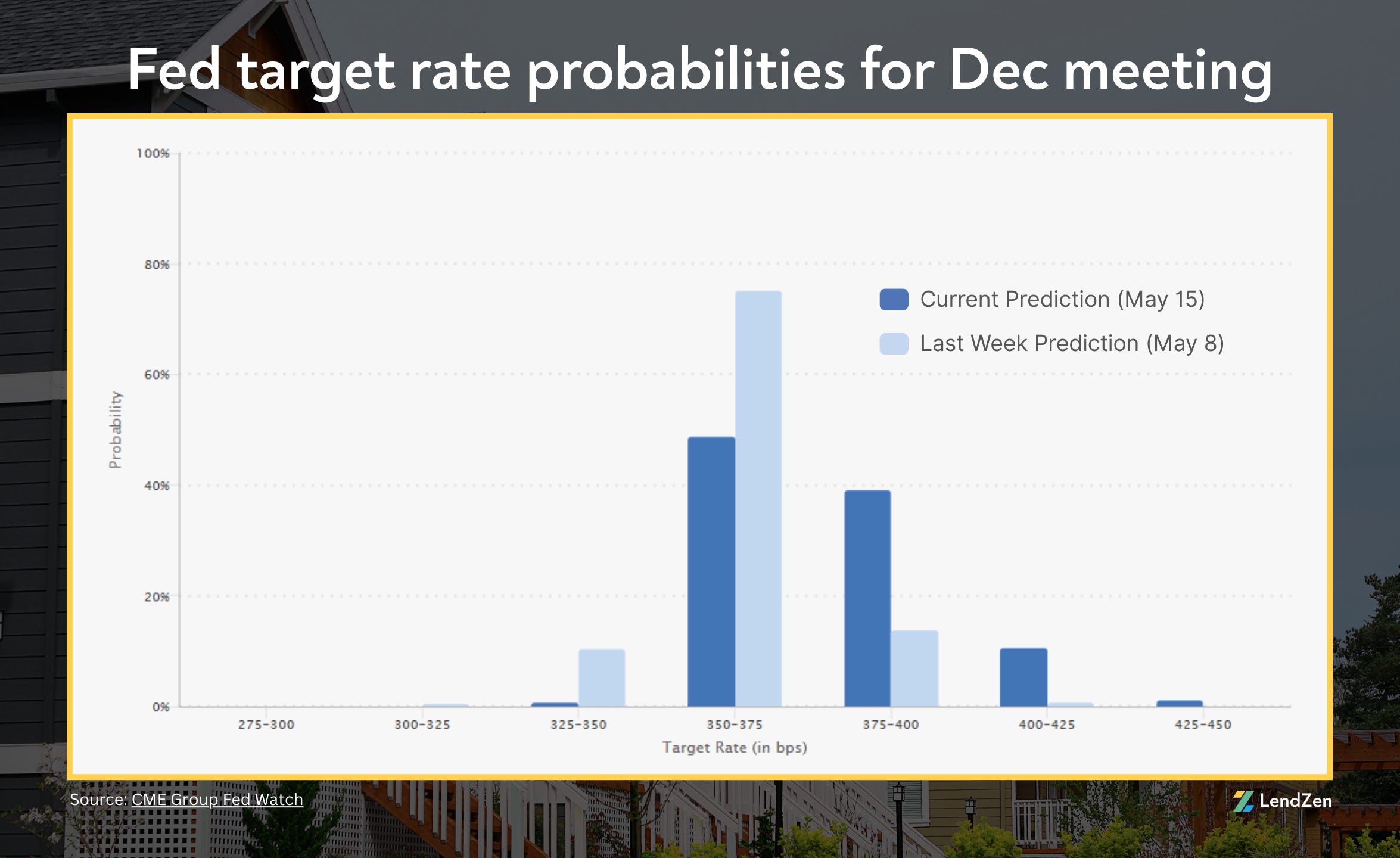

As a result, and in combination with the appointment of Kevin Warsh as the new Fed Chairmen, expectations for a Fed rate hike by the end of 2026 have surged.

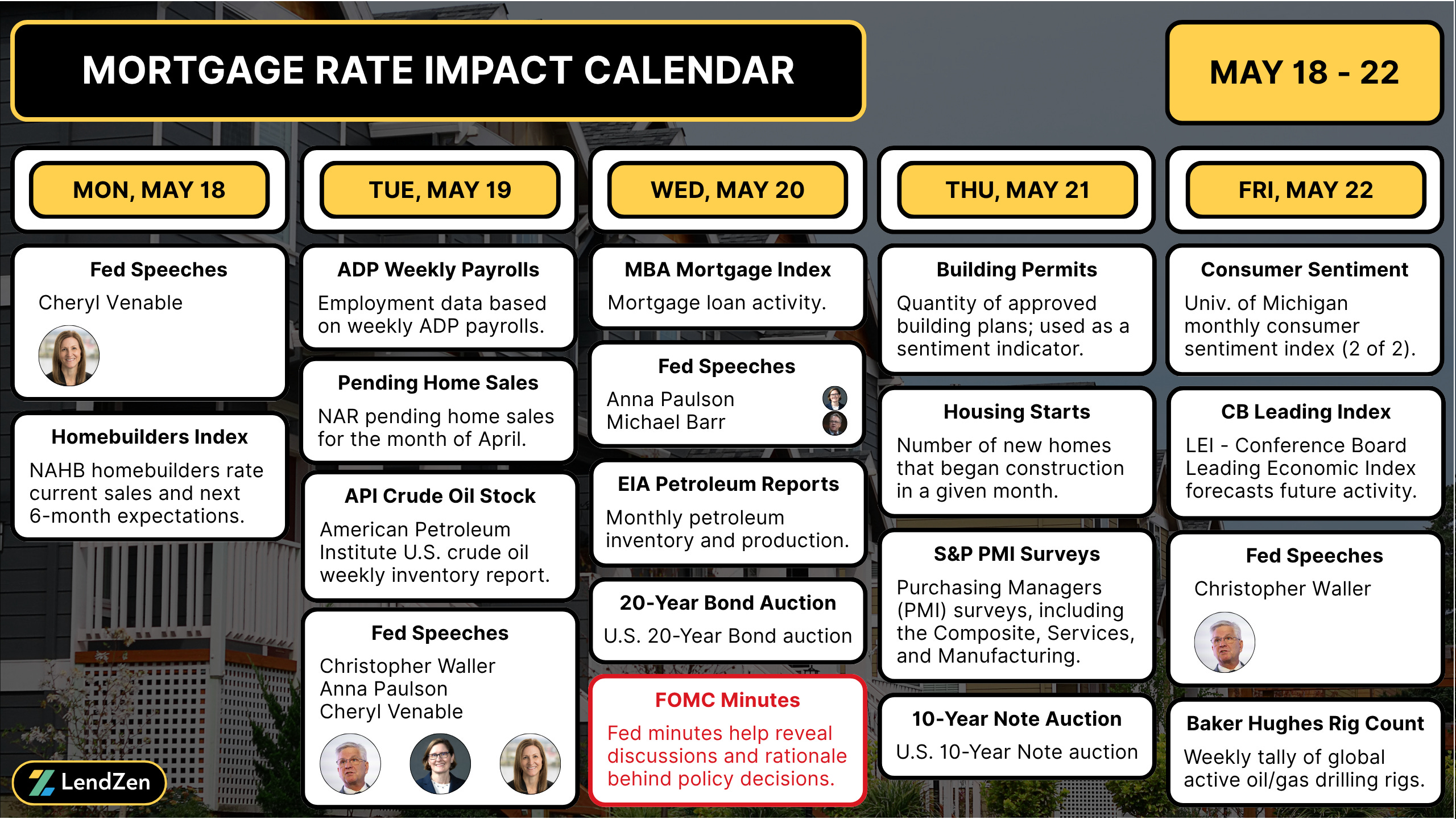

This week several Fed speakers will get a chance to jawbone bond markets back from the cliff’s edge.

Their soothing words will have to compete with housing market data, purchasing manager surveys, and their own FOMC minutes.

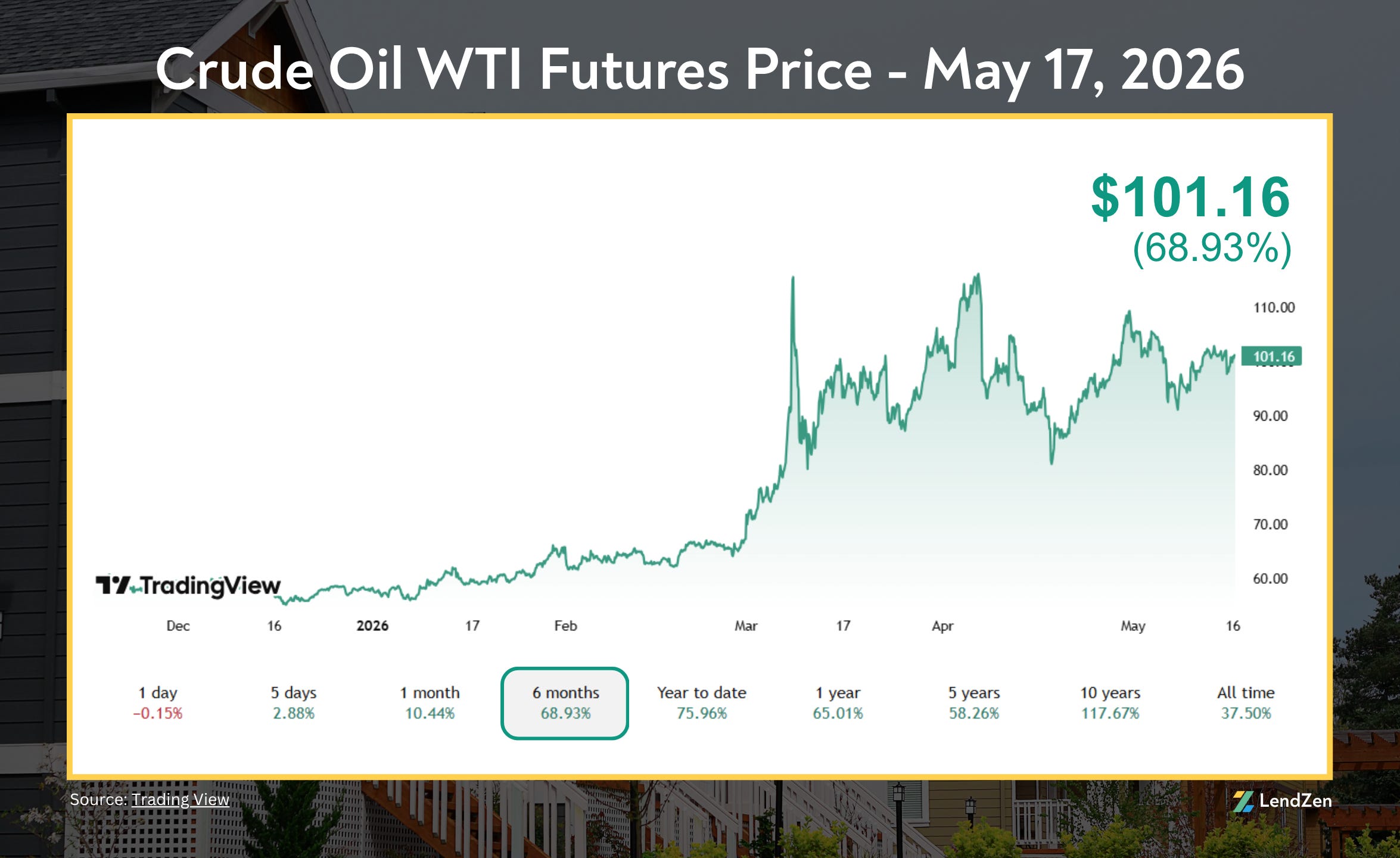

Meanwhile, the outlook for peace in the Middle East was a primary driver of the bond sell-off last week, and thus oil prices will require close attention as WTI futures remains over $100.

RATE LOCK GUIDE 🔒

---------------------

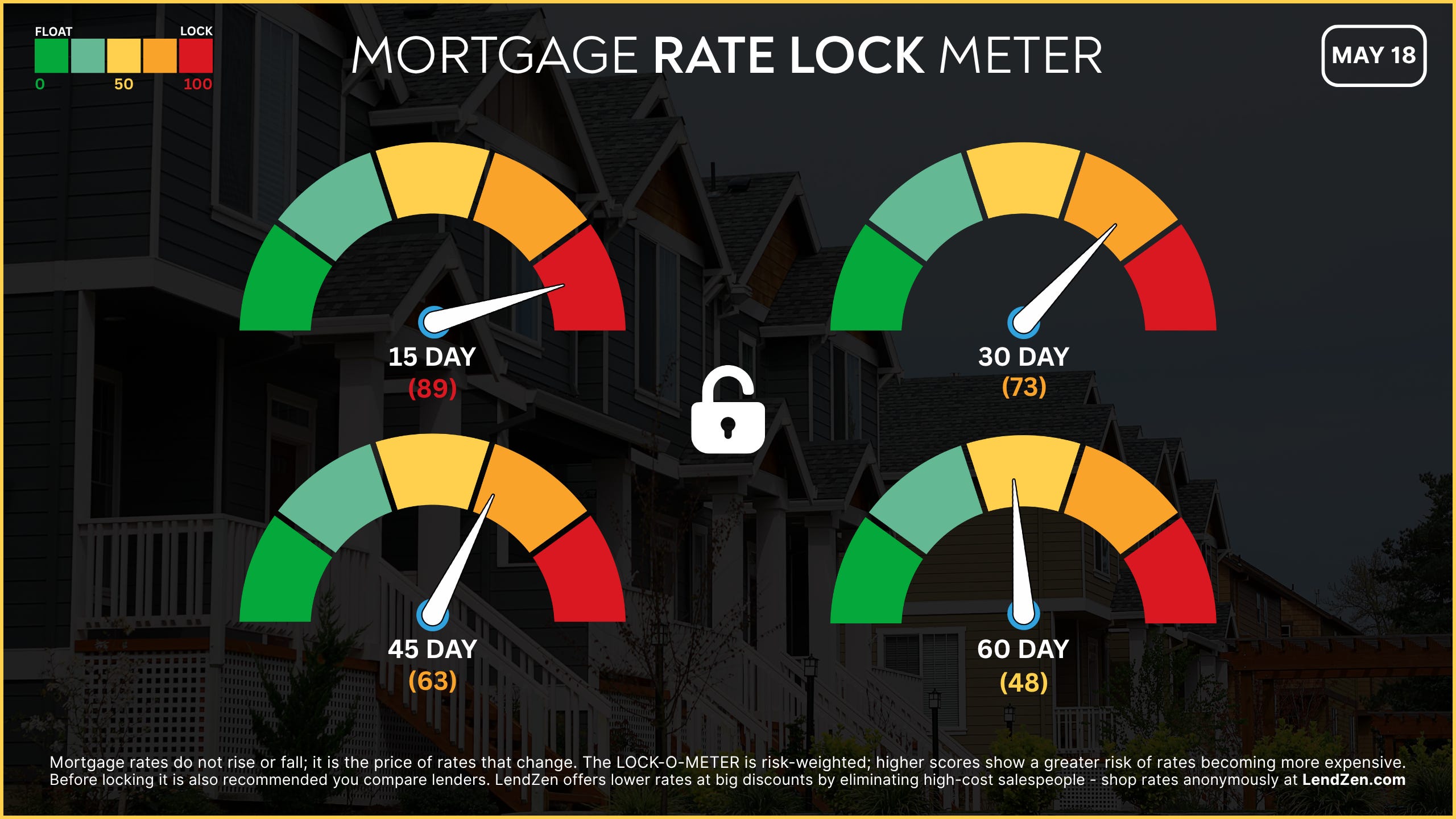

The LendZen LOCK-O-METER provides borrowers with a risk-weighted score based on how various macroeconomic events, including market data, central bank announcements, and geopolitics, each historically impacts the price of bonds.

higher risk scores = lean towards locking

------------------

Closing Window

------------------

[ 15 Days ] — 89 🔴

Mortgage rates have taken another meaningful hit from hotter inflation readings and persistent Middle East uncertainty. This week’s mix of Fed minutes, housing data, and multiple Fed speakers leaves very little room for error in the near term.

[ 30 Days ] — 73 🟠

The recent deterioration in bond prices has pushed the 30-day closing window deeper into caution territory. While there is some time to overcome the recent volatility, ongoing inflation concerns and geopolitical risks make floating feel increasingly dangerous.

[ 45 Days ] — 63 🟠

With the combination of factors outlined above, and another round of the “Big 3” (FOMC, jobs, inflation), floating risks remain elevated even for medium-term closings.

[ 60 Days ] — 48 🟡

The longer-term picture is still somewhat supportive if tensions ease, but the sharp recent reversal and inflation psychology have removed much of the previous comfort margin for floating.

If you are already in a strong position locking generally makes the most sense, especially for shorter windows, since the focus should be on making a savvy rate choice based on your longer-term rate outlook.

I expand on this “long game” approach in this Substack post.

Thanks for reading…

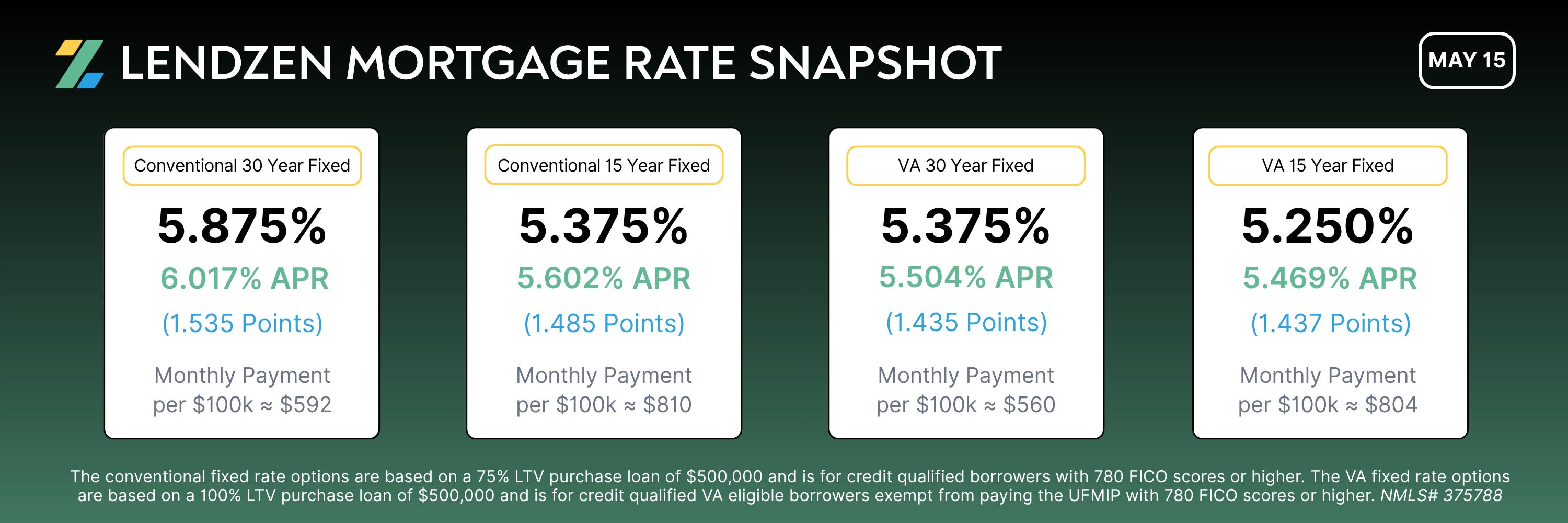

If you want to shop real-time mortgage rates and get instant qualification results without providing any contact information visit LendZen.com

The below snapshot is just a glimpse of today’s rates, but the pricing you see is exactly what you get - there are no additional lender fees or origination charges.

When you customize a rate quote on LendZen you get anonymous access to ALL AVAILABLE RATES that match your specific criteria.

Mortgage rates change daily, but on LendZen.com you can save a scenario and revisit your options anytime with one-click.

You can also request an official Loan Estimate for any loan you create.

Experience hassle-free mortgage shopping now at LendZen.com

LendZen Inc. is an equal opportunity mortgage lender, NMLS 375788