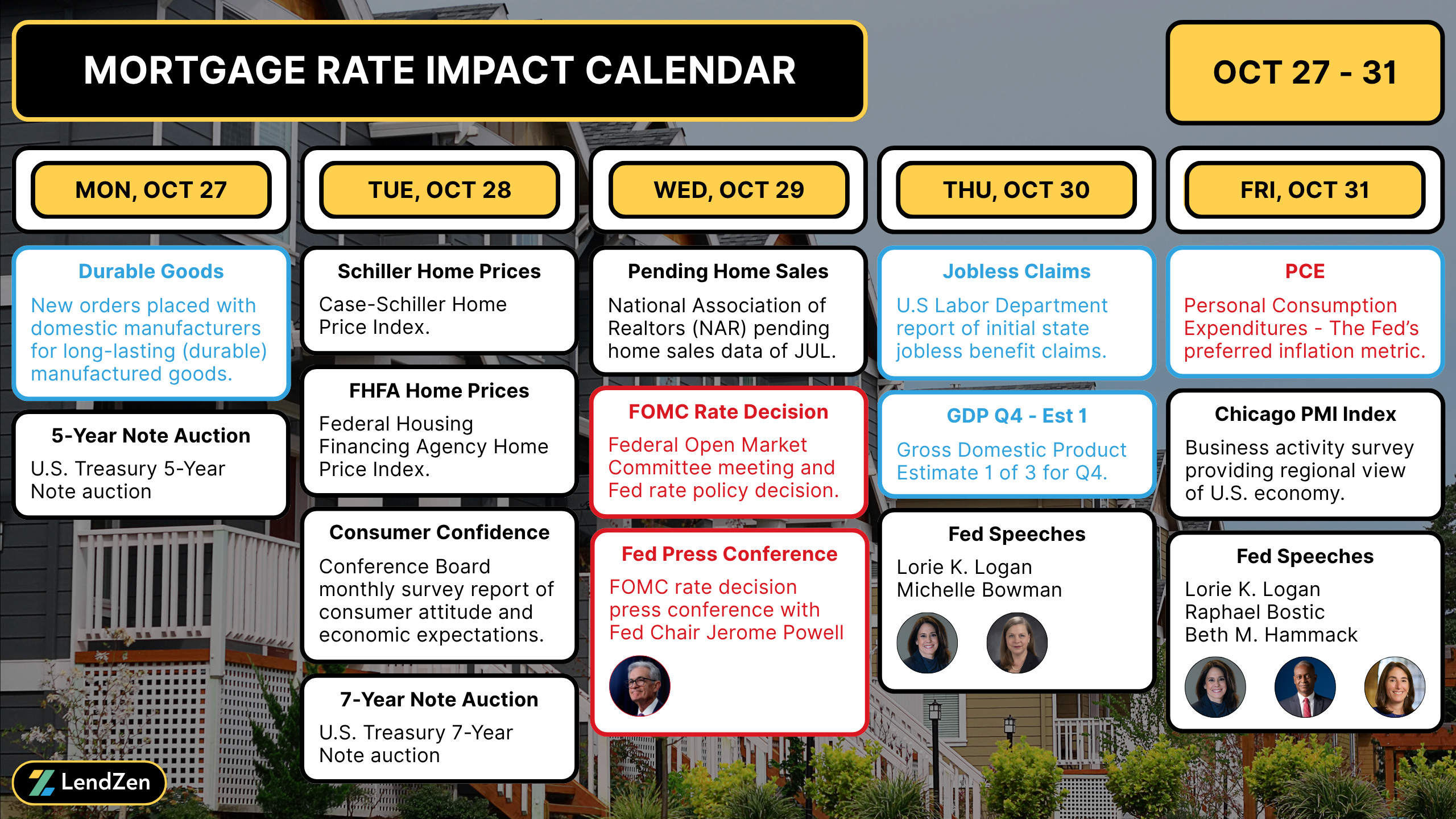

Mortgage Rate Data Deluge – OCT 27 🏠📉🔒

Here is a deluge of mortgage rate data to start your week!

KEY TAKEAWAYS ✅

------------------

Jawbone Jitters:

The Fed is widely expected to hold rates steady, but Powell’s press conference tone will be scrutinized. Meanwhile, GDP (Thursday) and PCE (Friday) could be delayed due to the shutdown, making Wednesday’s FOMC the key event steering mortgage rate pricing.

Mixed signals:

Friday’s CPI inflation was a mixed bag, which will put extra attention on this week’s durable goods and PMI data, especially in the absence of PCE, GDP, and the long overdue NFP employment report.

Shutdown Wildcard:

If GDP and PCE do end up being delayed, post-FOMC reactions could be what establishes directional momentum for the rest of the week.

**Events marked blue could be delayed by the shutdown.

Deeper analysis - be sure to read the RATE LOCK GUIDE at the bottom of this post for a more detailed rationale of what could impact mortgage rates in the weeks ahead.

MARKET RECAP 📉

------------------

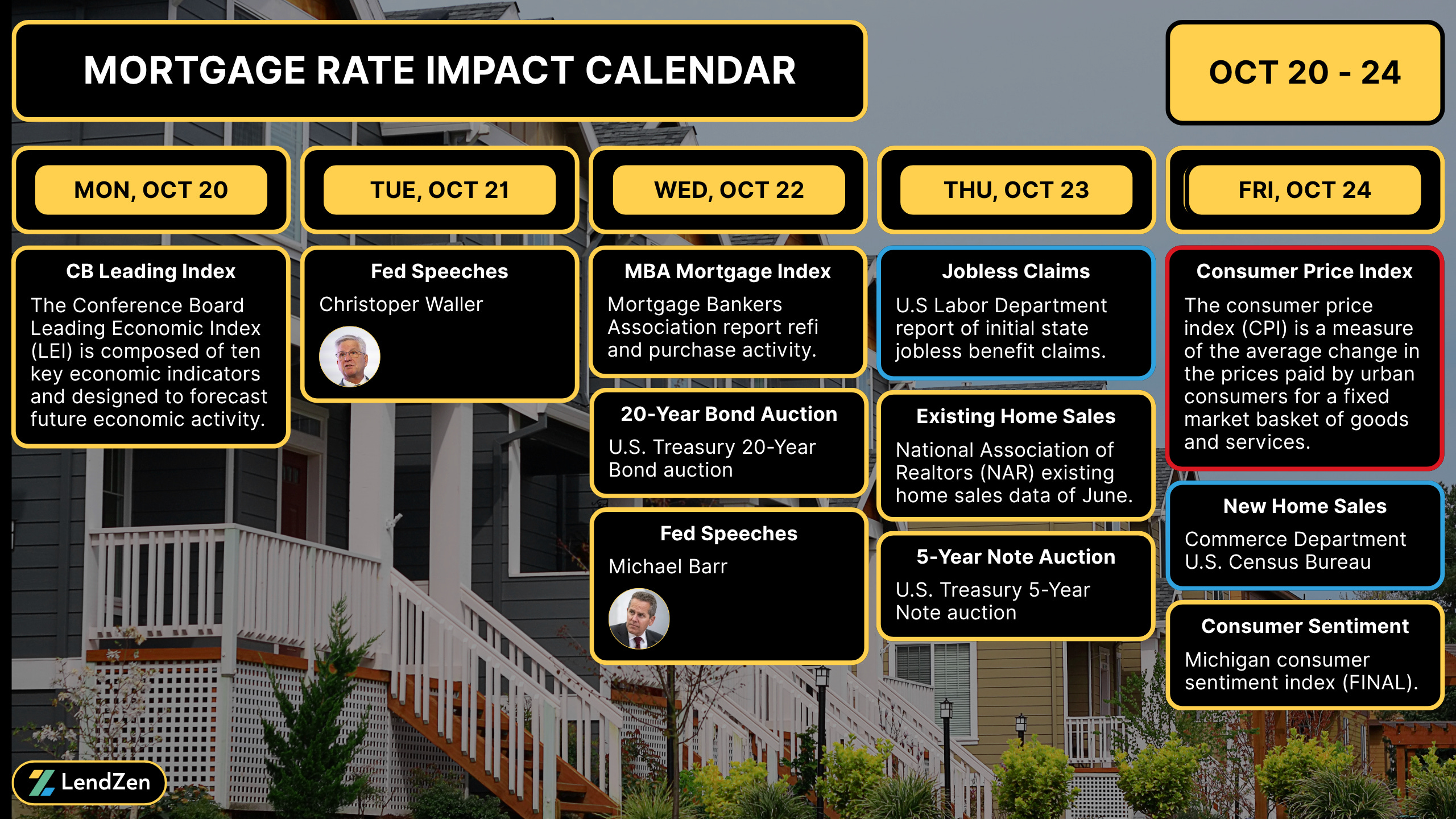

After 3 full weeks of the U.S. government shutdown we finally got some worthy econ data on Friday, after the Labor Department was called back to release the Consumer Price Index inflation report.

The highly anticipated CPI was within expectations and well received by bond markets with a decent rally in government bonds, while mortgage-backed-securities (MBS) showed less enthusiasm.

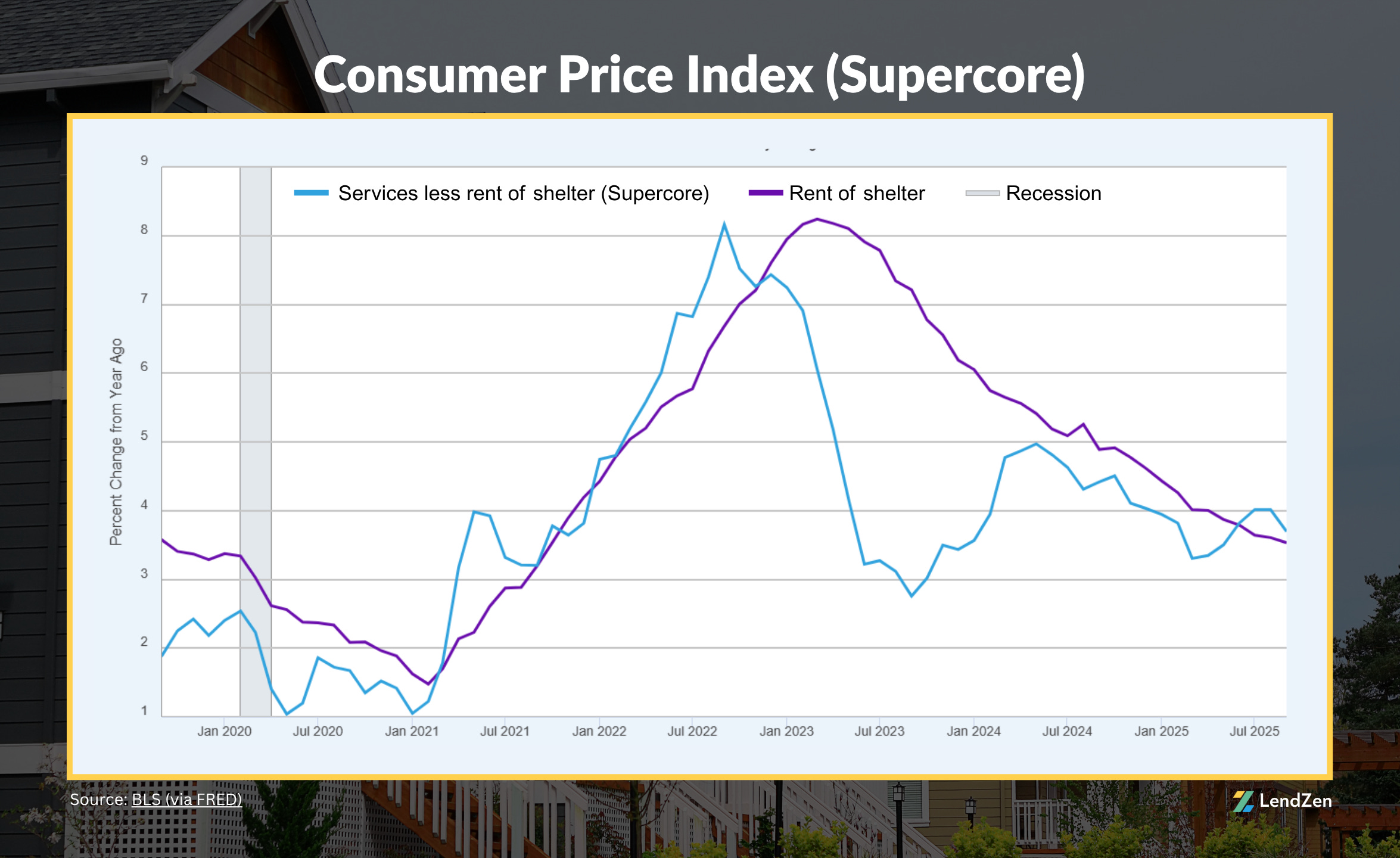

Inflation is measured as a rate of change.

Although the percentage change matters to the consumer (from whom the source CPI data is collected), how that number aligns with investor expectations is far more impactful to markets – most importantly bond markets.

There are also sub-sections of the inflation data called Core and Supercore.

Core removes the move “volatile” categories of food and energy, while Supercore also excludes housing because of the lag (delay) in its data.

Supercore inflation became something of relevance after Fed Chair Jerome Powell mentioned in a November 30, 2022 speech that it “may be the most important category for understanding the future evolution of core inflation”.

Supercore mostly reflects the prices of services, including those provided by lawyers, plumbers, hairdressers, etc.

For those who like the raw data, here it is:

September CPI Month-over-Month

· Headline: + 0.4% (0.3% forecast)

· Core: + 0.2% (0.3% forecast)

· Supercore: + 0.2%

September CPI Year-over-Year

· Headline: + 3.013% (3.1% forecast)

· Core: + 3.019% (3.1% forecast)

· Supercore: + 3.7%

MORTGAGE RATE PRICES 📉

------------------------------

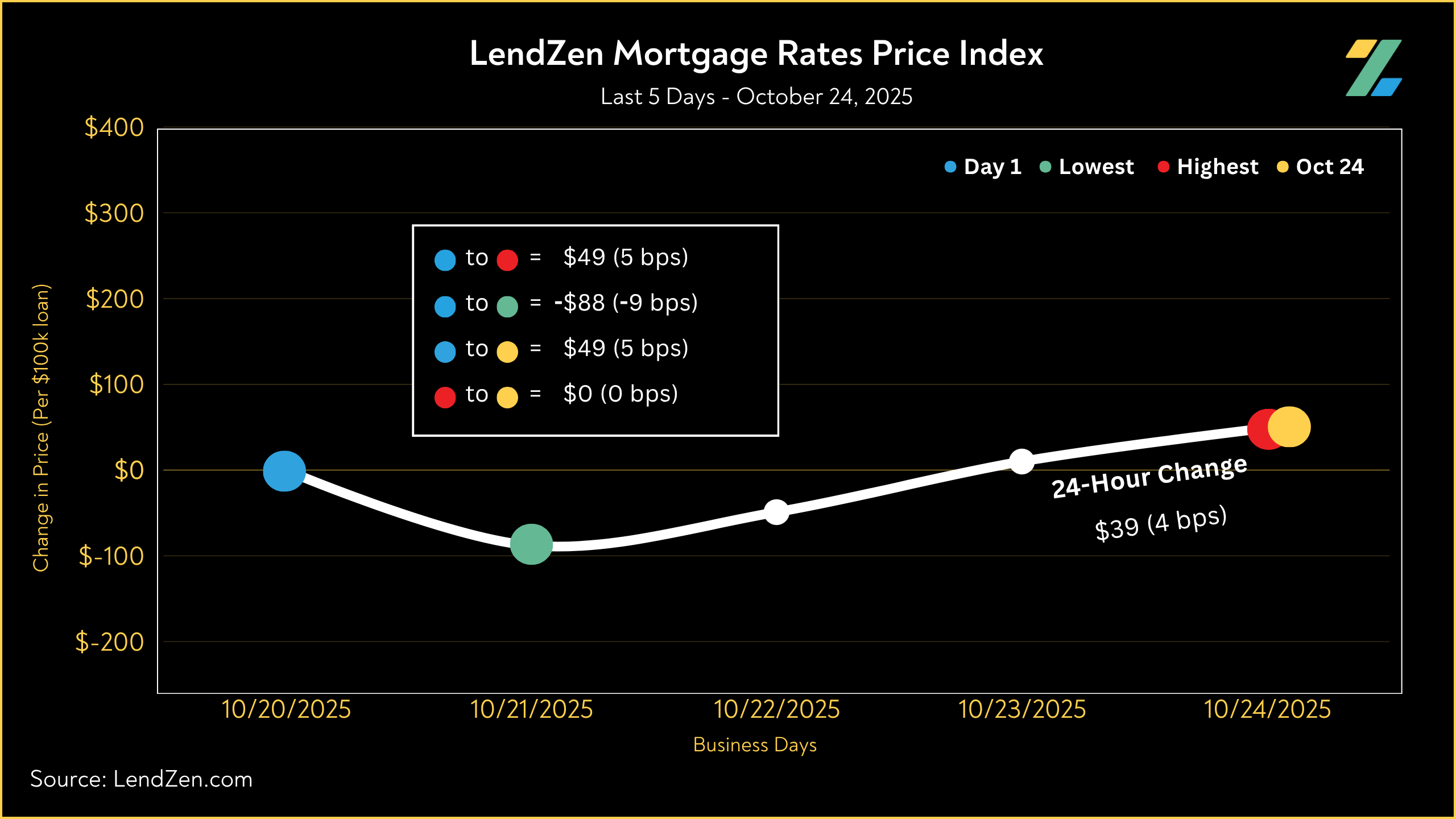

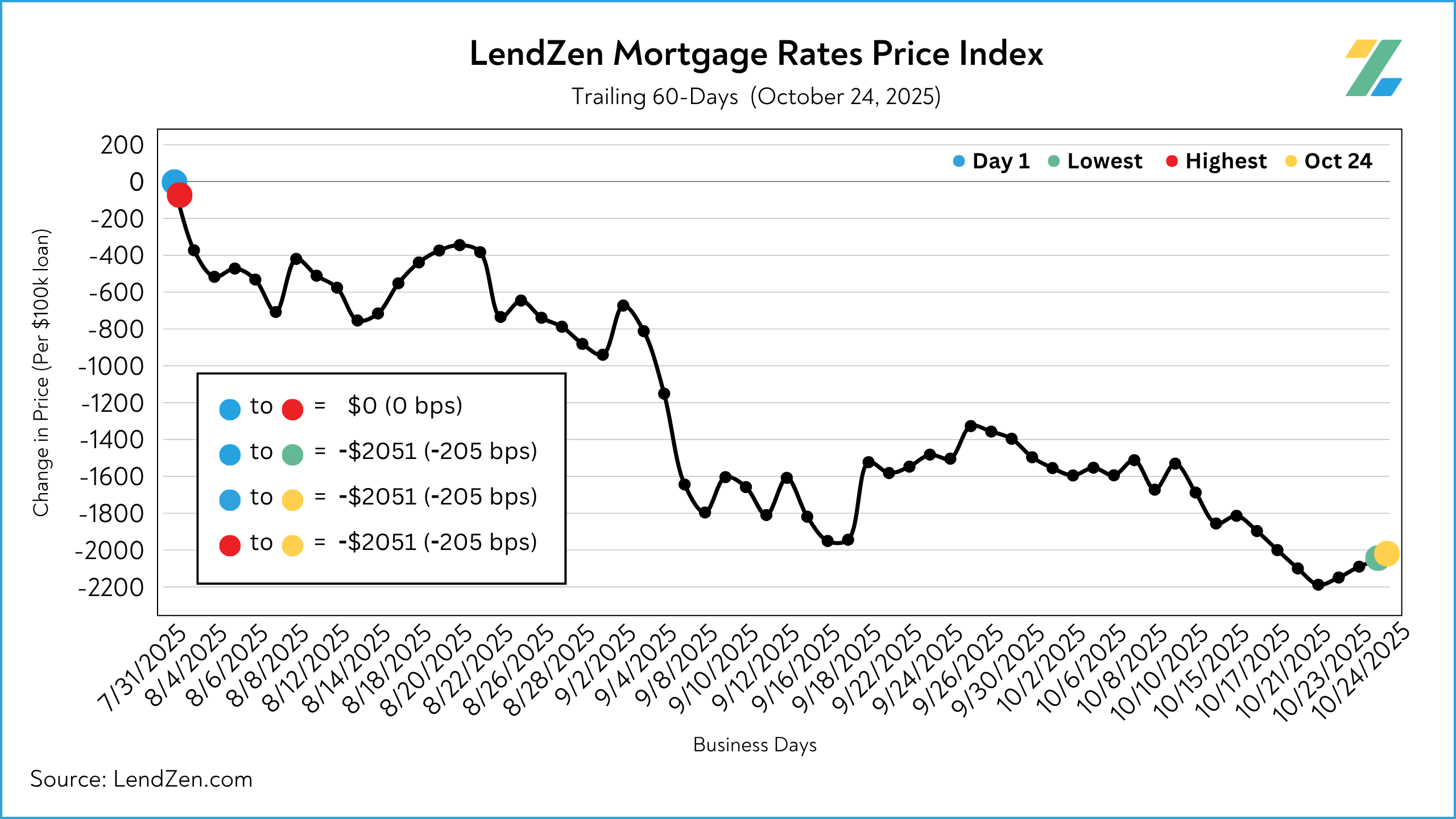

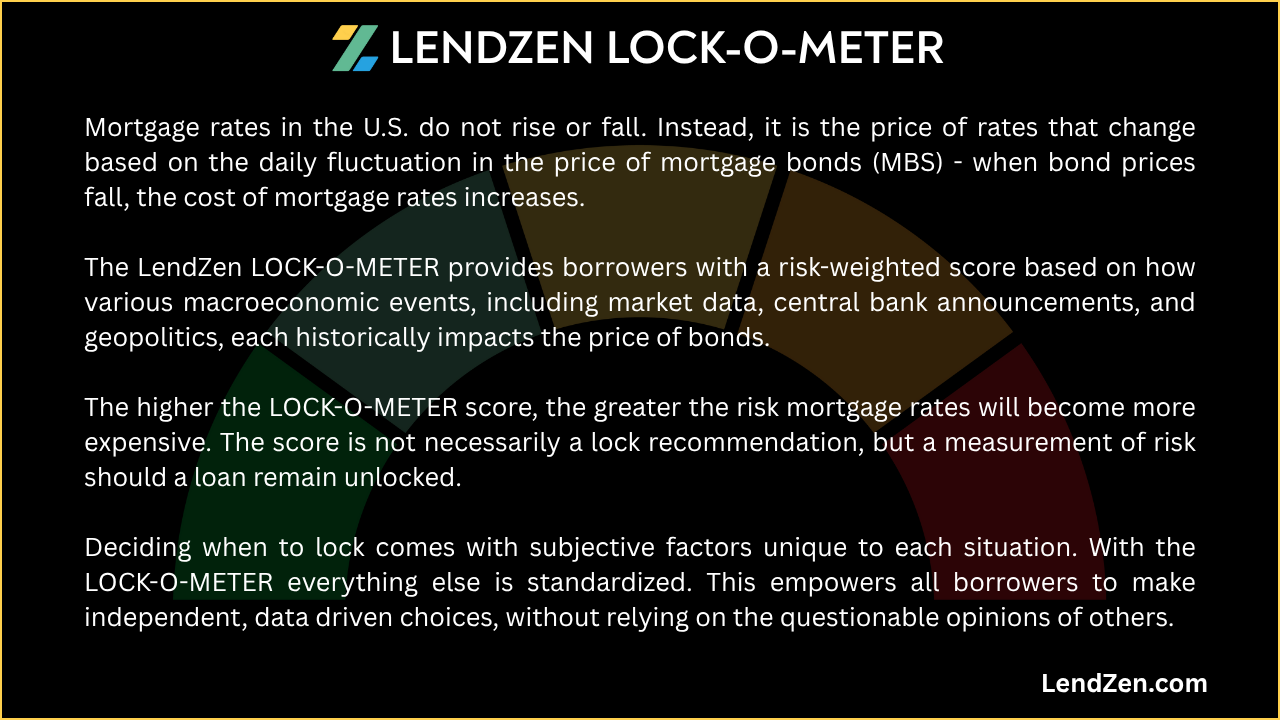

Mortgage rates do not rise or fall, instead the PRICE of rates change.

The LendZen Index calculates a daily change in the price of mortgage rates by tracking a spectrum of mortgage-backed securities (MBS).

This provides borrowers with a more specific measurement of how the cost to obtain a mortgage is changing, regardless of the lender, rate, or credit score.

-----------

10/24/2025

-----------

24-Hour: +4 bps ($39 per $100K)

5-Day: +5 bps ($49)

10-Day: -36 bps (-$363)

30-Day: -47 bps (-$469)

60-Day: -205 bps (-$2,051 less expensive per $100K)

Last week was as flat as it gets.

This sideway grind means bonds are holding onto the best levels of the year, as the price of mortgage rates fell 205 basis points in the last two months.

The LendZen Index monitors the change in price across a broad set of rates and mortgage bond coupons, whereas the LendZen Mortgage Rate Price Tracker is more “rate and loan program” specific.

Both are an example of how mortgage rates do not rise or fall, but instead it is their price that changes.

See Friday’s price tracker results on this Substack post.

Some substantial improvements in the last 3 weeks, with prices falling between 40 - 80 basis points for rates in the sub-6% range.

MORTGAGE SPREADS 🧈

-------------------------

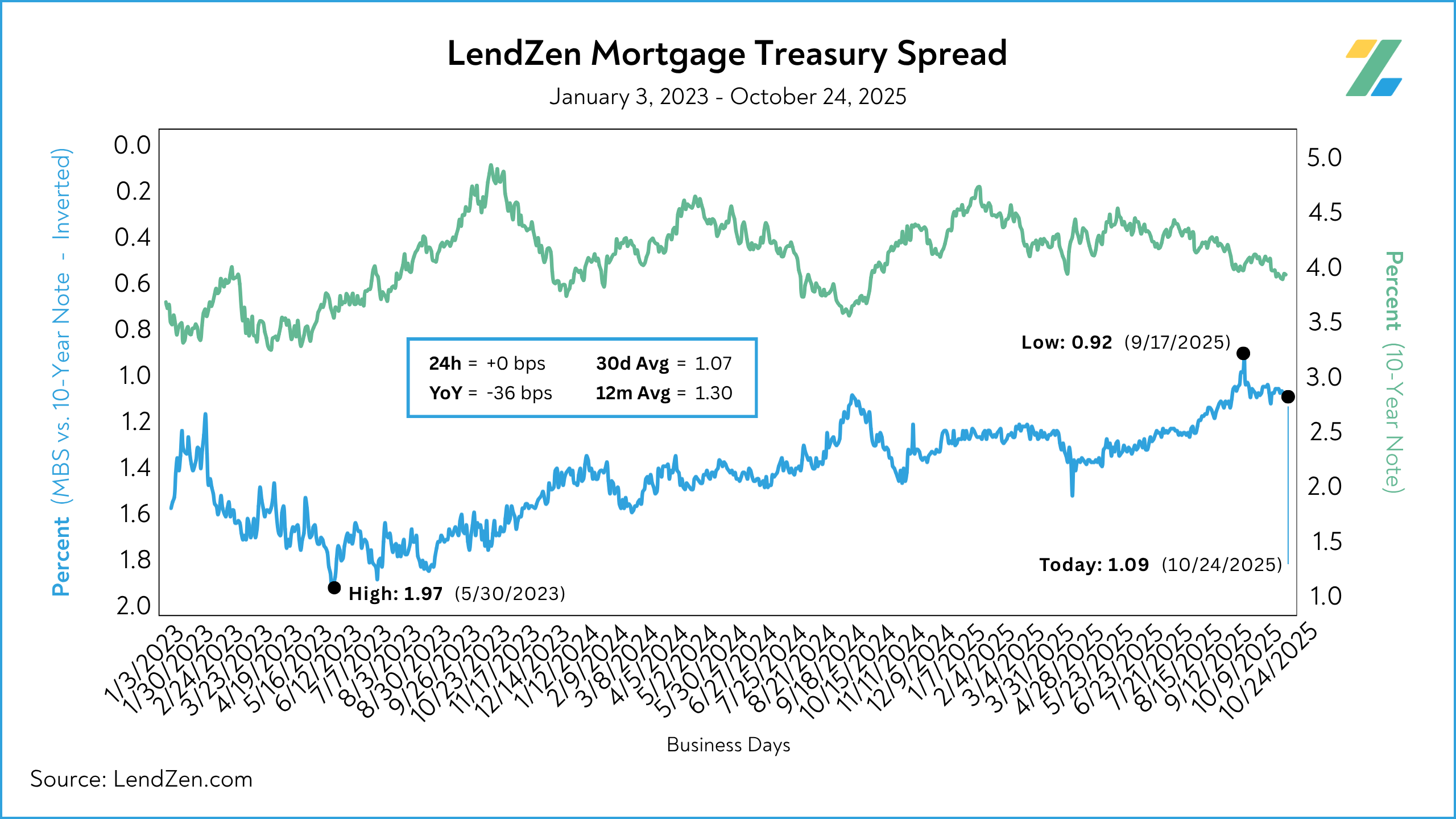

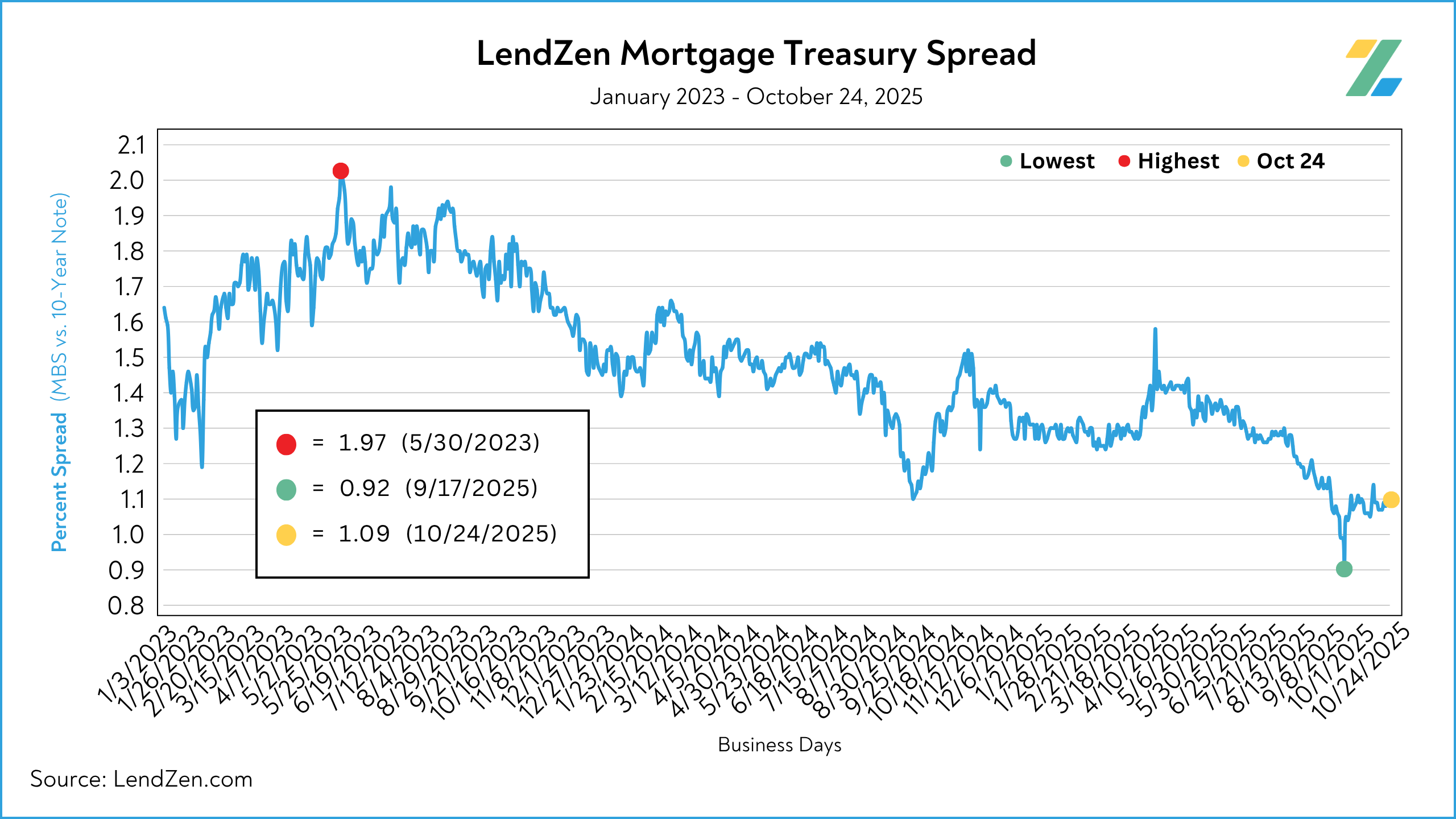

Published daily with the LendZen Index is the LendZen Mortgage-Treasury Spread.

The LMTS uses actual bond yields to create a historically consistent, and reliable, data set.

Learn more about the importance of accurately calculating spreads on this Substack post.

The spread between mortgage bonds and the U.S. 10-Year widened 2-bps at the start of the week and mostly stayed there throughout.

However, with a decline of 30 - 36 bps since last year, spreads have been the real story behind mortgage rates now versus 2024.

Oct 20 = 1.07

Oct 24 = 1.09

30d Avg = 1.07

12m Avg = 1.30

YoY = - 36 bps (1.45)

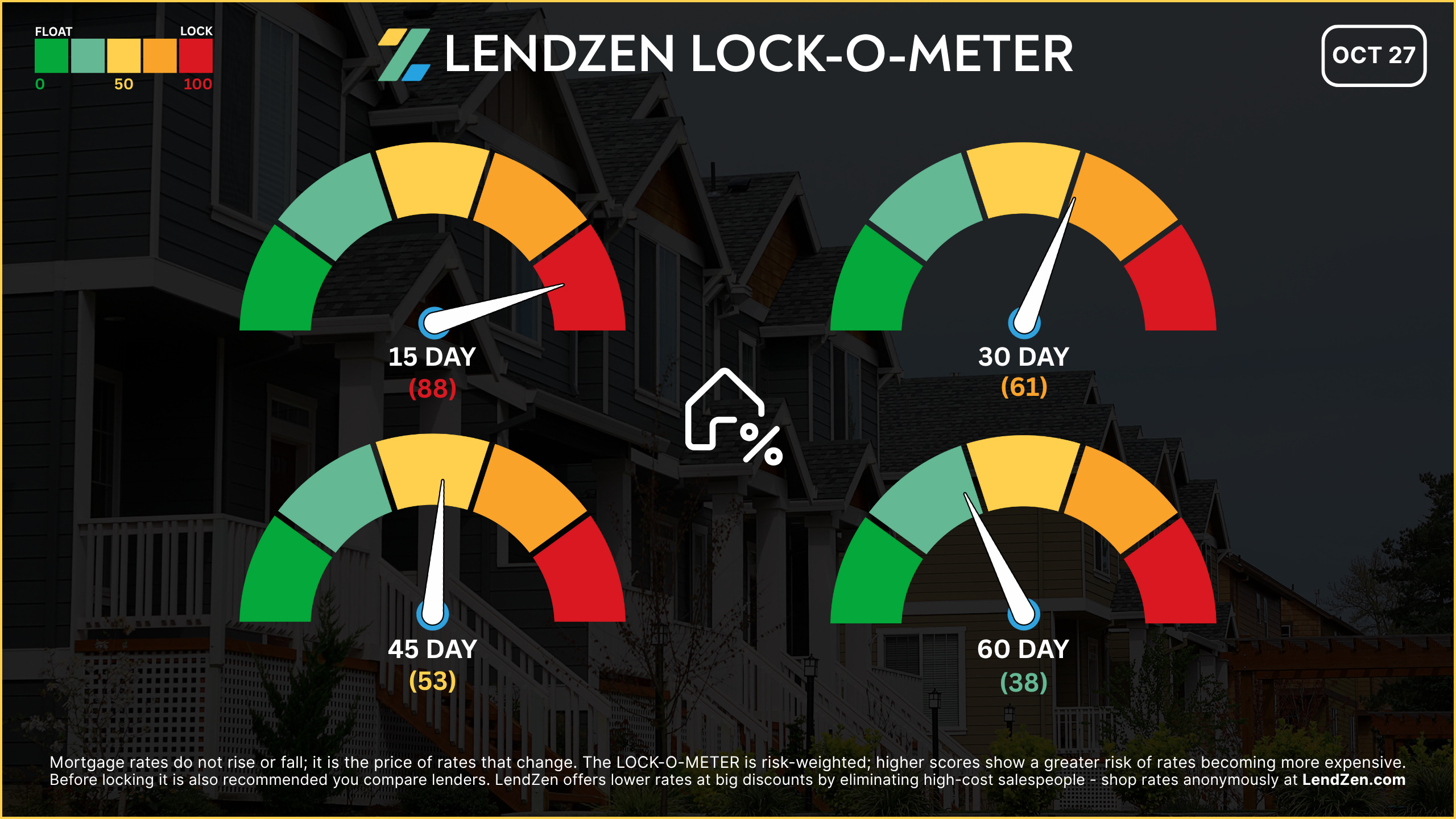

RATE LOCK GUIDE 🔒

---------------------

The LendZen LOCK-O-METER provides borrowers with a risk-weighted score based on how various macroeconomic events, including market data, central bank announcements, and geopolitics, each historically impacts the price of bonds.

higher risk scores = lean towards locking

------------------

Closing Window

------------------

[ 15 Days ] -- 88 🔴

CPI came and went, but uncertainty around GDP/PCE due to the shutdown adds to short-term risks. Although the Fed rate cut is priced in, Powell’s press conference remarks are not.

[ 30 Days ] -- 61 🟠

FOMC forward guidance will dominate short-term trajectory amidst a lockdown induced data desert. Float with alertness for sudden changes in market sentiment.

[ 45 Days ] -- 53 🟡

Unless data resumes in November bonds will be seeking unfamiliar corners of the economy for guidance. This doesn’t make for a confident float environment, but locking this far out seems extra conservative given the current bond friendly trend.

[ 60 Days ] -- 38 🟢

With more than 200 bps in mortgage rate price gains in the last 60-days (LendZen Index), the long-term bond trajectory favors floating. The ongoing stability, even in the face of all-time highs across various asset classes, gives us more than just a sliver of hope that a new bond bull market is emerging.

If you are already in a strong position, locking makes the most sense since the focus should be on making a savvy rate choice based on your longer-term rate outlook.

I expand on this “long game” approach in this Substack article.

Thanks for reading.

If you are interested in more mortgage insights, then I suggest checking out this recent Substack article.