Mortgage Rate Price Tracker 🏠 📉🔍 (DEC 1 – 19)

Monitoring the change in price of specific mortgage rates

Included in this post are the following:

THE TRACKER 🔭

----------------

Most mortgages are sold into mortgage-backed securities (MBS) and the price of these bonds determines rates for all banks and lenders.

However, mortgage rates DO NOT rise or fall. Instead, the price of each rate changes while the rates available to you remain the same.

The Mortgage Rate Price Tracker (MRPT) illustrates this dynamic by showing how the price of each rate changed within the time series.

This change is driven by mortgage bonds, not the lender, who will then add their own fees on top.

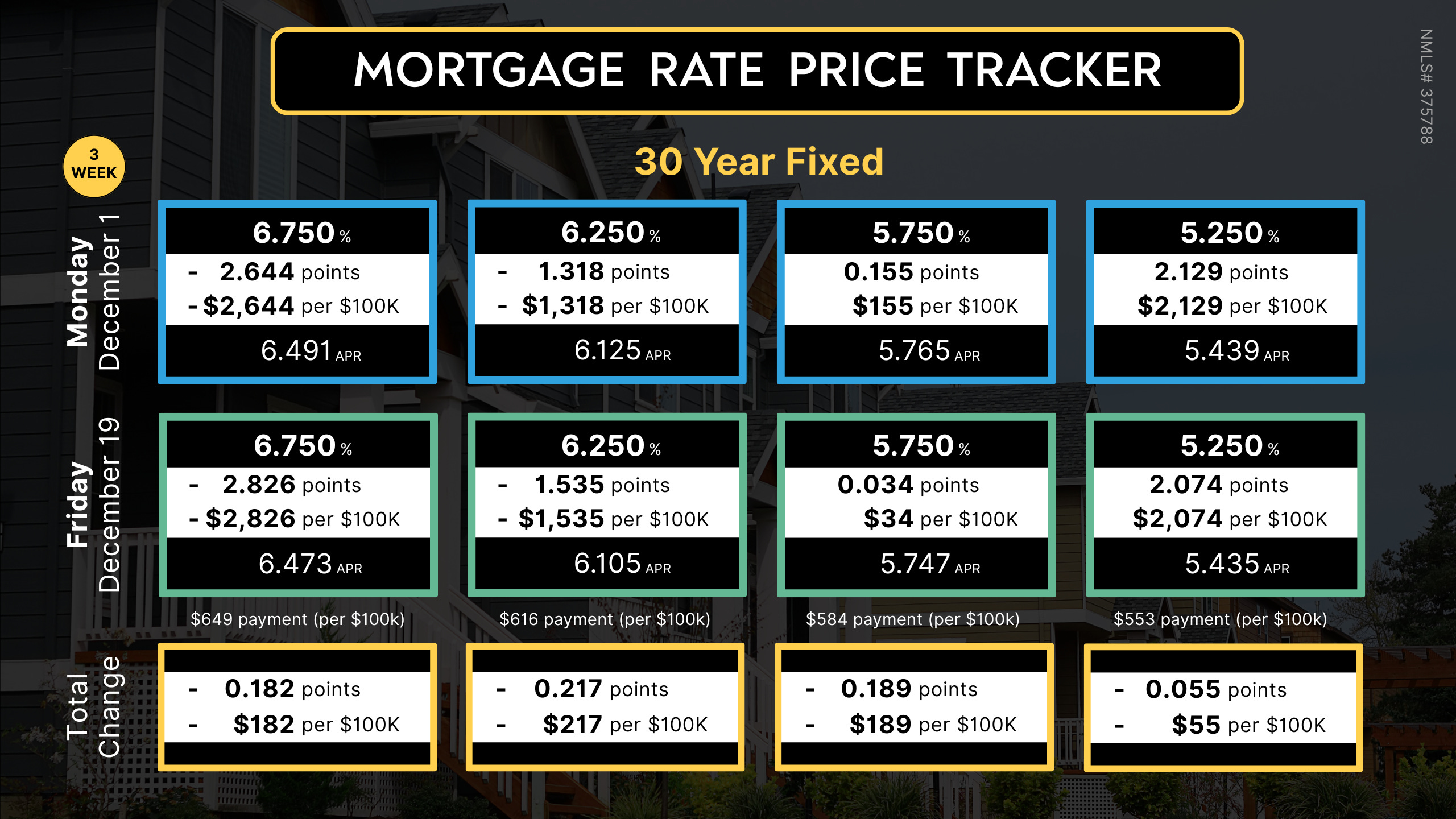

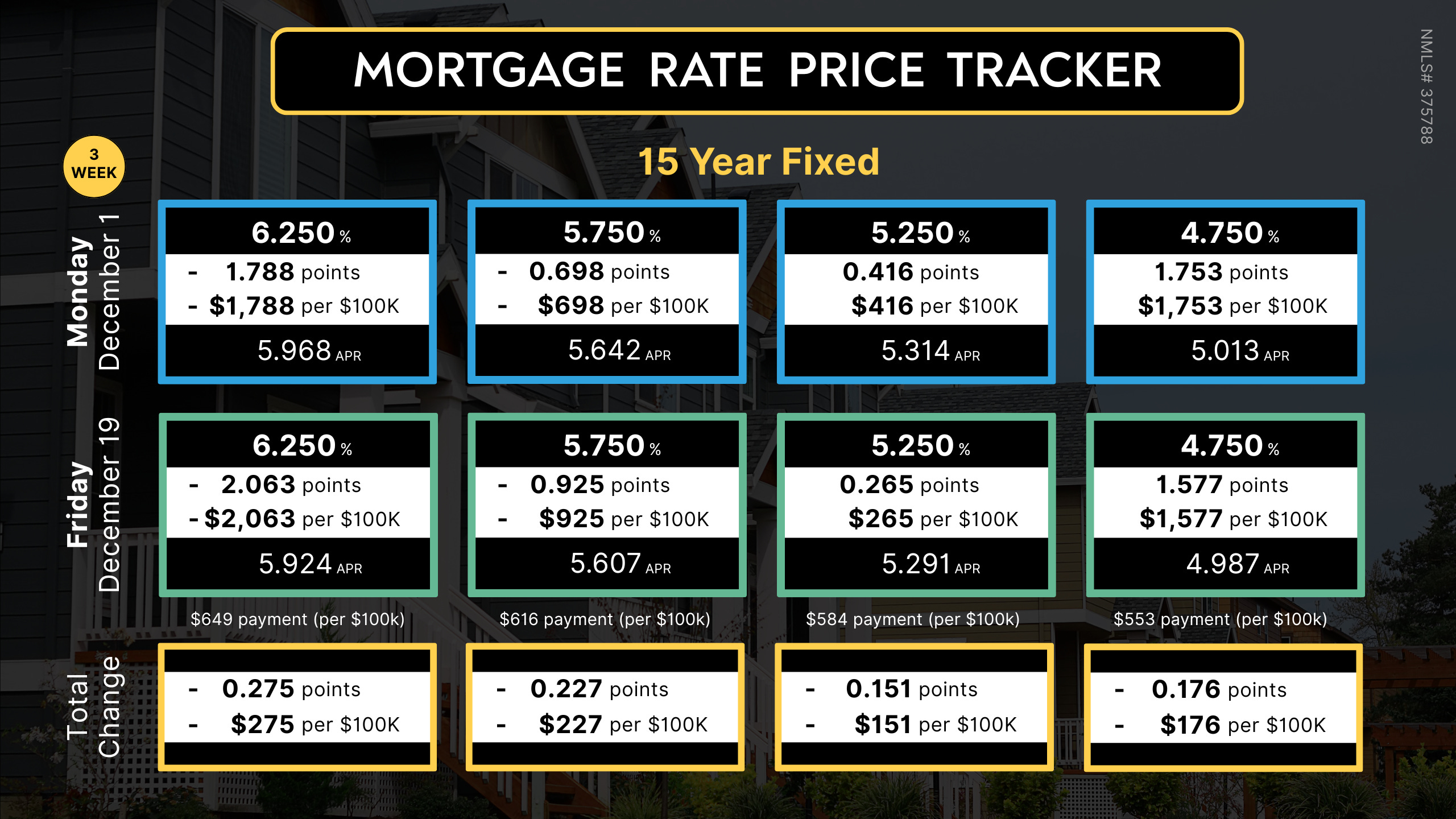

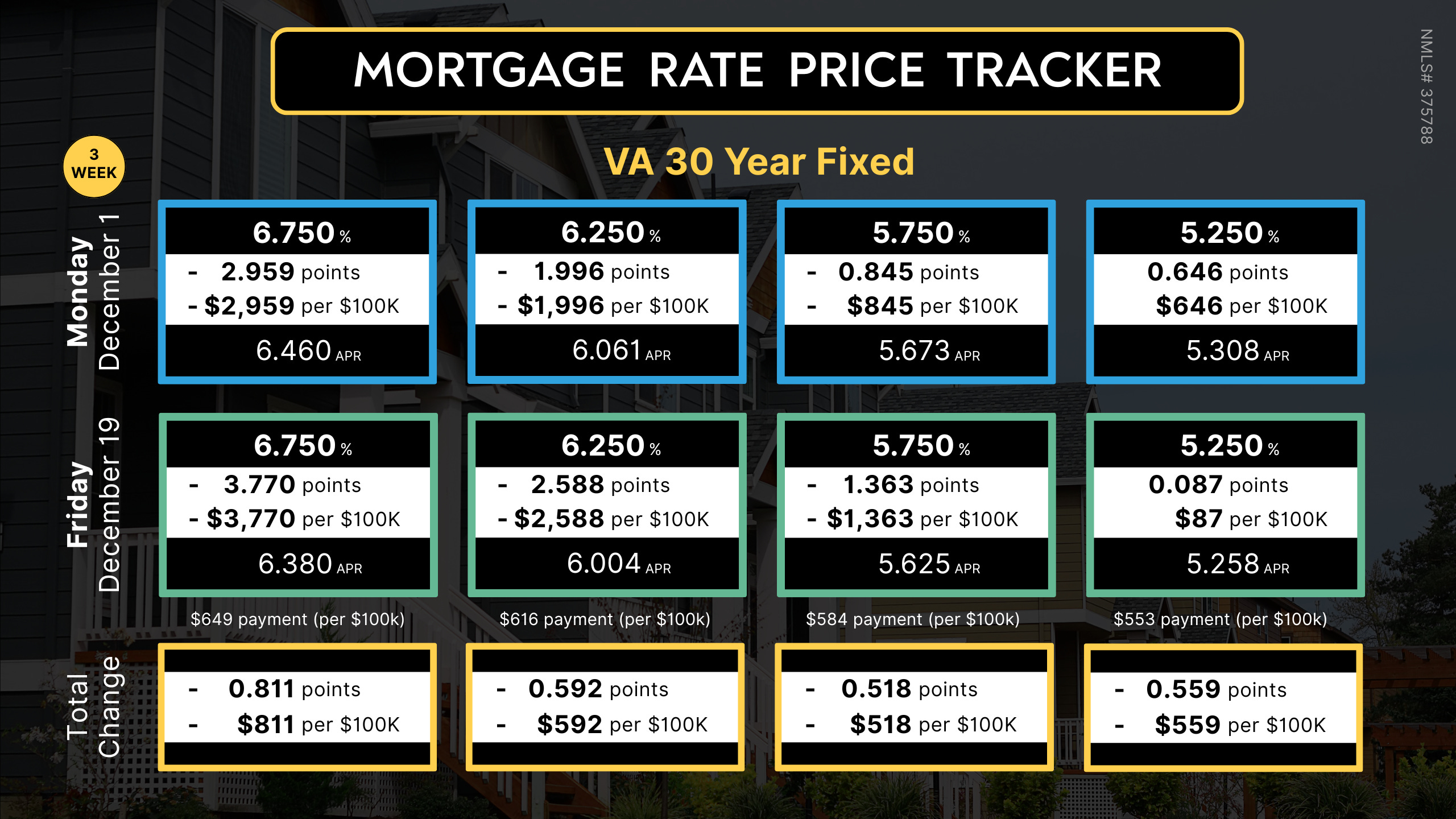

The higher the rate, the lower the fee (points). Some higher rates pay a rebate; this is illustrated on the tracker with negative (-) points.

When the “total change” is negative it means a reduction in the price of the rate.

The MRPT is a more “rate and loan program” specific example of the LendZen Index, which monitors a much broader set of rates and mortgage bond coupons.

Both are effective for visualizing how the PRICE of mortgage rates has changed, while the LendZen Index is published daily at LendZen.substack.com

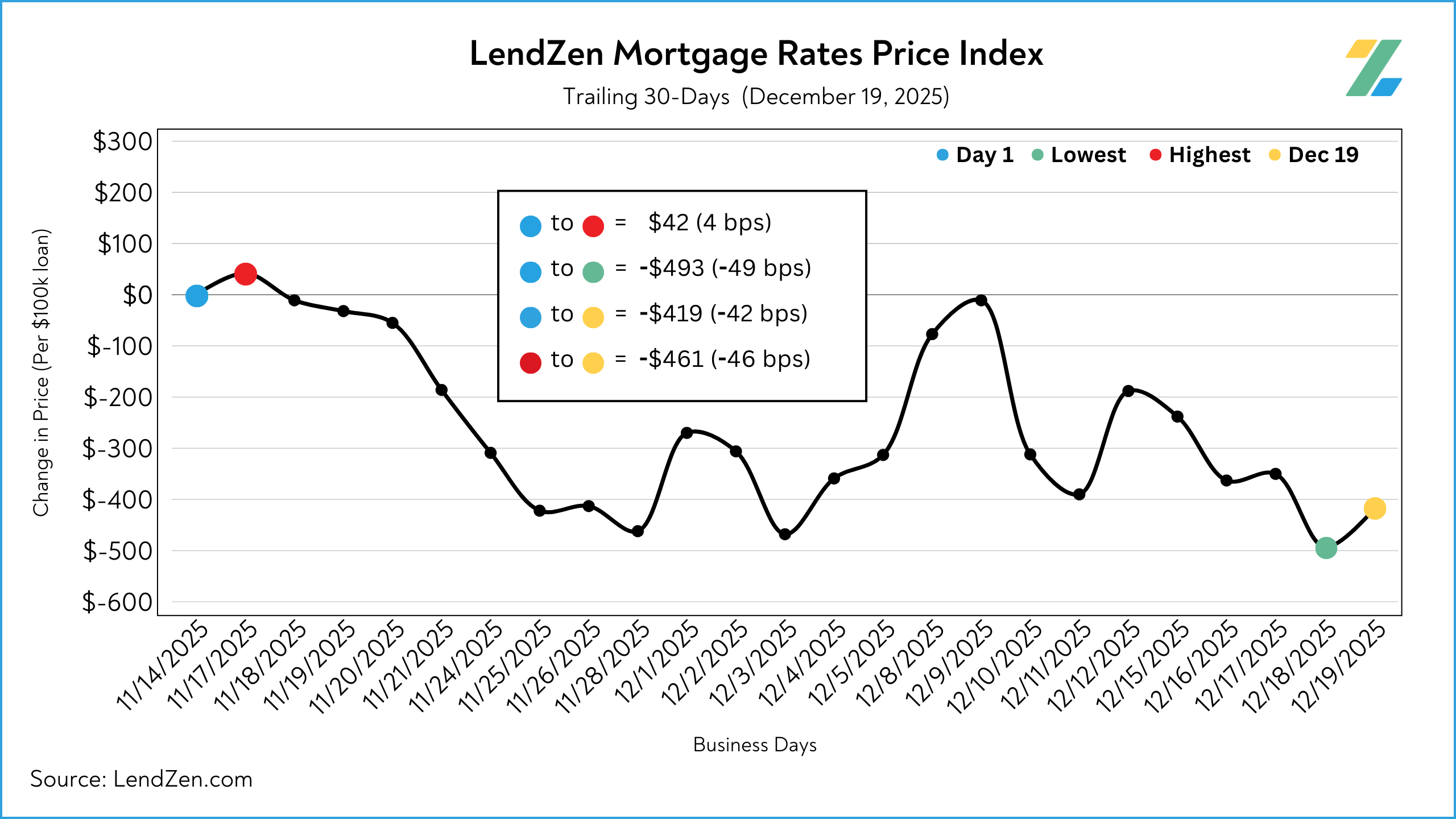

WEEK 3 📉

---------

Since the LendZen Index has a variety of time series, the MRPT will focus on just the current month’s activity.

Attached are the results for December Week 3.

You can also explore the final results for Week 2 on this previous Substack post.

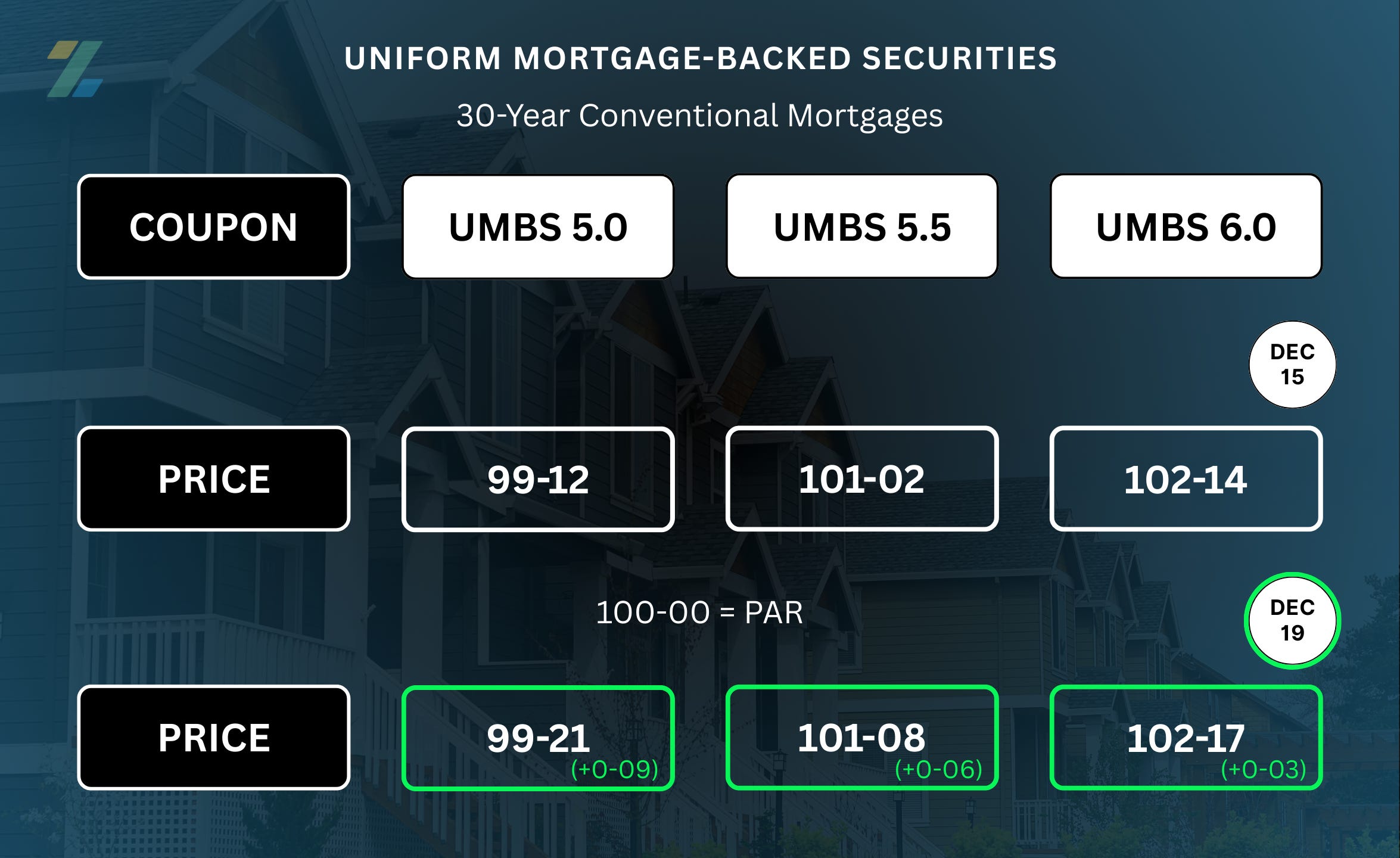

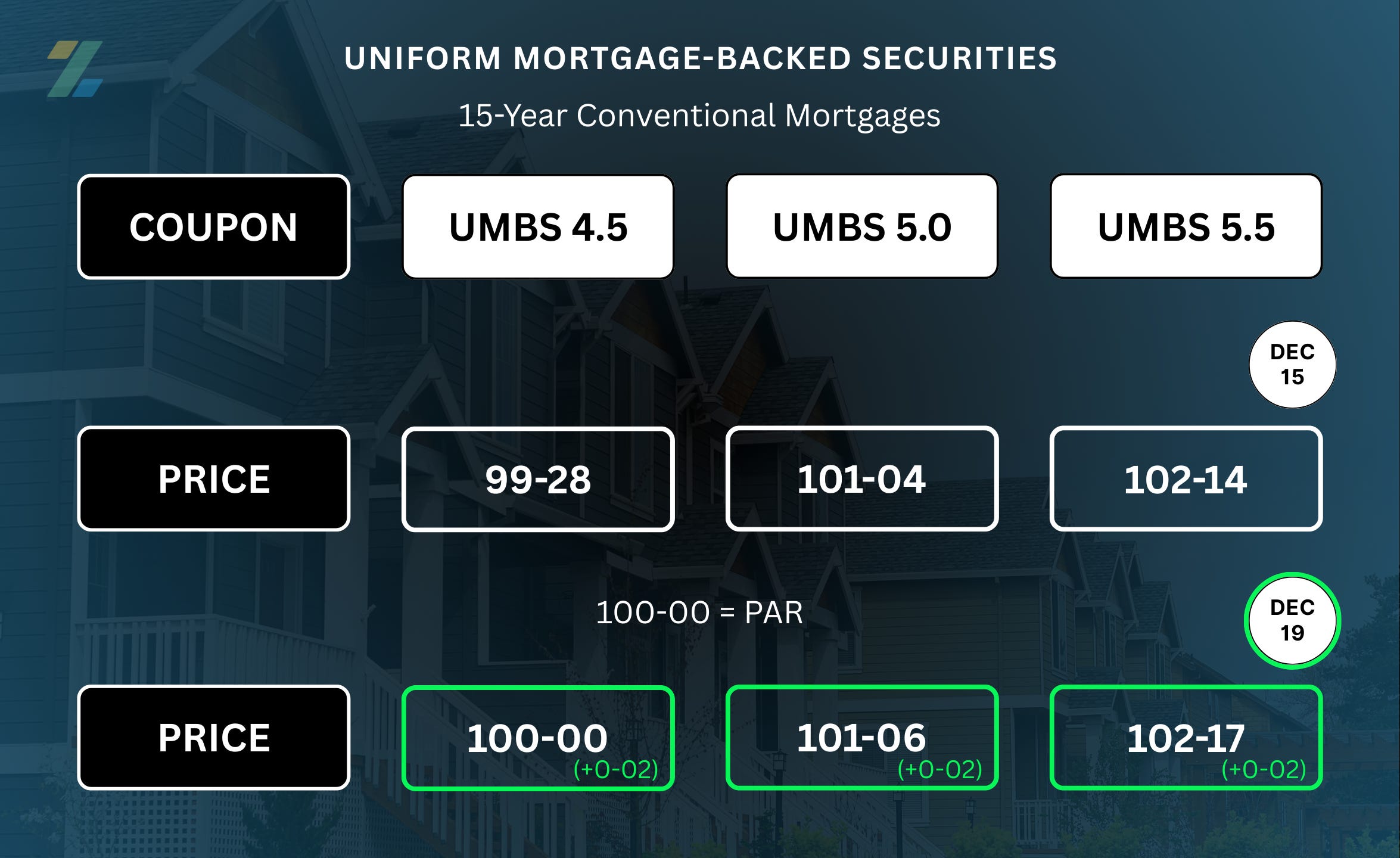

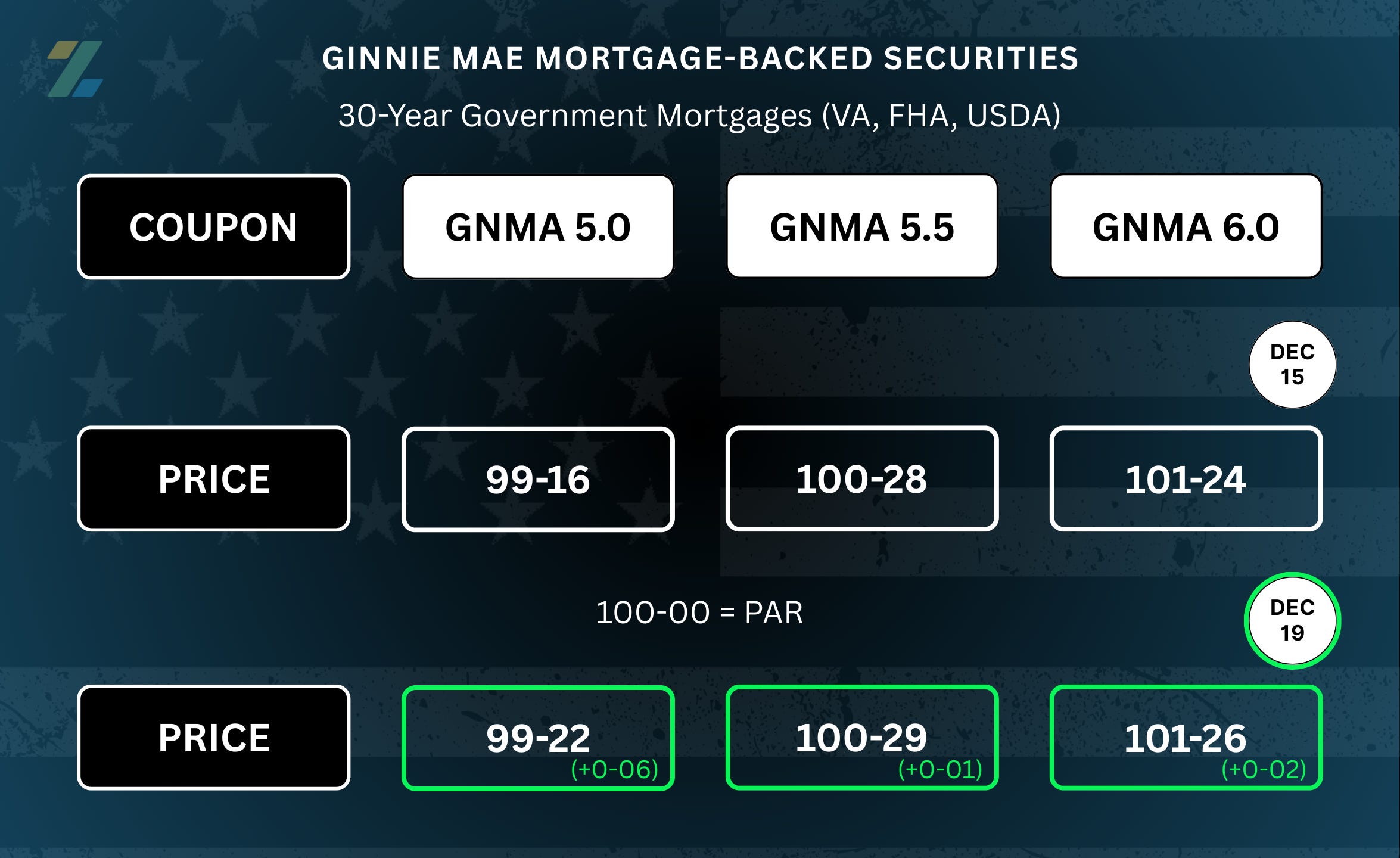

MBS PRICING 🏦

----------------

NEW to the Tracker are the current week’s MBS coupon price changes.

MBS coupons are sold at half-percent increments, while their price moves in 32nds (ticks).

ex. (0-04) = 4/32 = 12.5 bps

100-00 acts as the starting line, also referred to as PAR.

The higher the coupon price, the less expensive the rates will be that are sold into that security.

Therefore, an increase in the price of mortgage bonds is good for mortgage rates.

Learn more about the dynamics of MBS pricing and how it impacts your mortgage options in any of the bi-weekly “Rate Snapshot” Substack posts.

RATE RECAP ⏪

--------------

Mortgage bonds come through the week’s Double Whammy on the winning side of things.

The December Non-Farm Payroll report (Tuesday) did little to inspire bonds, but Thursday’s CPI inflation report finally helped nudge things in the right direction.

November inflation came in below 3% for the first time since August 2024, prior to that year-over-year inflation hasn’t been in the 2-handle since March 2021.

Bonds liked it, but the rally was slightly subdued, perhaps due to skepticism around how “thorough” the data is given our recent government shutdown.

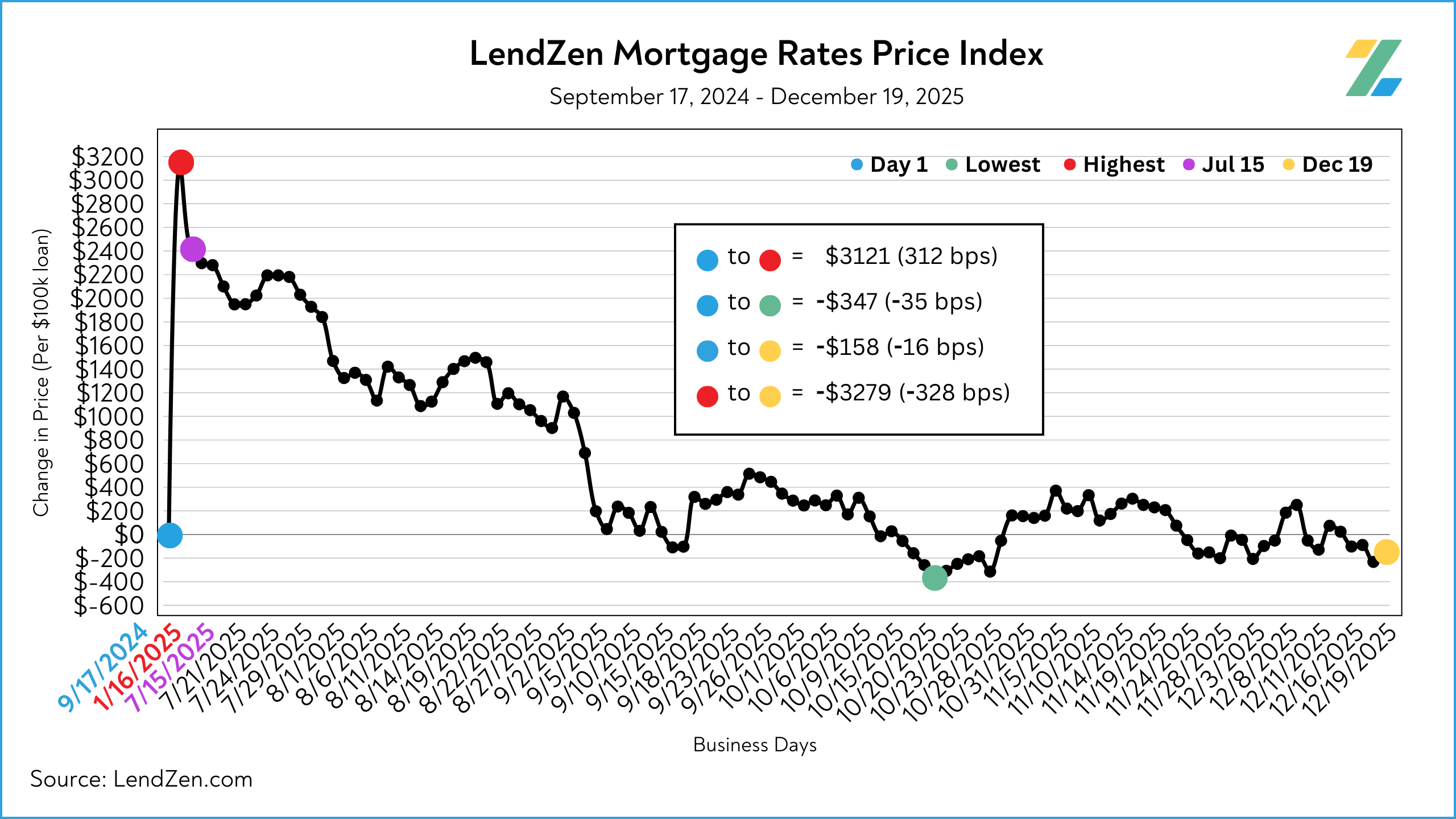

On Friday, mortgage rates gave back some of the gains but overall the month of December has been meaningfully positive, with most conventional loan rates seeing a 3-week drop in price of 20-bps or more, while VA loan rates fared twice as well.

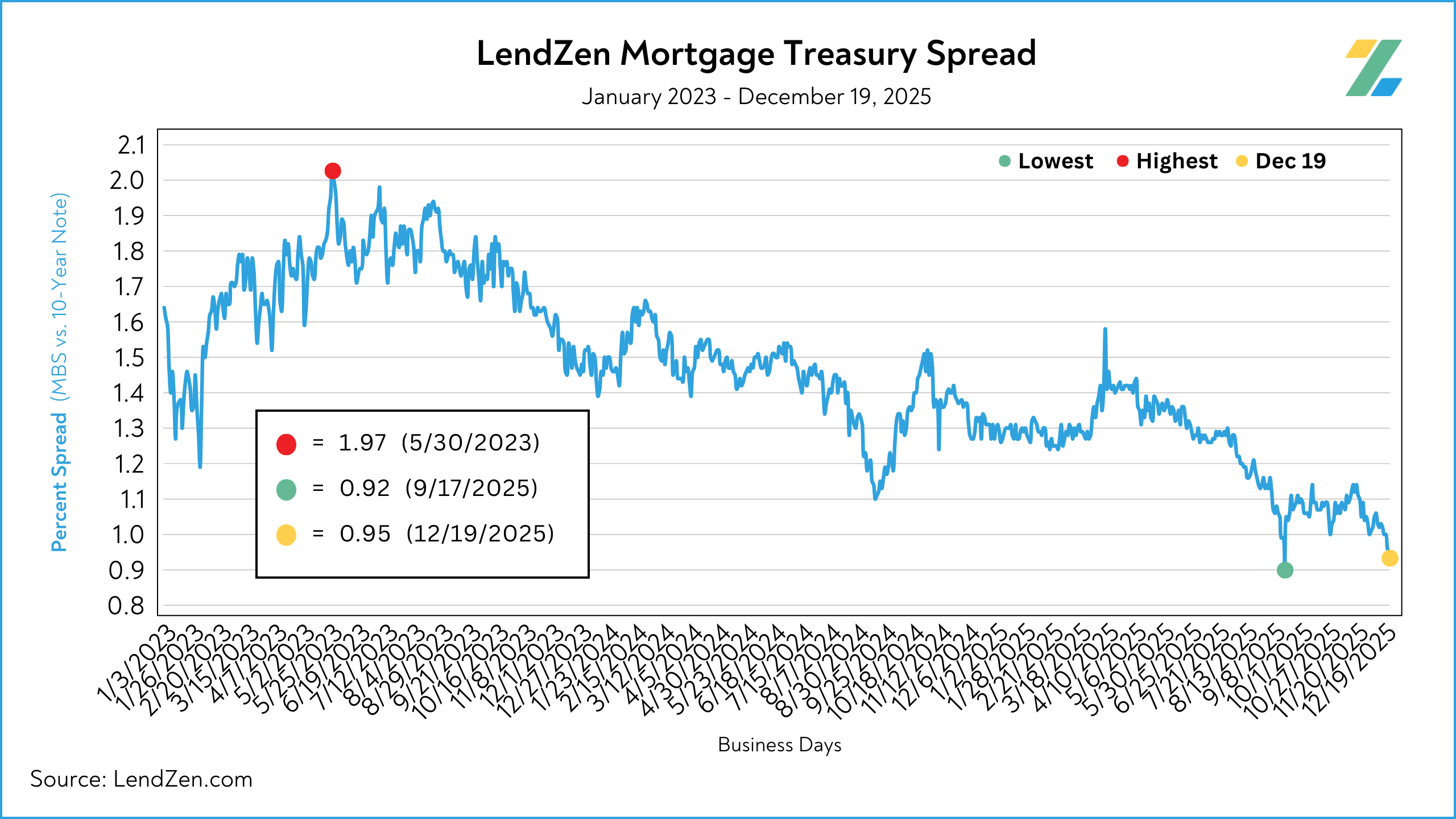

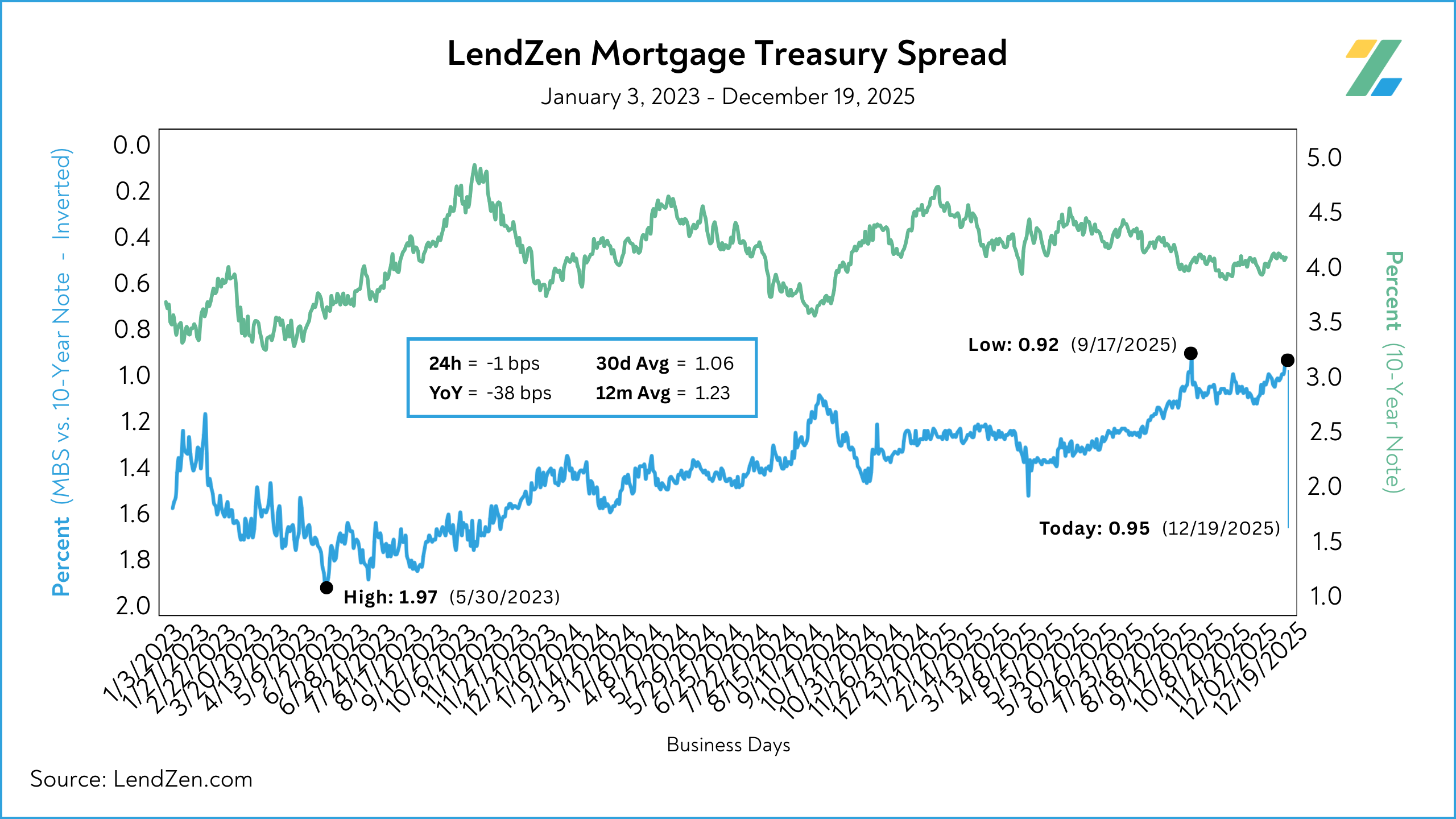

The recent improvement is all well and good, but the big reason mortgage rates are at the best levels of the year is predominantly due to the spread between the 10-Year and MBS dipping below 1%, and within 3-bps of a multiyear low.

For all the attention people in the mortgage industry like to put on the 10-Year, the mortgage spreads are what matter.

The reason mortgage rate PRICES have surpassed 2024, despite a 48 bps higher 10-Year (3.66 vs 4.14), is because the spreads have compressed over 30-bps since last year.

Learn more about the importance of mortgage spreads in this Substack post.

UP NEXT 🗓️

----------

With the “Big 3” data (NFP, CPI, FOMC) out of the way, the rest of the year should hopefully be quiet.

Next week is short with markets closed on Thursday for the Christmas Holiday and nothing of importance Friday.

Tuesday has a delayed preliminary Q3 GDP report, but the actual third and final estimate has been postponed until Thursday, January 22, 2026.

Besides the initial GDP estimate, durable goods orders, and various Treasury bond auctions, there isn’t a whole lot that is expected to rattle markets.

Hopefully, Santa doesn’t have any off-script surprises for us, so we can enjoy a long weekend while basking in the best year for mortgage rates since 2020.

After peaking on January 16, mortgage rate PRICES have declined by over 320 basis points.

That means the cost of getting a $500k mortgage (regardless of rate) is $16,000 cheaper today than at the start of the year.

Thanks for reading.

If you want to shop real-time mortgage rates and get instant qualification results without providing any contact information visit LendZen.com

LendZen provides a fully automated mortgage shopping experience that gives you anonymous access to all mortgage rates with full transparency of costs upfront as bond prices change.

DISCLOSURES

LendZen Inc. is an equal opportunity mortgage lender, NMLS 375788.