Mortgage Rate Snapshot 📷📉🏠 (FEB 13)

Included in this snapshot are the following sections:

STORYLINE 📰

-------------

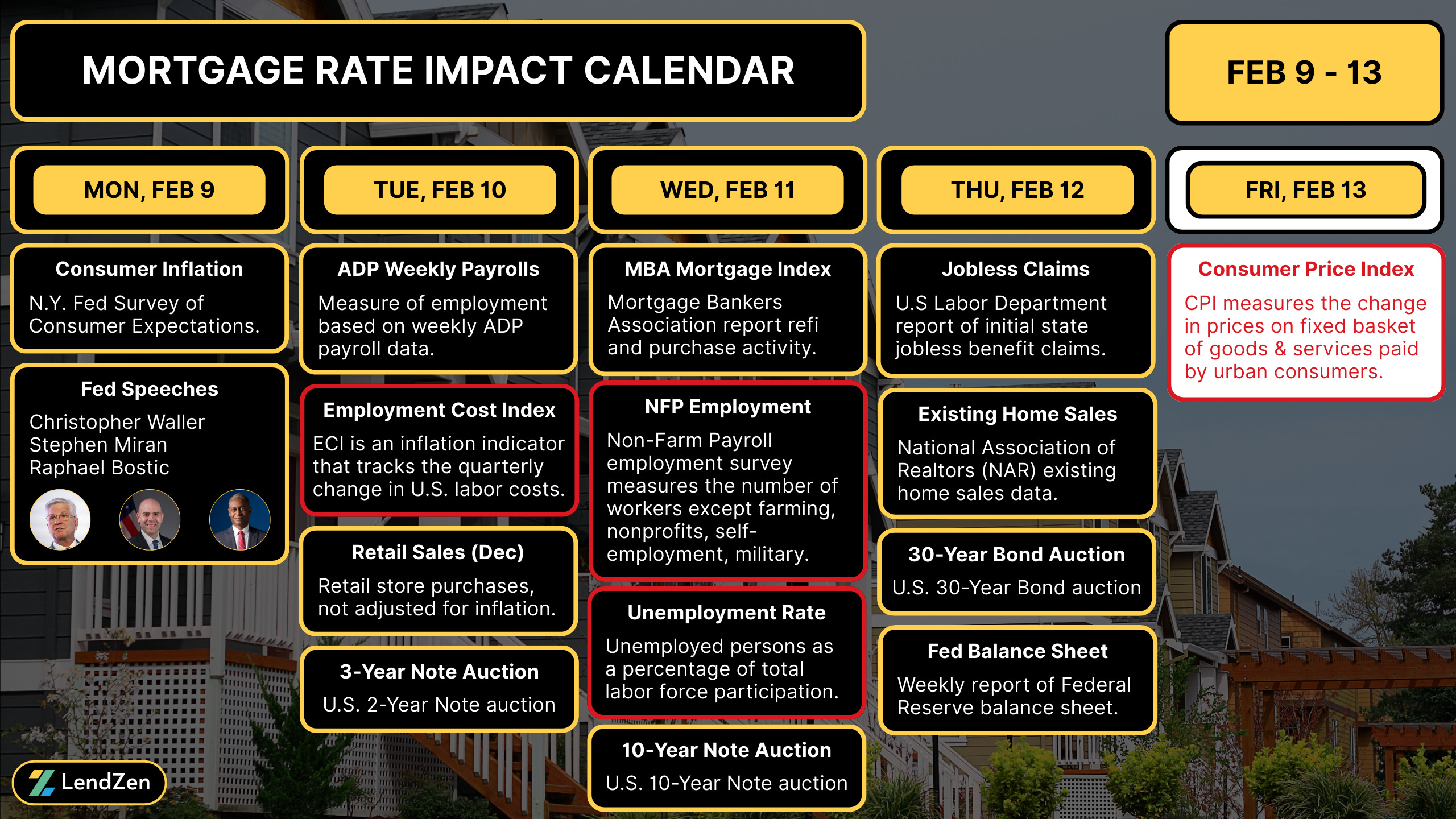

Bond markets just had a “what the heck happened” moment, which I deconstructed in yesterday’s Flash Update Substack post.

Today, all eyes will be on the CPI inflation report which is published at 8:30am EST.

That will conclude a rare week of econ data, with two major reports in one week.

If mortgage rates manage to survive this week’s nightmare, then things look promising for the rest of the month.

With no FOMC meeting in February, markets will instead focus on the Fed Minutes (Feb 18) and PCE inflation (Feb 20).

Personal Consumption Expenditures is the Fed’s preferred inflation data and is followed the last Friday of the month (Feb 27) by another inflationary gauge, Producer Price Index (PPI).

These reports are likely to follow the script from today’s CPI, so fingers crossed things go in our favor in a few hours.

RATE PRICE INDEX 📉

---------------------

Mortgage rates DO NOT rise or fall.

The full range of rates is always available, and instead the price of each rate changes based on the trading of individual mortgage bonds.

Learn how bonds influence mortgage rates in the MBS sections later in this post.

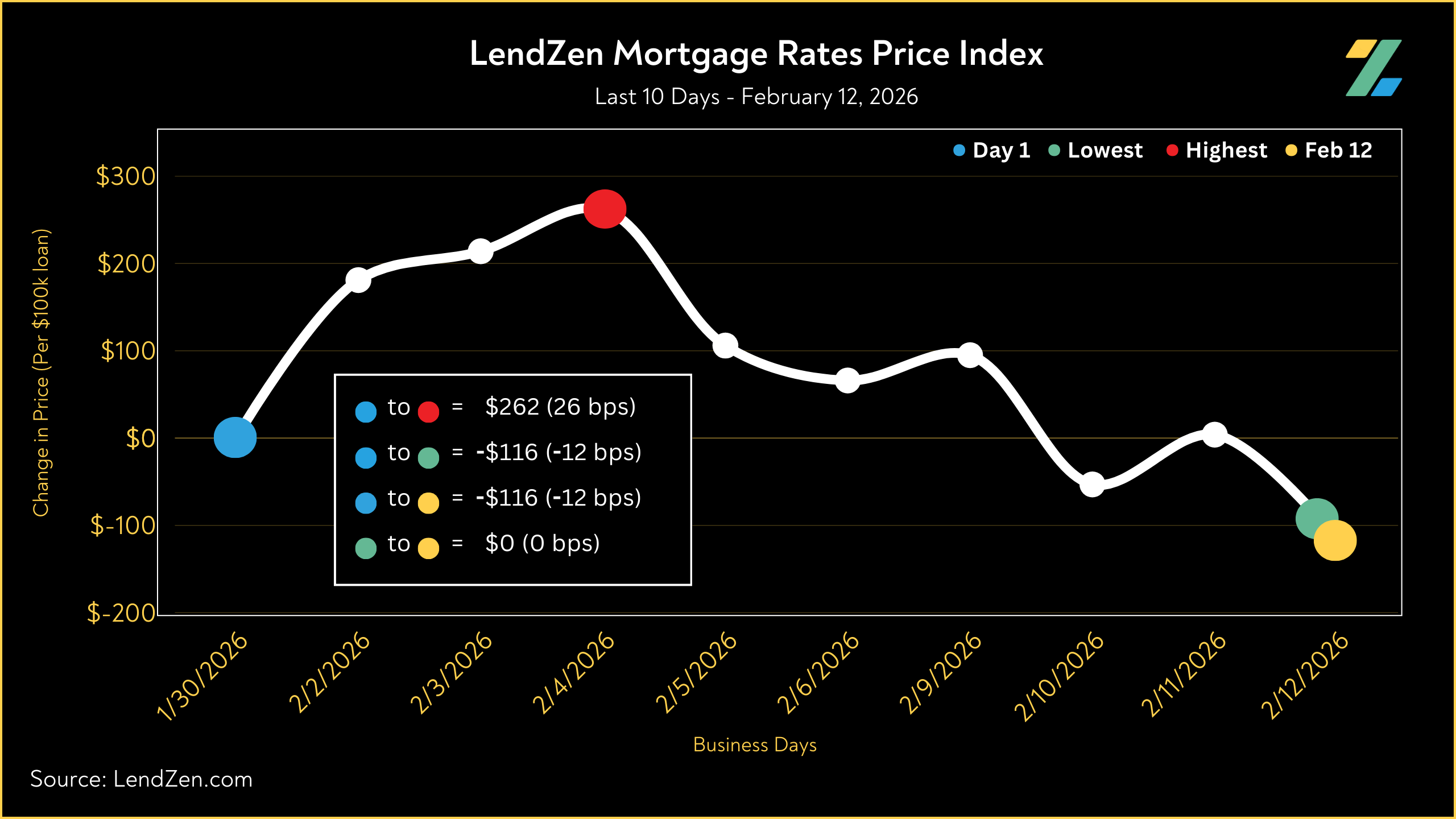

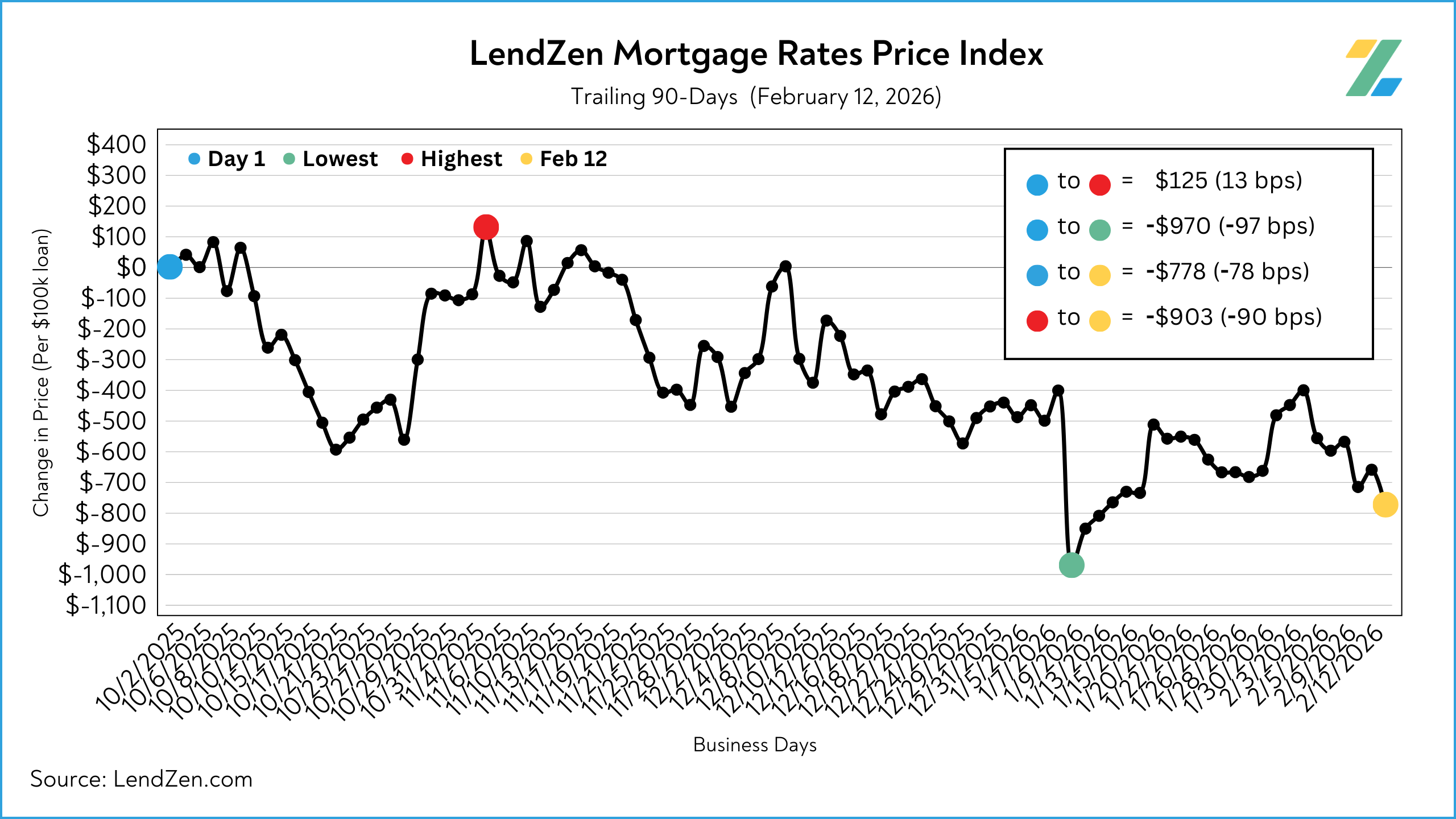

The LendZen Index calculates a daily change in the price of mortgage rates by tracking a spectrum of mortgage-backed securities (MBS).

Below are the 10-Day and 90-Day charts, but you can track the daily changes across a variety of time series at LendZen.substack.com

Mortgage rate prices have slid 78 bps lower over the past 90 days but fell as much as 90 bps from peak (11/5) to trough (1/9).

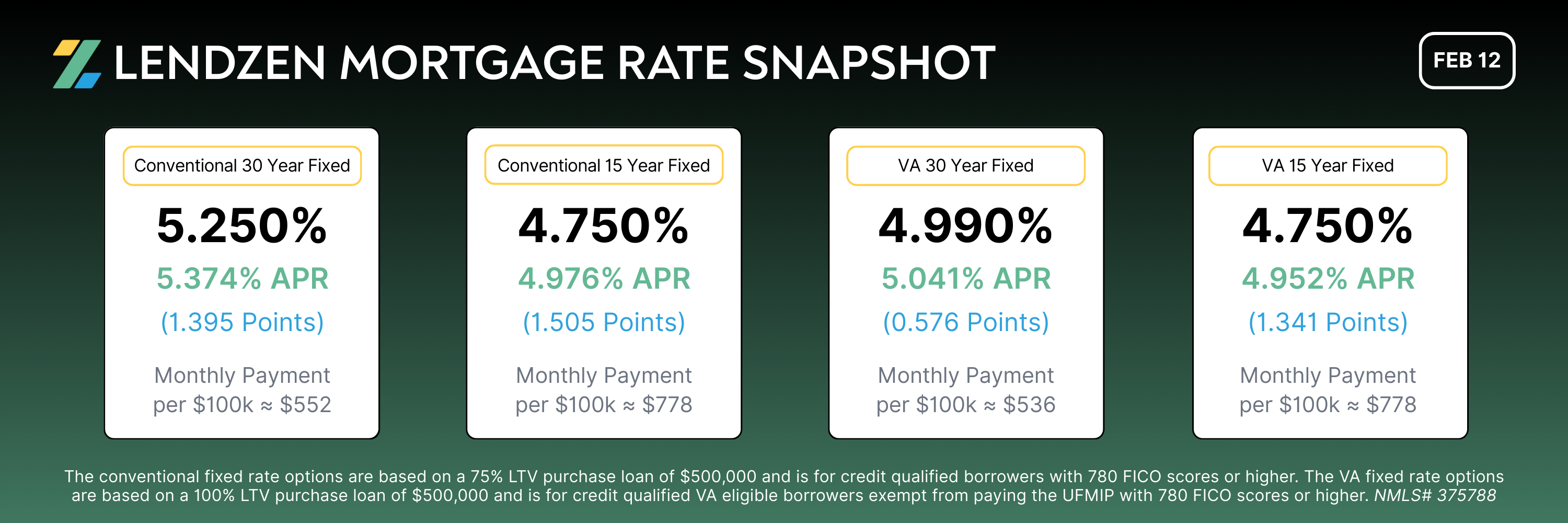

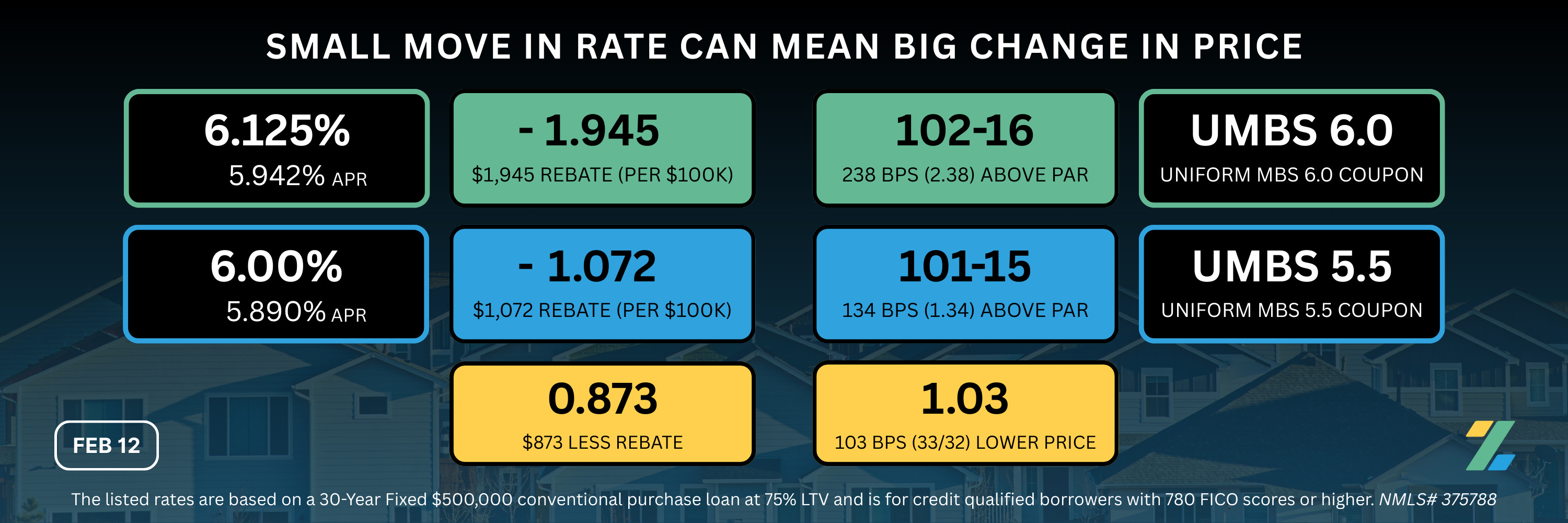

RATE SNAPSHOT 📷

-------------------

The mortgage industry thrives on a lack of pricing transparency, hence why most lenders only publish a single daily rate or nothing at all.

Fortunately, LendZen gives you anonymous access to ALL rate options that meet your criteria, with full transparency of costs upfront.

Below is a snapshot of a few different rate options available today.

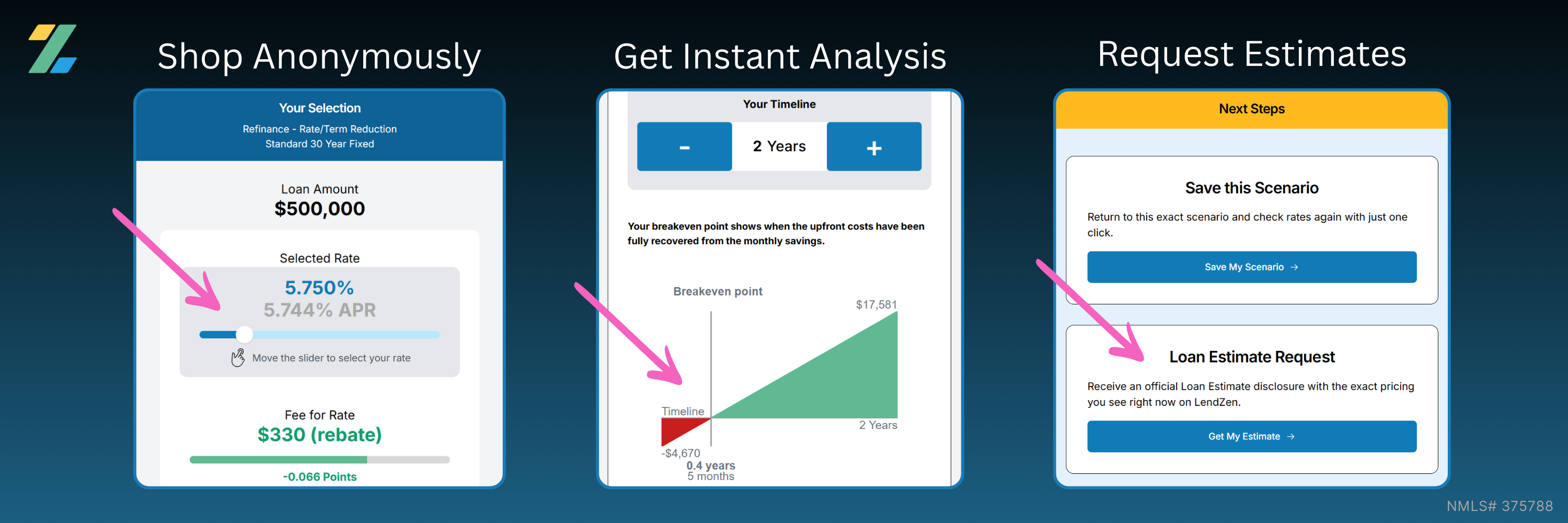

When you customize a quote on LendZen, every available rate for that program is displayed in real-time.

There is no contact information required to explore your options and results are provided instantly.

You can also request an official Loan Estimate for the exact loan you created and save your scenario to revisit your rate options daily with one-click.

See for yourself at LendZen.com

COMPARE OFFERS 🔍

---------------------

Because rates are determined by the bond market, the companies offering you a mortgage merely add their fees on top.

You are not shopping for a lender using rate alone, instead your decision should be based on total costs for the same rate (same day).

This is why it is recommended you NEVER choose a mortgage company without first comparing Loan Estimates, each with matching loan criteria.

Learn more about the LE disclosure and how to find the best deal instantly on this Substack post.

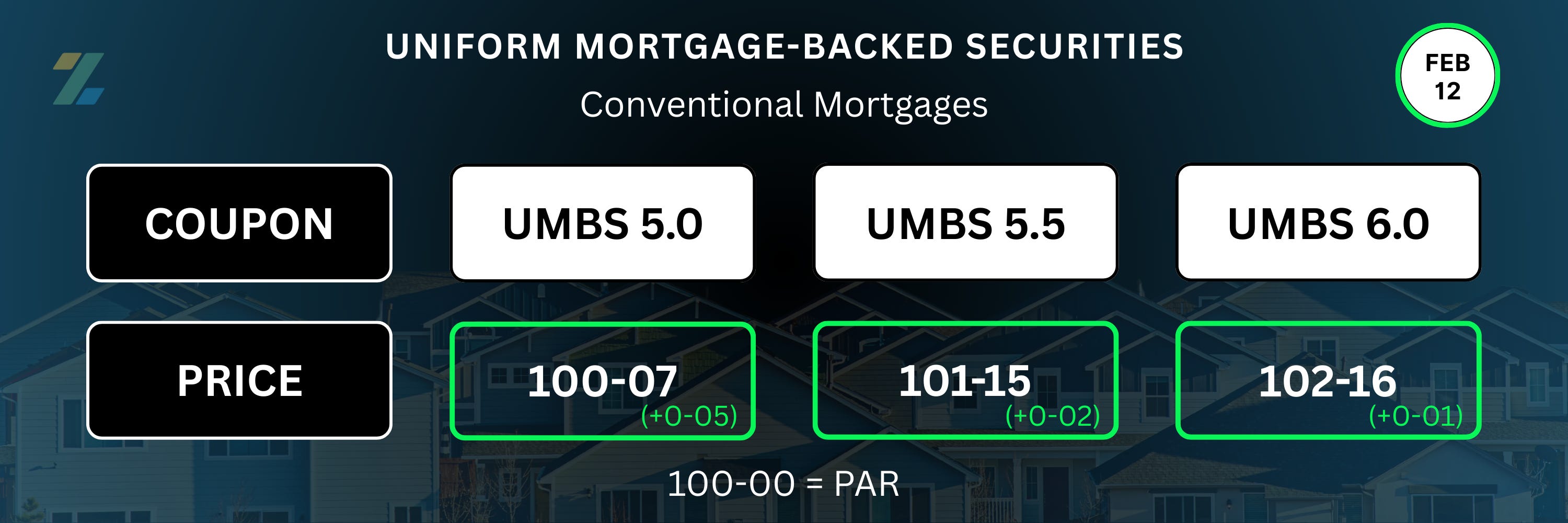

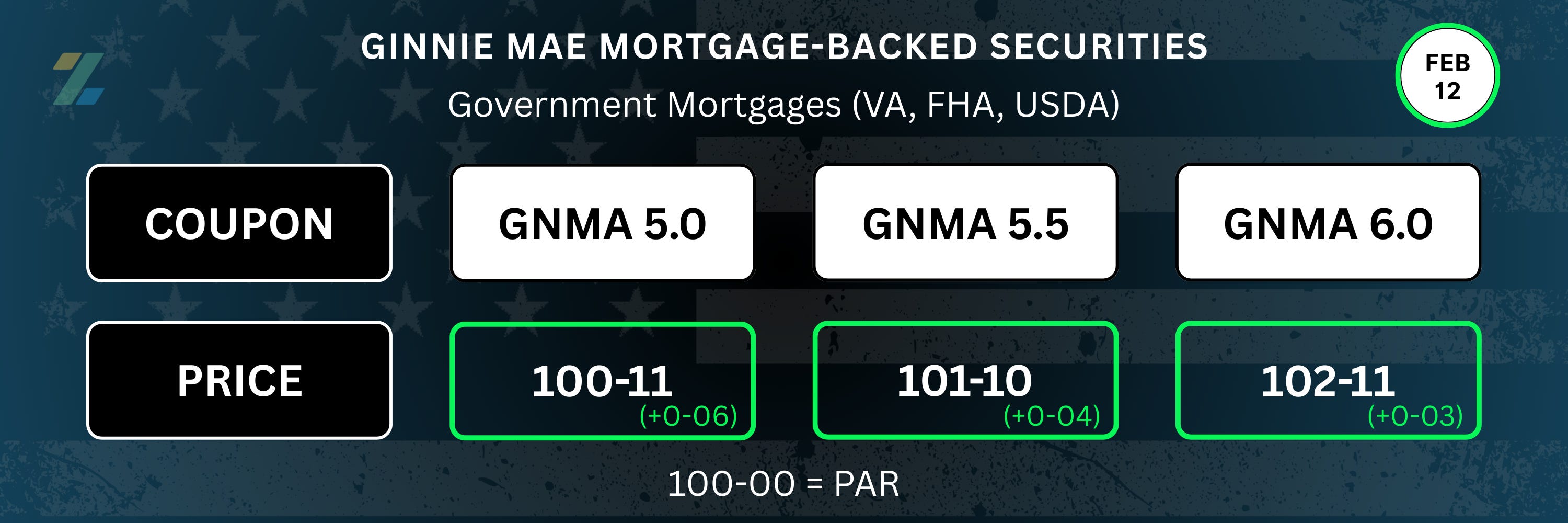

MBS PRICING 🏦

----------------

Most mortgages are sold into mortgage-backed securities (MBS) and the price of these bonds determines rates for all banks and lenders.

MBS coupons are sold at half-percent increments, while their price moves in 32nds (ticks).

100-00 acts as the starting line, also referred to as PAR.

The higher the coupon price, the less expensive the rates will be that are sold into that security.

Therefore, an increase in the price of mortgage bonds is good for mortgage rates.

Learn more about the dynamics of MBS pricing and how it impacts your mortgage options in the explainer at the bottom of this post.

MBS EXPLAINER 📖

-------------------

Mortgage rates do not rise or fall, instead the PRICE of rates change.

How much a mortgage-backed security is priced below or above par determines the “price” of the mortgage rates packaged into that MBS coupon.

For example, the higher an MBS is priced above par the less expensive the rates will be that are sold into that security. (ex. 102-00 > 101-00)

The Note rates of each mortgage sold into a specific MBS typically range between 0.125 – 0.750 above the coupon rate, depending on the loan type. (ex. 6.125% – 6.750% rates ~ 6.00 MBS)

The spread between the mortgage Note rate and the coupon rate is retained as a servicing fee (minus guarantee fees). (ex. 0.125 – 0.750)

This is why a 6.00 note rate is not sold into a 6.00 coupon and is therefore priced based on lower coupons. (ex. 6.00% rate ~ 5.50 MBS)

As a result, when comparing a X.00% rate with a X.25% rate (or a X.50% rate with a X.75% rate) the shift between different coupons can disproportionality affect the PRICE of the lower Note rate despite the close proximity of the two rates.

Thanks for reading.

If you want to shop real-time mortgage rates and get instant qualification results without providing any contact information visit LendZen.com

LendZen provides a fully automated mortgage shopping experience that gives you anonymous access to all mortgage rates with full transparency of costs upfront as bond prices change.

LendZen Inc. is an equal opportunity mortgage lender, NMLS 375788.