When to refinance and finding the best rate 🏠💰📊 (JAN 2)

Deciding when to refinance is not just about a lower rate

Included in this analysis are the following sections:

MARKET RECAP ⏪

------------------

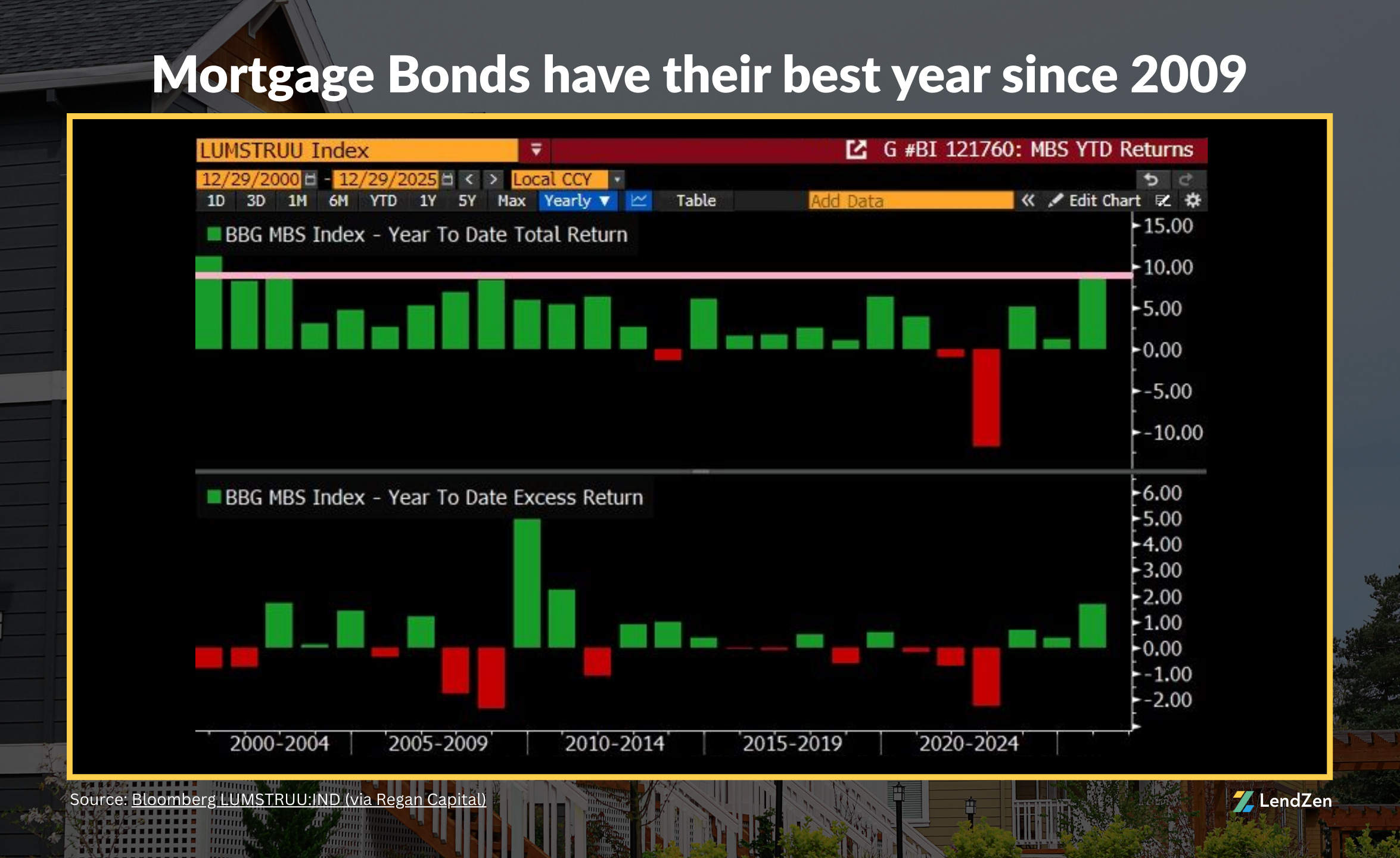

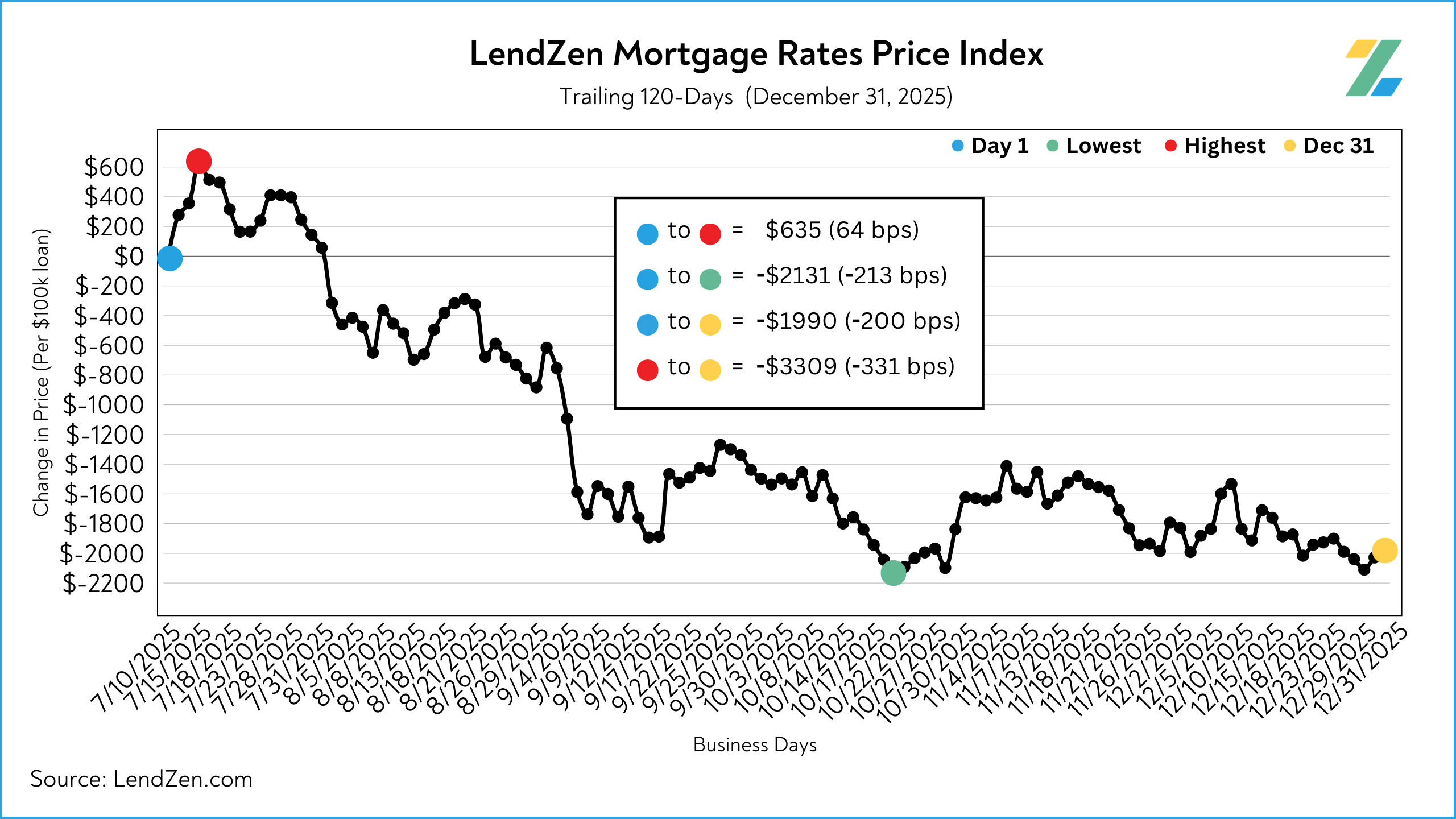

Since early August, when I first posted a version of this breakeven table, mortgage bonds went on a momentous rally.

The result was the best year for mortgage rates since 2020 and the best total return for mortgage-backed securities in two decades.

Higher bond prices mean that lower mortgage rates become less expensive.

In just the last two quarters of 2025 the price of getting a mortgage declined by as much as 330 basis points.

The same rate that might have cost 3-points in July is now 0-points, dramatically reducing the breakeven timeline for all borrowers.

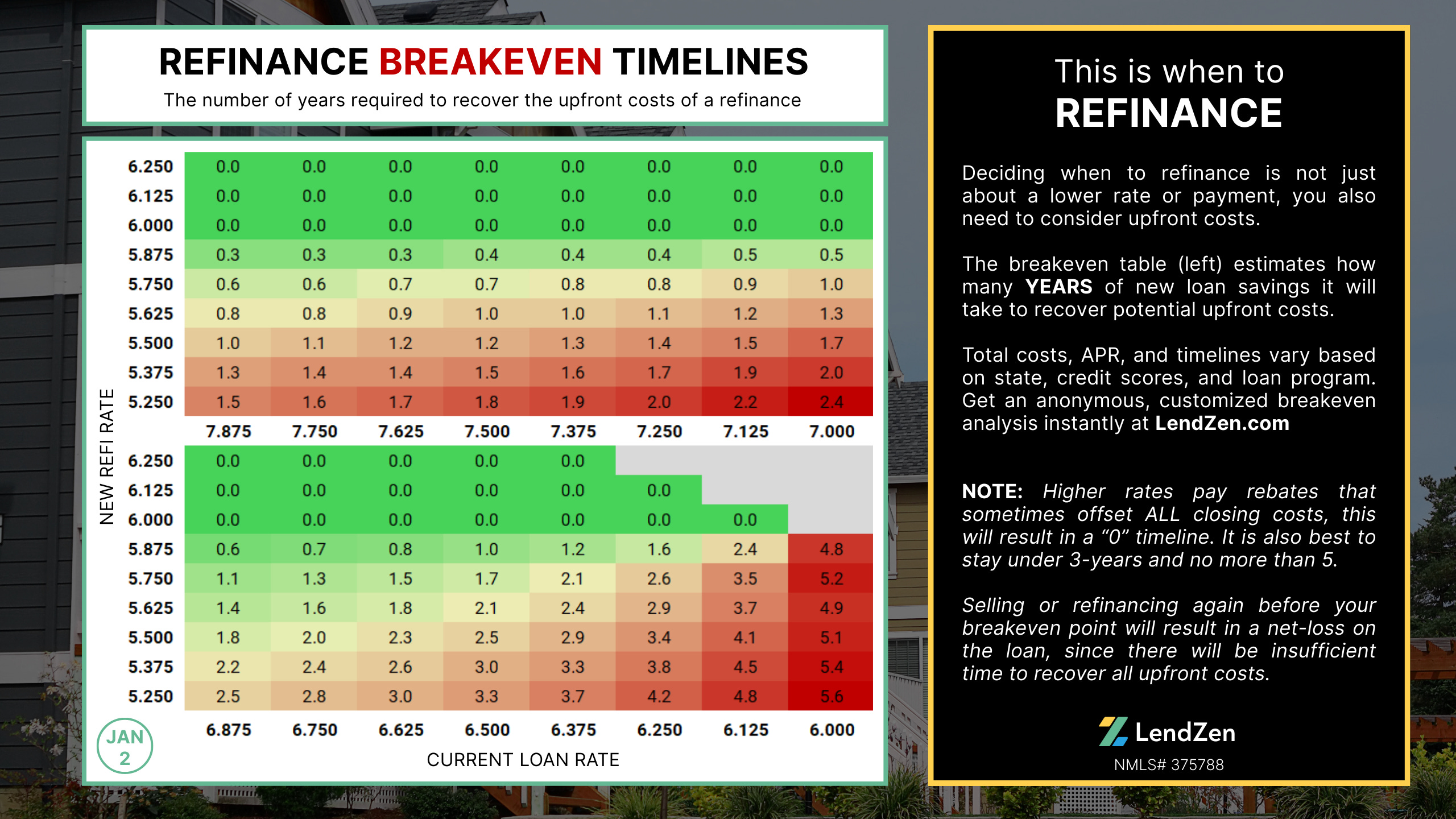

In august, the lowest current loan rate that could consider refinancing a minimum 0.25% lower with less than a 1-year breakeven was 6.875%.

Today, that rate is 6.25%, as the lowest “no cost” option is hovering around 6.00%.

In other words, if you have a 6.25% or higher you should be refinancing now.

To add further context on how much rates improved, going from a 6.875% to a 5.250% in August had a breakeven timeline of 4.9 years.

Today, it is only 2.5 years, which is within the “zone of consideration” (less than 3-years).

3-STEP GUIDE 📋

----------------

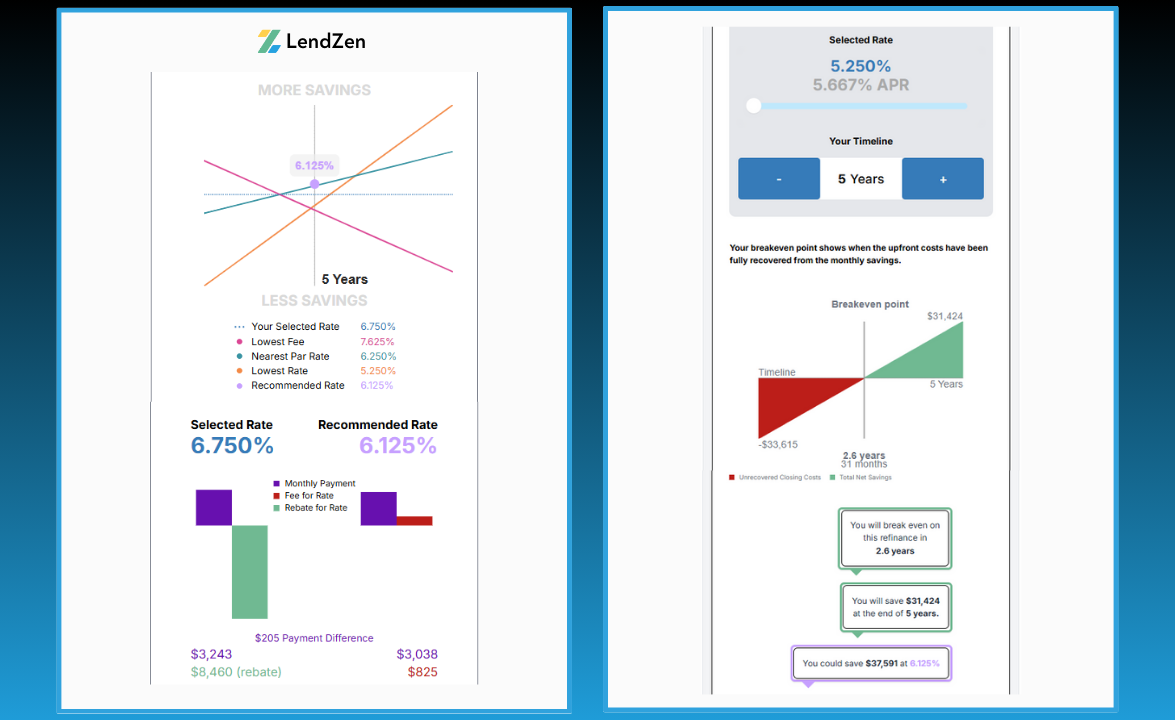

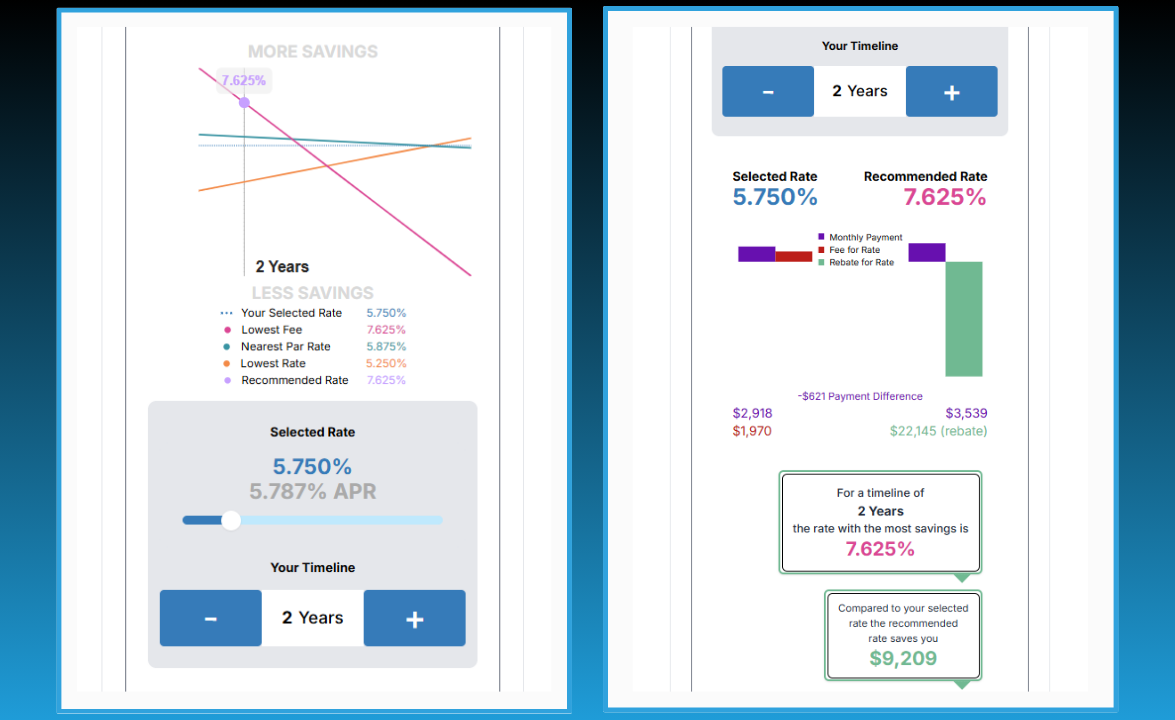

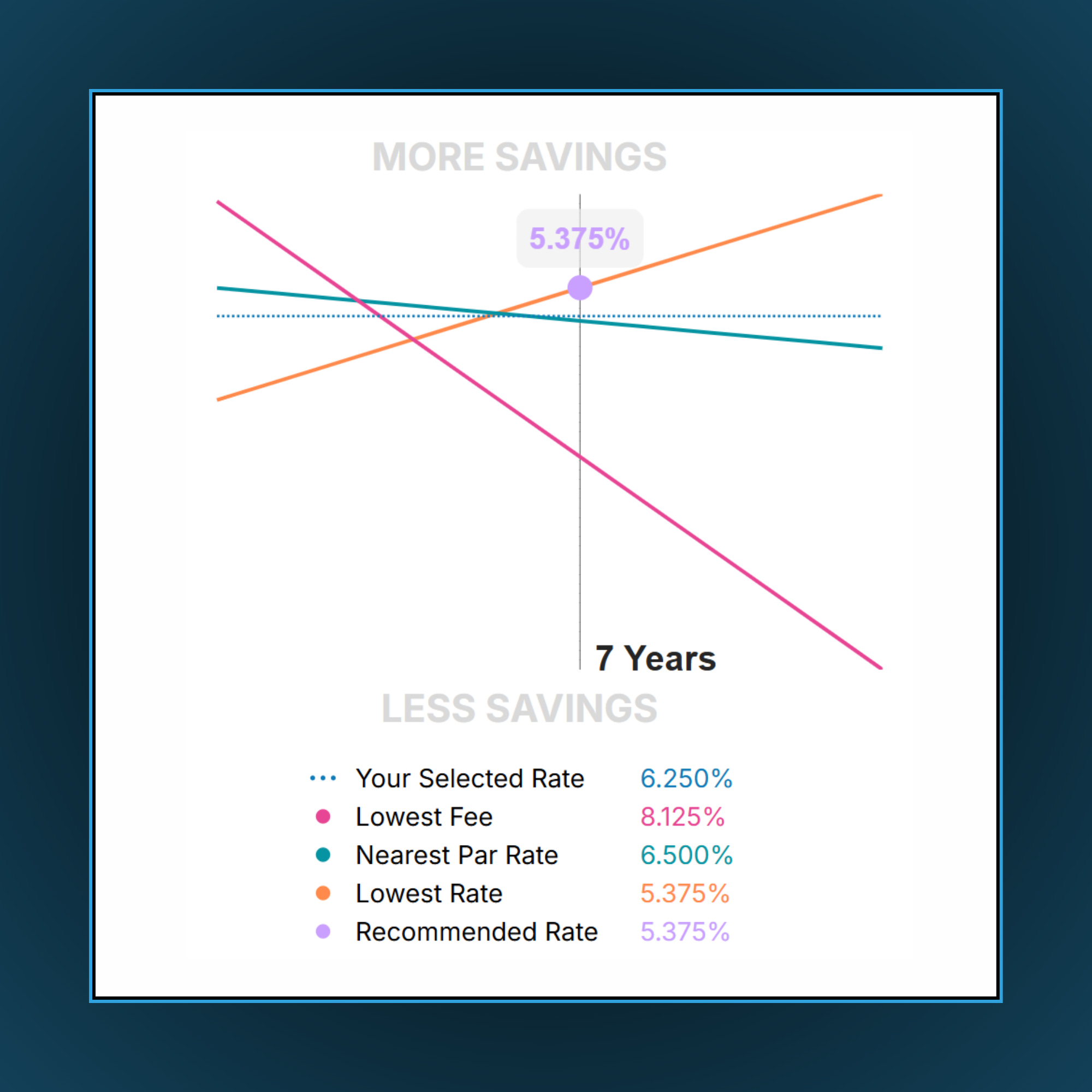

Here are the 3-steps to know if you are in range to refinance using the breakeven table

Find your current NOTE rate in either horizontal x-axis (there are two subsets)

Compare it with any of the refinance rates listed in the associated y-axis

Decide if the breakeven timeline (years) fits your objectives

The attached breakeven table “estimates” how many years of new loan savings it will take to recover potential upfront costs.

Selling or refinancing again before your breakeven point will result in a net-loss on the loan, since there will be insufficient time to recover all upfront costs.

Higher rates sometimes offset ALL closing costs; this will result in a “0” timeline.

It is also best to stay under 3-years (zone of consideration) and no more than 5.

Current note rates lower than 6.250% are unlikely to breakeven within that timeframe.

Total loan costs, APR, and exact timelines will vary based on state, credit scores, and loan program chosen.

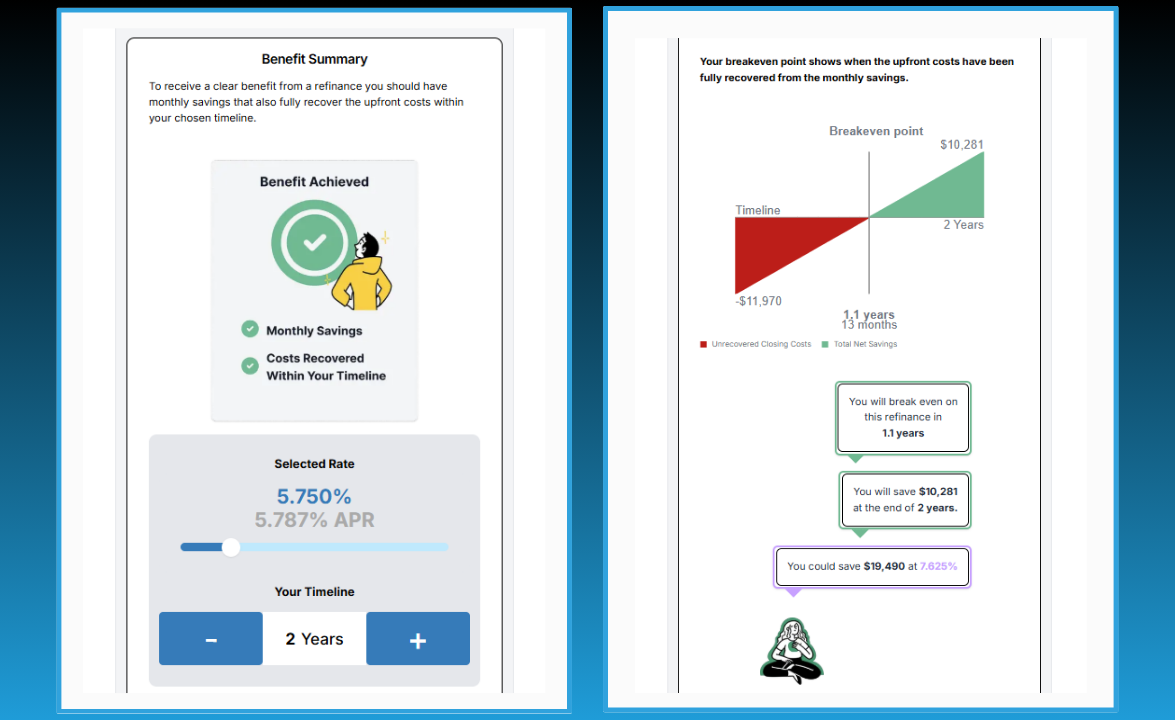

CUSTOMIZED BREAKEVEN 🎯

------------------------------

Get an anonymous, customized breakeven analysis, instantly at LendZen.

Click the link below for an interactive rate quote and scroll down to the Benefit Summary section to see the breakeven analysis.

You can MODIFY any of the loan parameters from that screen or customize your own from the home page.

Use the “Save this Scenario” option to receive a private link and check rates for your exact criteria anytime with just one click.

INTERACTIVE REAL-TIME RATE QUOTE

MODERN MORTGAGES 🏦

--------------------------

Most mortgages are sold into mortgage-backed securities (MBS) and the price of these bonds determines rates for all banks and lenders.

However, mortgage rates DO NOT rise or fall.

Instead, the price of each rate changes while the rates available to you remain the same.

The lower the rate, the more you pay upfront for it - this is often referred to as points but is more accurately known as a “discount fee”.

When mortgage bond prices rise the additional liquidity get passed through to borrowers making the price of mortgage rates lower.

This makes it “feel like” lower mortgage rates are suddenly available even though they always existed.

This rate-price dynamic also means the higher you go in rate, the lower the discount fee.

Some rates even pay a rebate - this typically increases as you go higher in rate.

Rebates and discount fees change daily, based on the fluctuation in mortgage bond prices.

BEST REFI RATE 🧮

------------------

Deciding if a refinance is worth it depends on two things:

The timeline you predict to be in the loan, before selling or refinancing again

The breakeven point for the rate you choose falls within that timeline

Multiple rates could breakeven within your timeline, and the BEST rate is not necessarily the lowest.

Instead, choose whichever rate provides the most net-savings at the end of your selected timeline.

When you are offered a “No Points” loan, the rate quoted has enough rebate to offset the fees normally charged by that lender in Section A of the Loan Estimate disclosure.

This is VERY different than a “No Cost” loan, which means the rate chosen has enough rebate to eliminate ALL new costs of doing the loan.

Although the “no cost” rate will be higher, the savings are immediate because there are no upfront costs to recover.

This type of approach usually provides the most benefit (net-savings) for borrowers considering shorter timelines.

The “timeline” is not about the loan term (15-Year, 30-Year, etc.) and in many cases isn’t necessarily about how long you plan to be in the home.

When choosing a timeline, you need to also consider how long before you think mortgage rates will become less expensive and choose the shorter of the two timelines.

Timeline is the only subjective part of deciding which rate to choose.

The rest is derived mathematically, with only one rate that provides the most benefit for that timeline.

To instantly and anonymously find the rate with the most benefit for your exact loan criteria visit LendZen.com

Thanks for reading.

If you want to shop real-time mortgage rates and get instant qualification results without providing any contact information visit LendZen.com

LendZen provides a fully automated mortgage shopping experience that gives you anonymous access to all mortgage rates with full transparency of costs upfront as bond prices change.

LendZen Inc. is an equal opportunity mortgage lender, NMLS 375788.