Mortgage Rate Data Deluge 🏠📉🔒 (FEB 2)

Here is a deluge of mortgage rate data to start your week!

Included this week are the following sections:

MARKET RECAP ⏪

------------------

Last week bond markets had to navigate the FOMC rate decision (pause), silver’s manic rise and fall, not-so-friendly inflation data, and a Fed Chair nomination surprise.

The end result was a sideways grind that left mortgage bonds and mortgage rate prices only a tad better.

See more in the Rate Price Index section below.

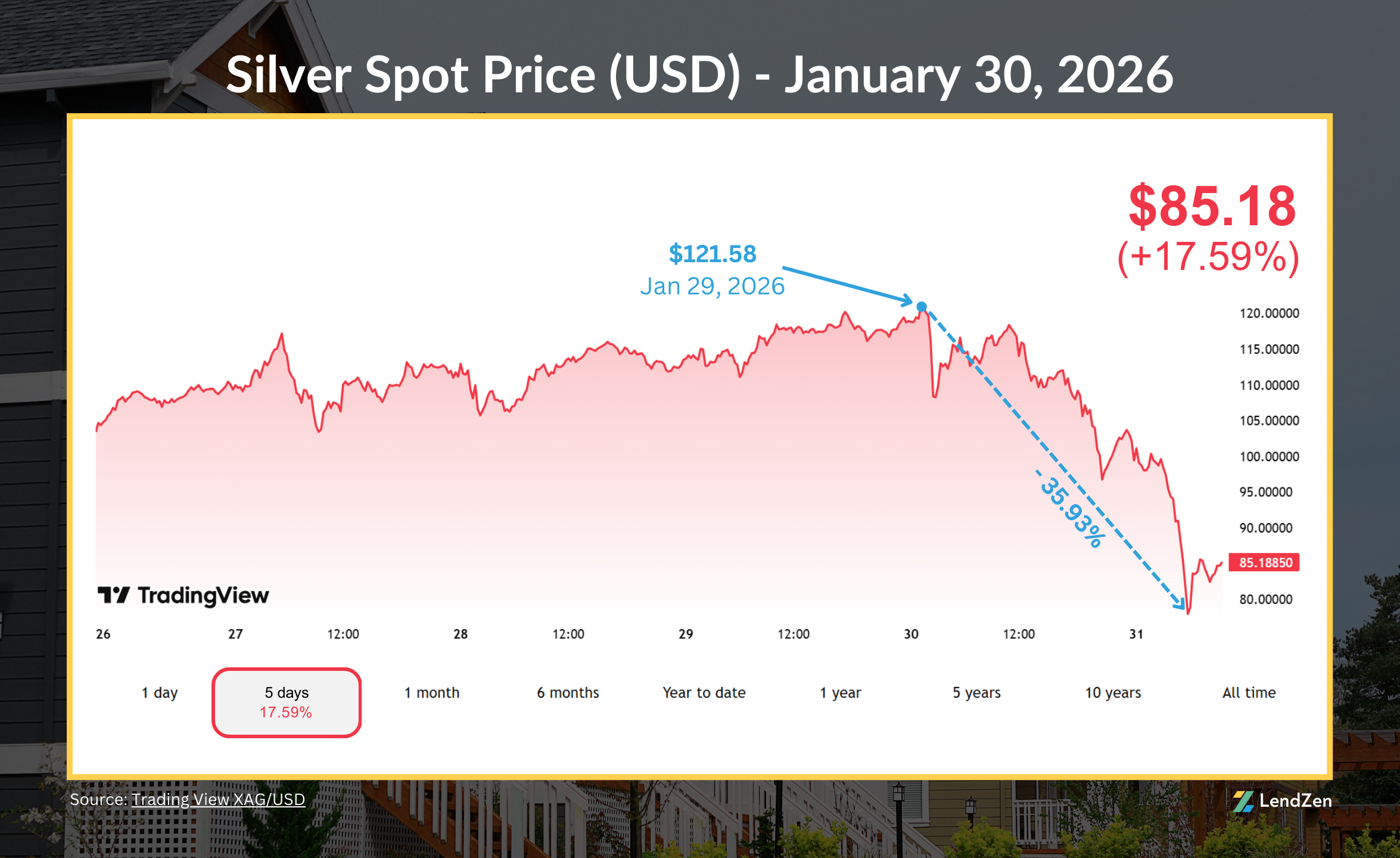

SILVER SLUMP 🪙

----------------

Silver traded like a meme coin last week, crashing 36% in a day.

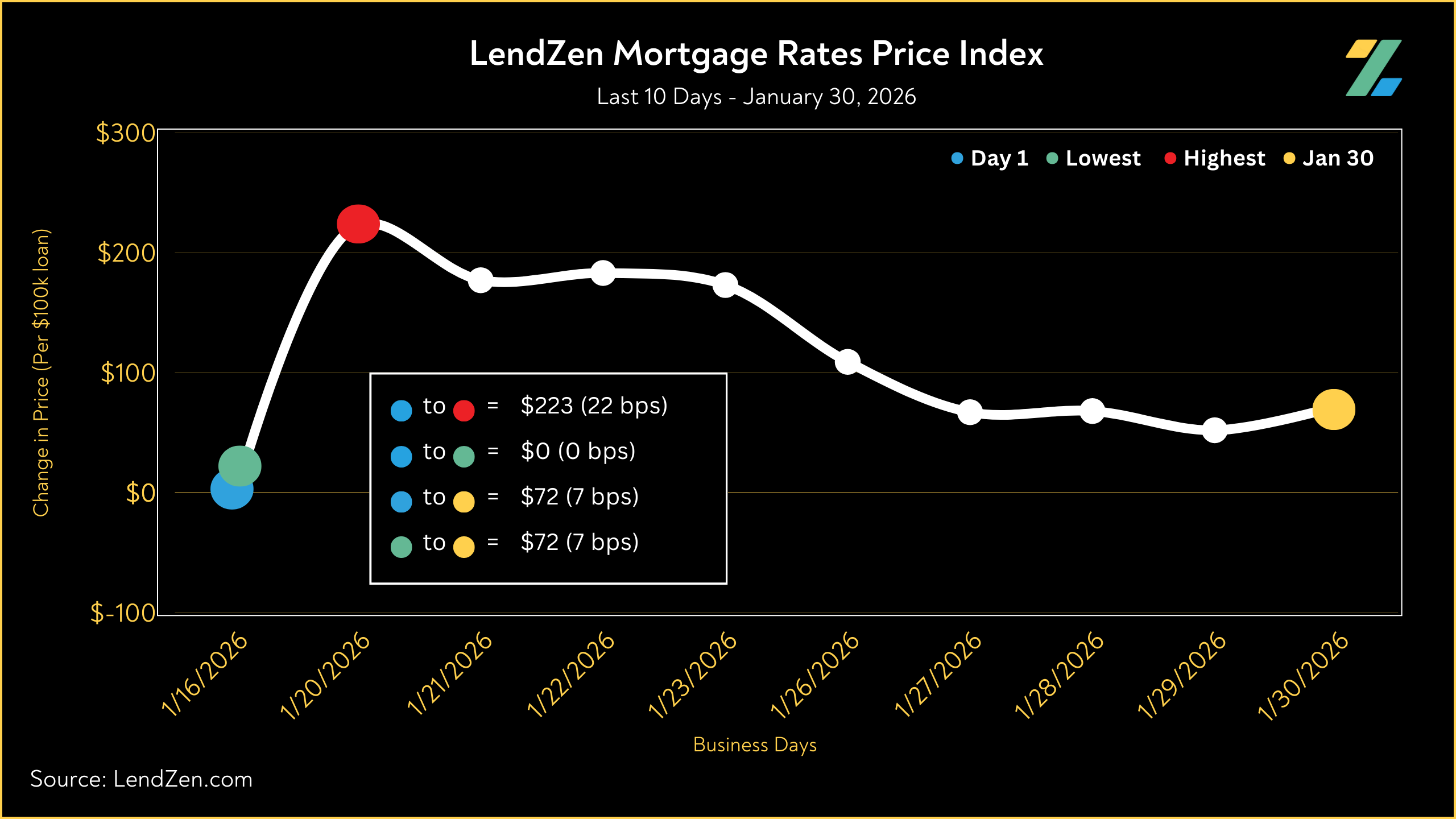

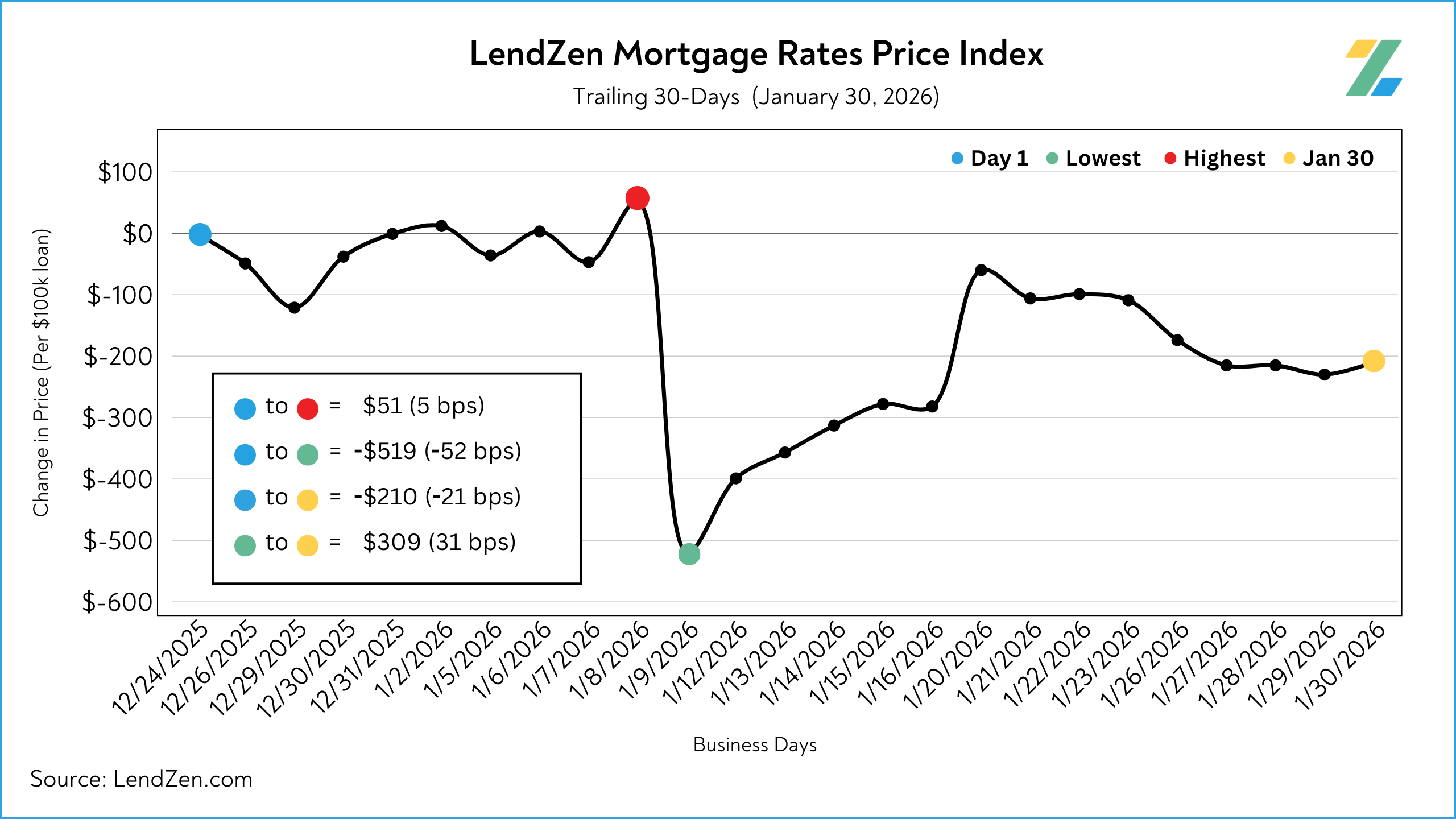

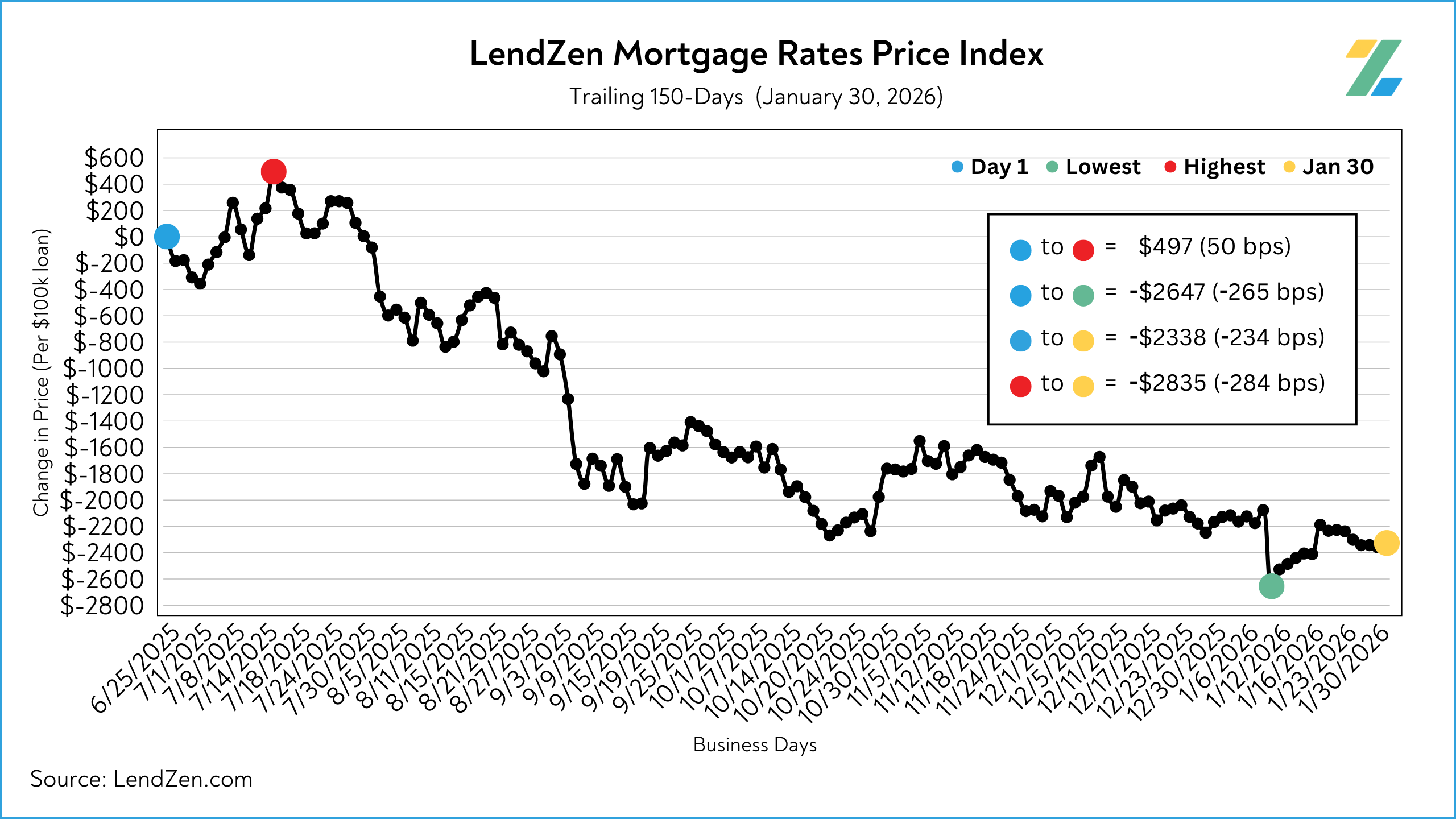

RATE PRICE INDEX 📉

----------------------

Mortgage rates DO NOT rise or fall.

The full range of rates is always available, and instead the price of each rate changes based on the trading of individual mortgage bonds.

The LendZen Index calculates a daily change in the price of mortgage rates by tracking a spectrum of mortgage-backed securities (MBS).

This provides borrowers with a more specific measurement of how the cost to obtain a mortgage is changing, regardless of the lender, rate, or credit score.

-----------

01/30/2026

-----------

24-Hour: +2 bps ($20 per $100K)

5-Day: -4 bps ($37)

10-Day: +7 bps ($72)

30-Day: -21 bps (-$210)

60-Day: -56 bps (-$556)

120-Day: -155 bps (-$1549)

Mortgage rate prices have been grinding sideways even after The Fed rate pause decision.

Mortgage rates are still waiting for something more substantial than the sugar high of a Trump outburst.

The biggest moves in the last 150 days have come after Non-Farm Payroll reports.

Could this week be the next big move ... and in which direction?

THE TRACKER 🔭

----------------

The LendZen Index monitors the change in price across a broad set of rates and mortgage bond coupons, whereas the Mortgage Rate Price Tracker is more “rate and loan program” specific.

Both are an example of how mortgage rates do not rise or fall, but instead it is their price that changes.

Since the LendZen Index has a variety of time series, the MRPT focuses on the current month’s activity.

You can explore the full results from January Week 4 on this Substack post.

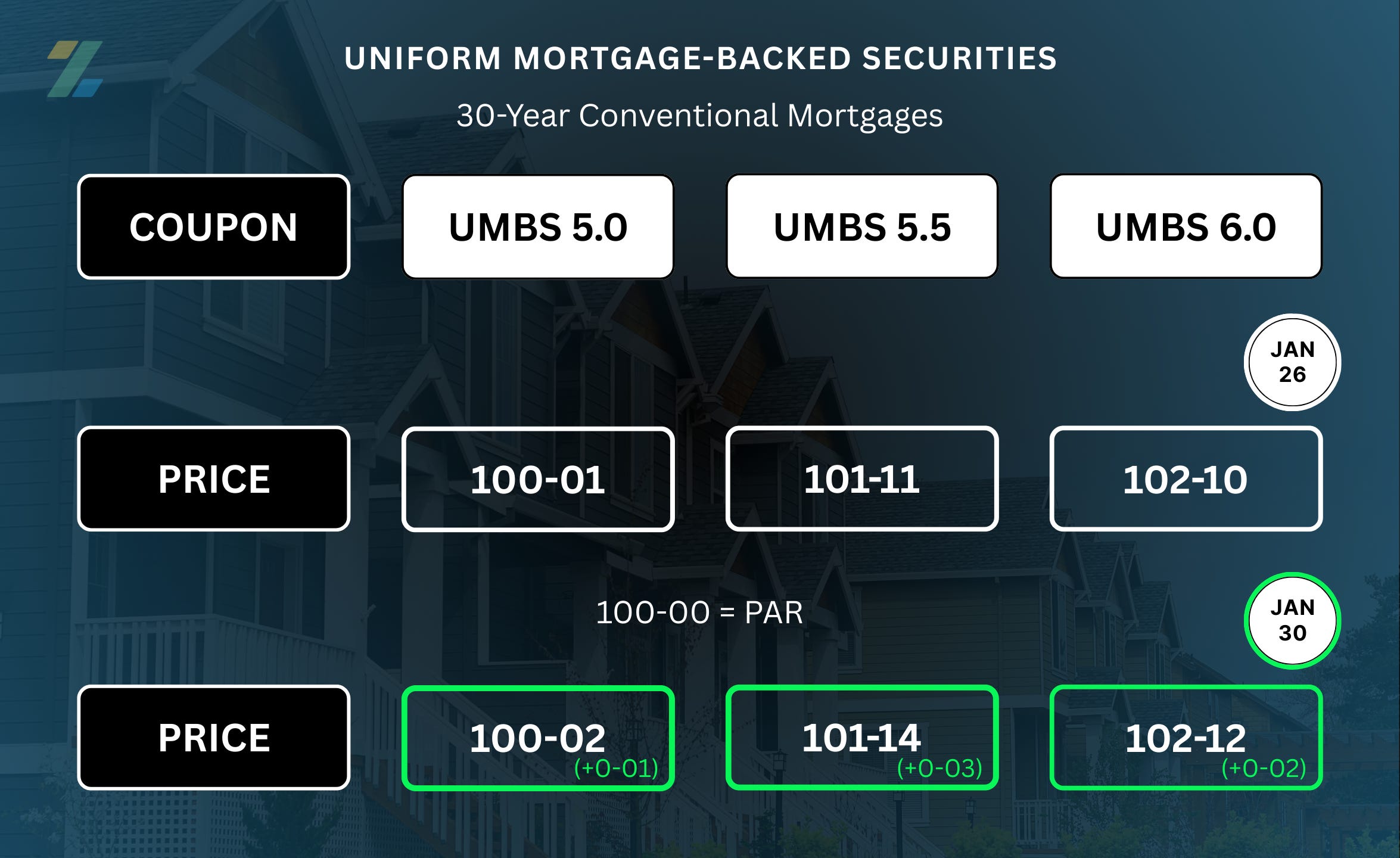

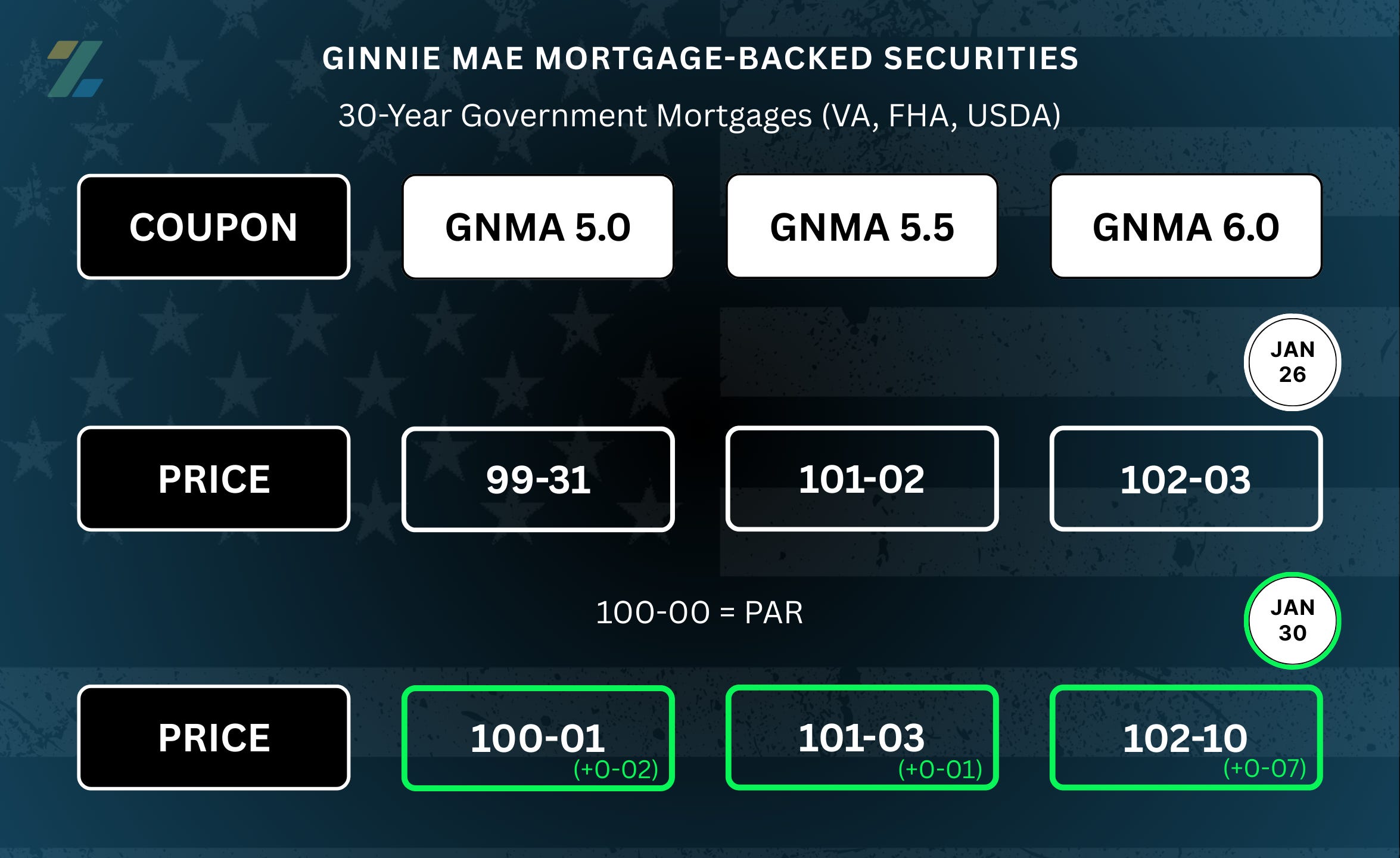

MBS PRICING 🏦

----------------

MBS coupons are sold at half-percent increments, while their price moves in 32nds (ticks).

ex. (0-04) = 4/32 = 12.5 bps

100-00 acts as the starting line, also referred to as PAR.

The higher the coupon price, the less expensive the rates will be that are sold into that security.

Therefore, an increase in the price of mortgage bonds is good for mortgage rates.

Learn more about the dynamics of MBS pricing and how it impacts your mortgage options in any of the bi-weekly “Rate Snapshot” Substack posts.

Mortgage bond prices have been relatively tame despite increased volatility in other asset classes, including precious metals.

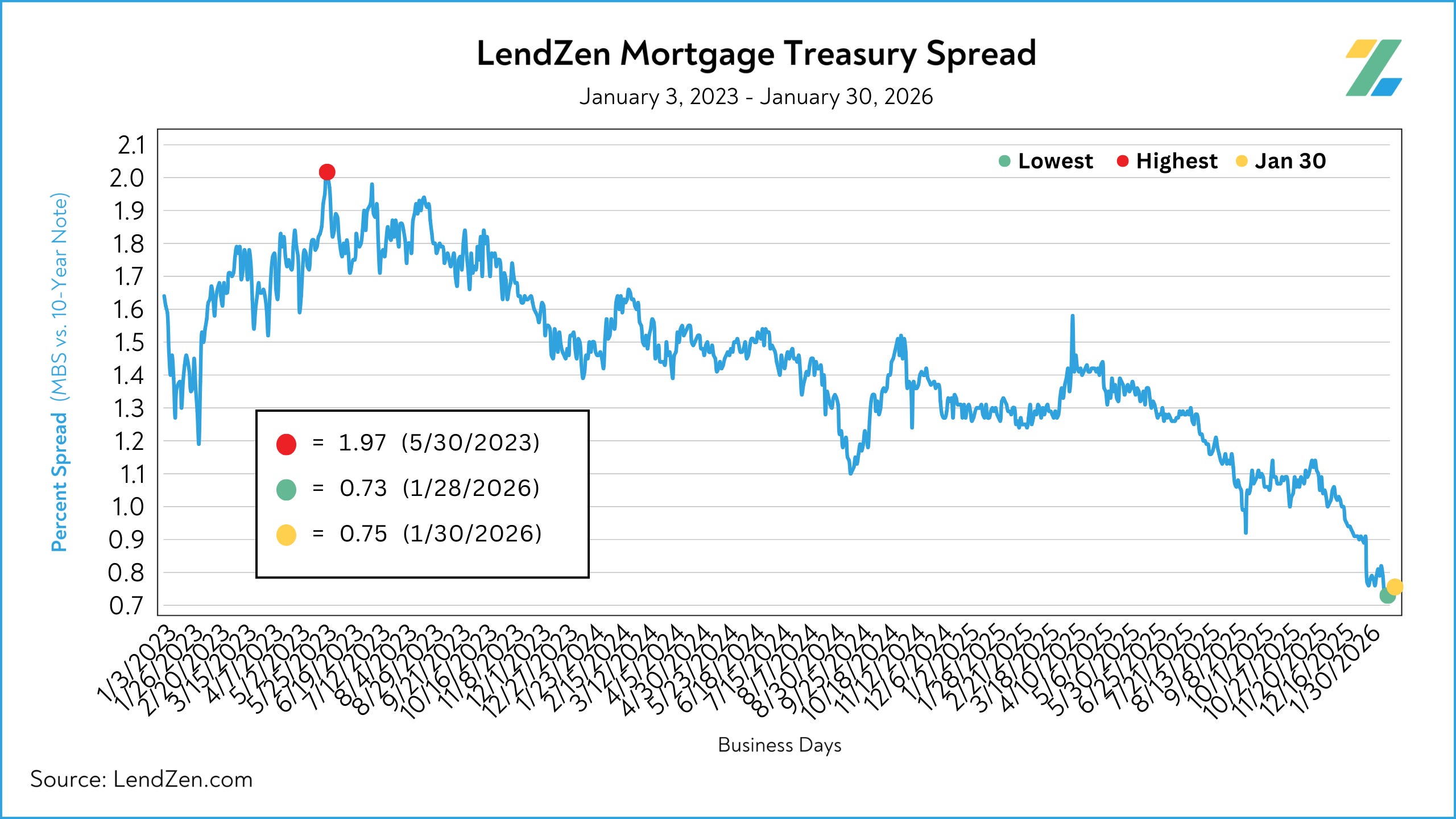

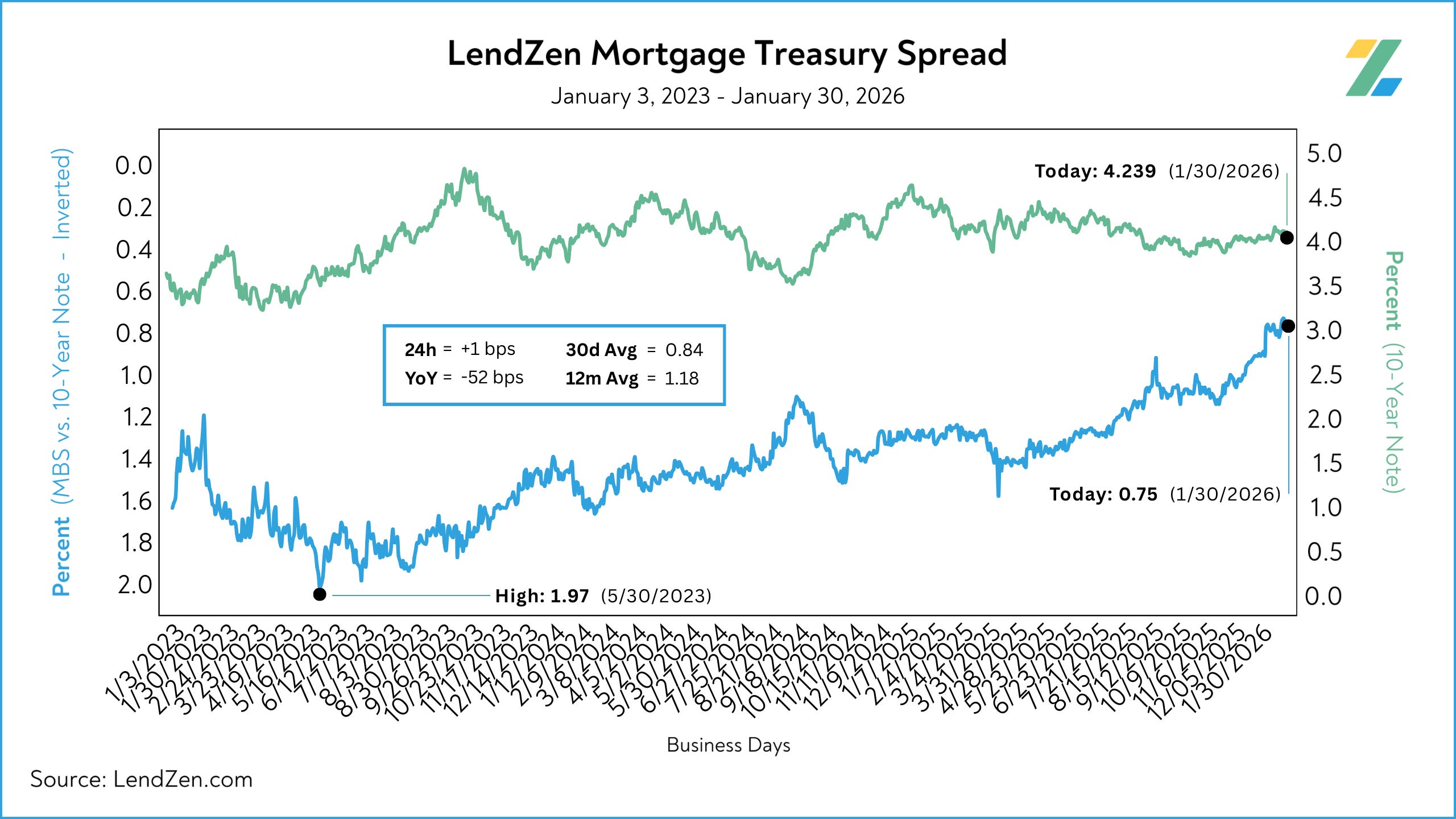

MORTGAGE SPREADS 🧈

-------------------------

Published daily with the LendZen Index is the LendZen Mortgage-Treasury Spread.

The LMTS uses actual bond yields to create a historically consistent, and reliable, data set.

Learn more about the importance of accurate mortgage spreads on this Substack post.

-----------

01/30/2026

-----------

Jan 26: 0.79

Jan 30: 0.75

5d: -4 bps

30d Avg: 0.84

12m Avg: 1.18

YoY: -52 bps

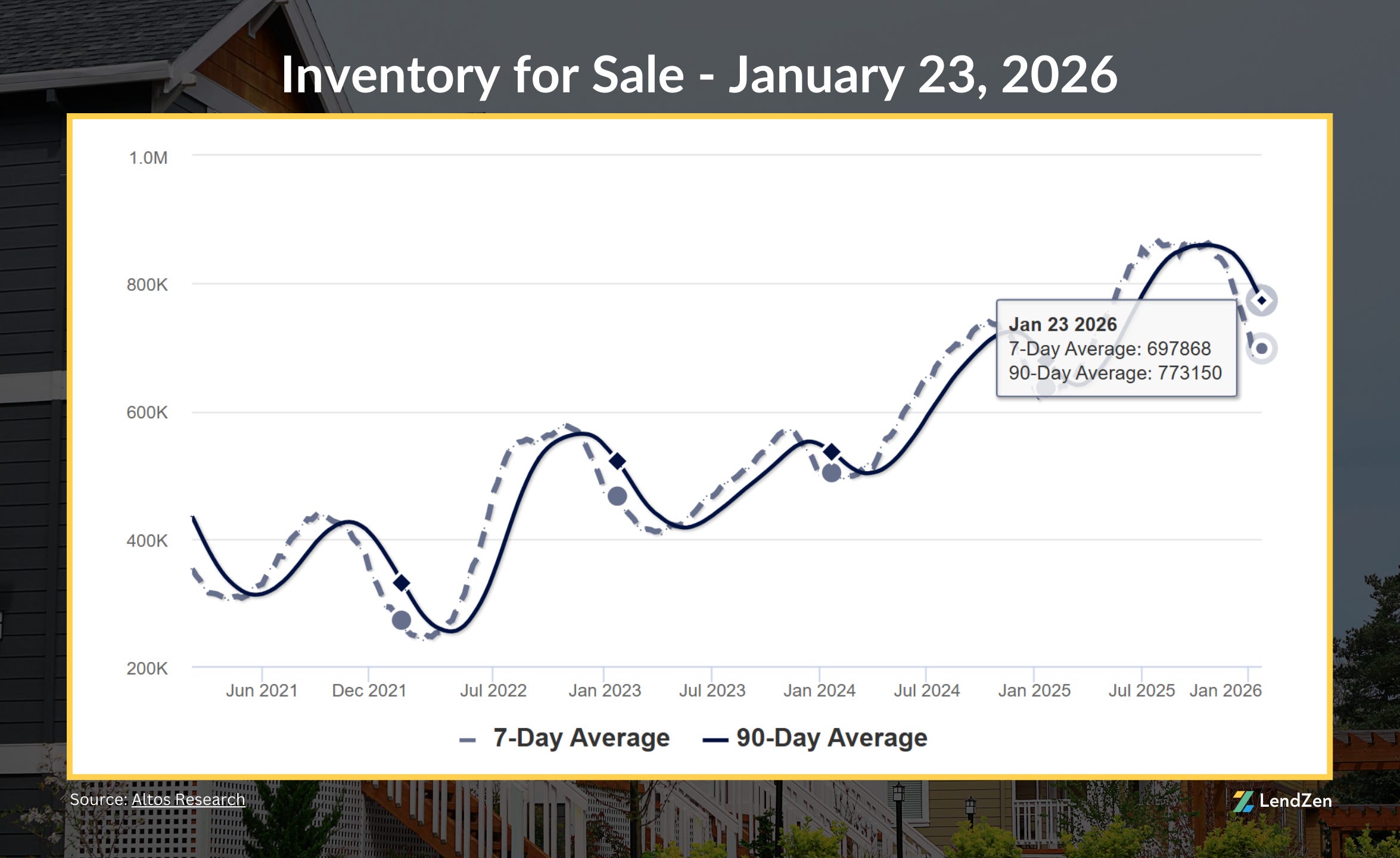

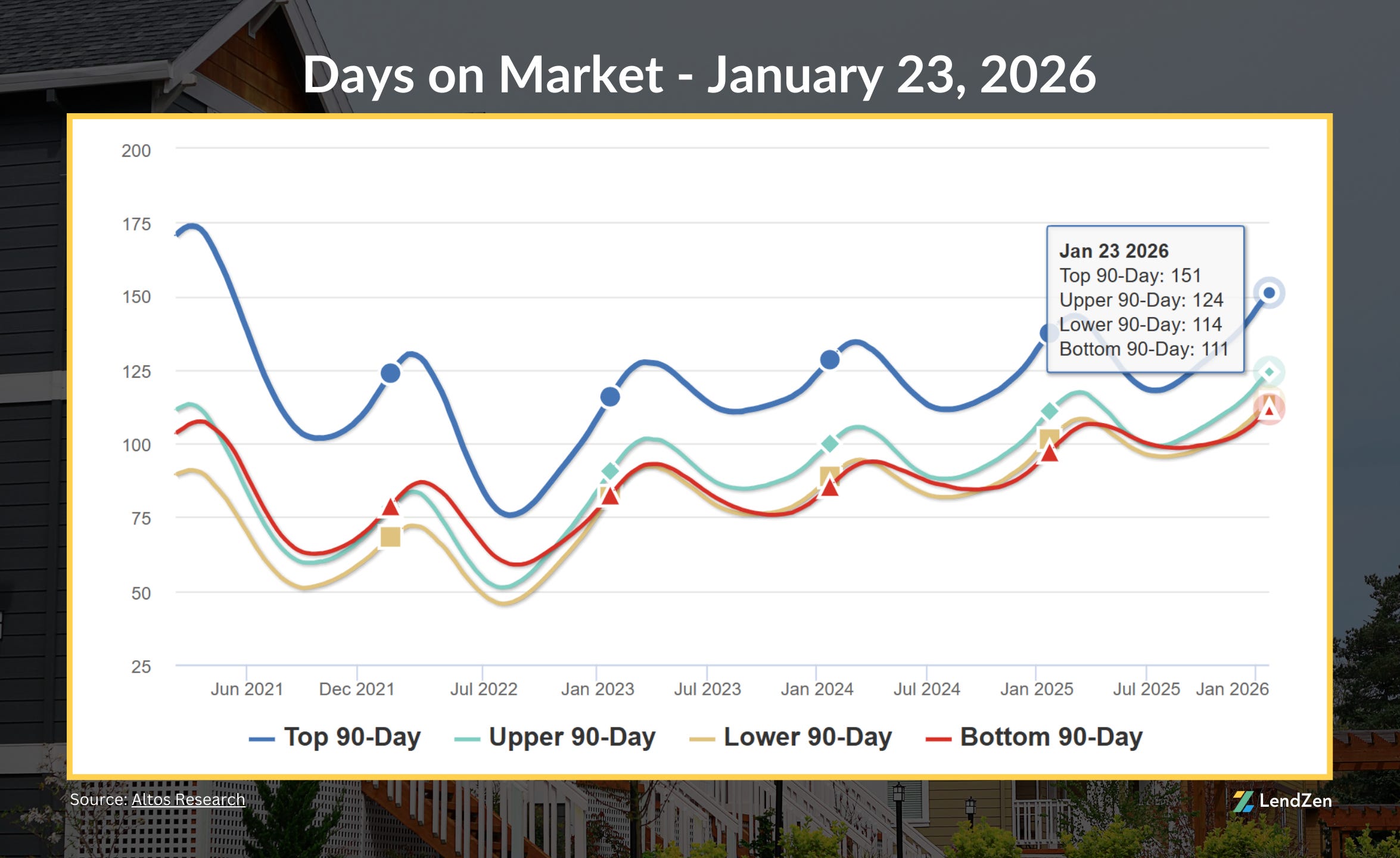

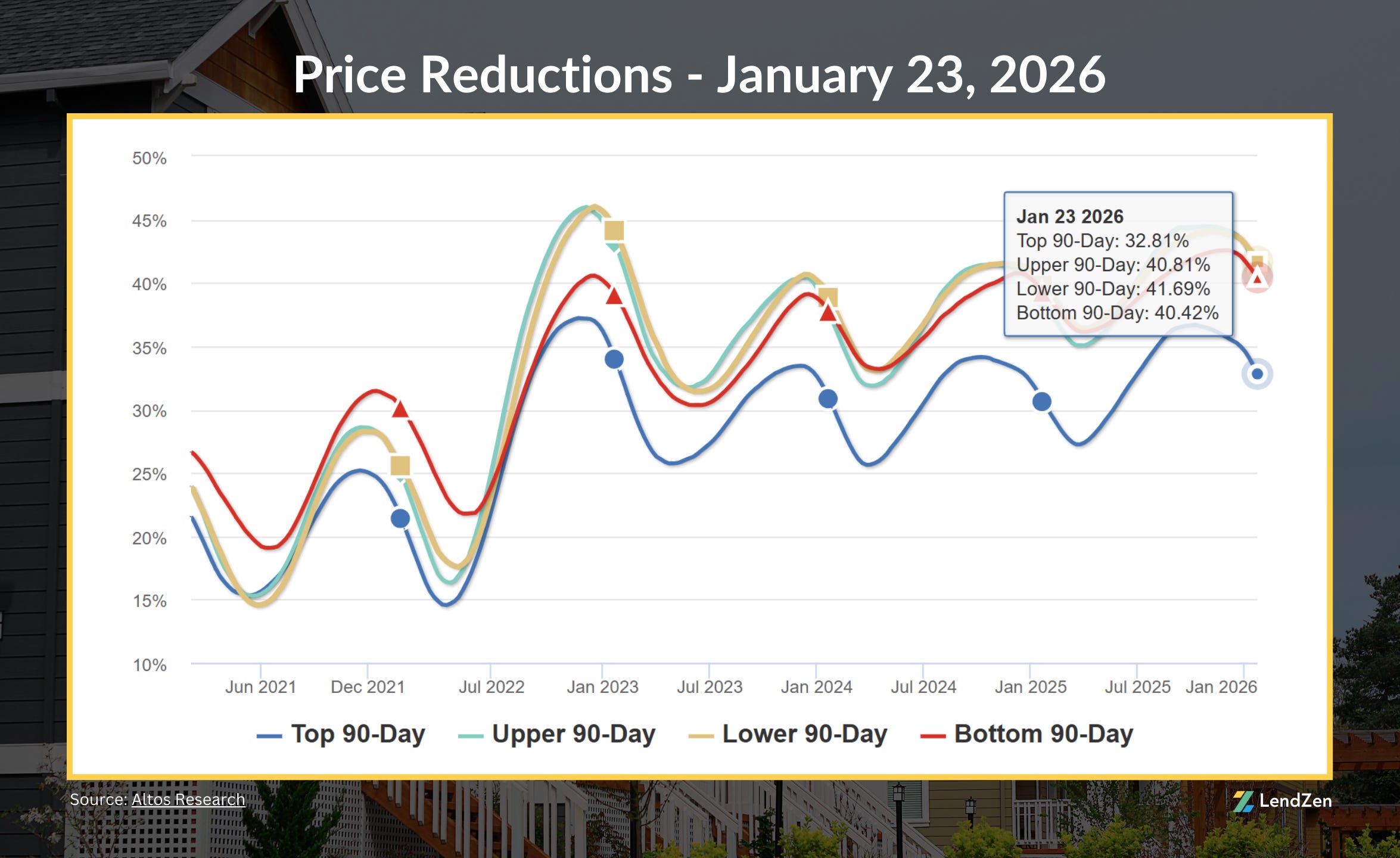

HOUSING DATA 🏠

------------------

Here are the latest housing market stats, with trends from the last 90 days.

The U.S. median list price is $419,900, a slight notch up from the previous week.

Inventories ticked up again ever-so-slightly.

Days on market was unchanged with an average of 133.

Price reductions softened again with the 90-day national average dipping below 34%.

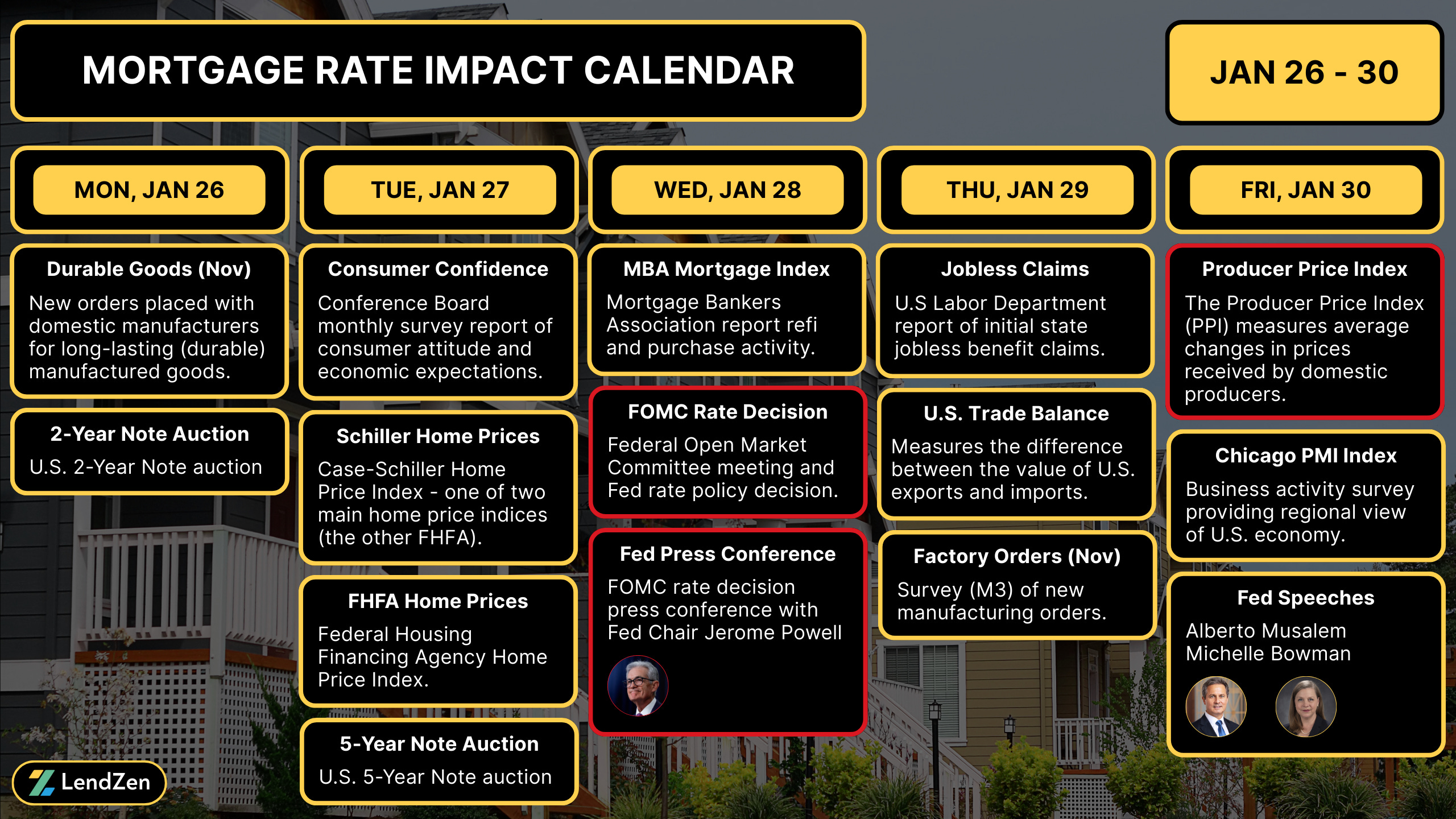

WEEK AHEAD 📅

----------------

There is a triple threat of employment data starting on Wednesday with ADP payrolls, Challenger layoffs and Jobless Claims on Thursday, and the heavy-hitting Non-Farm Payroll (NFP) employment report on Friday.

Read more in yesterday’s Week Ahead.

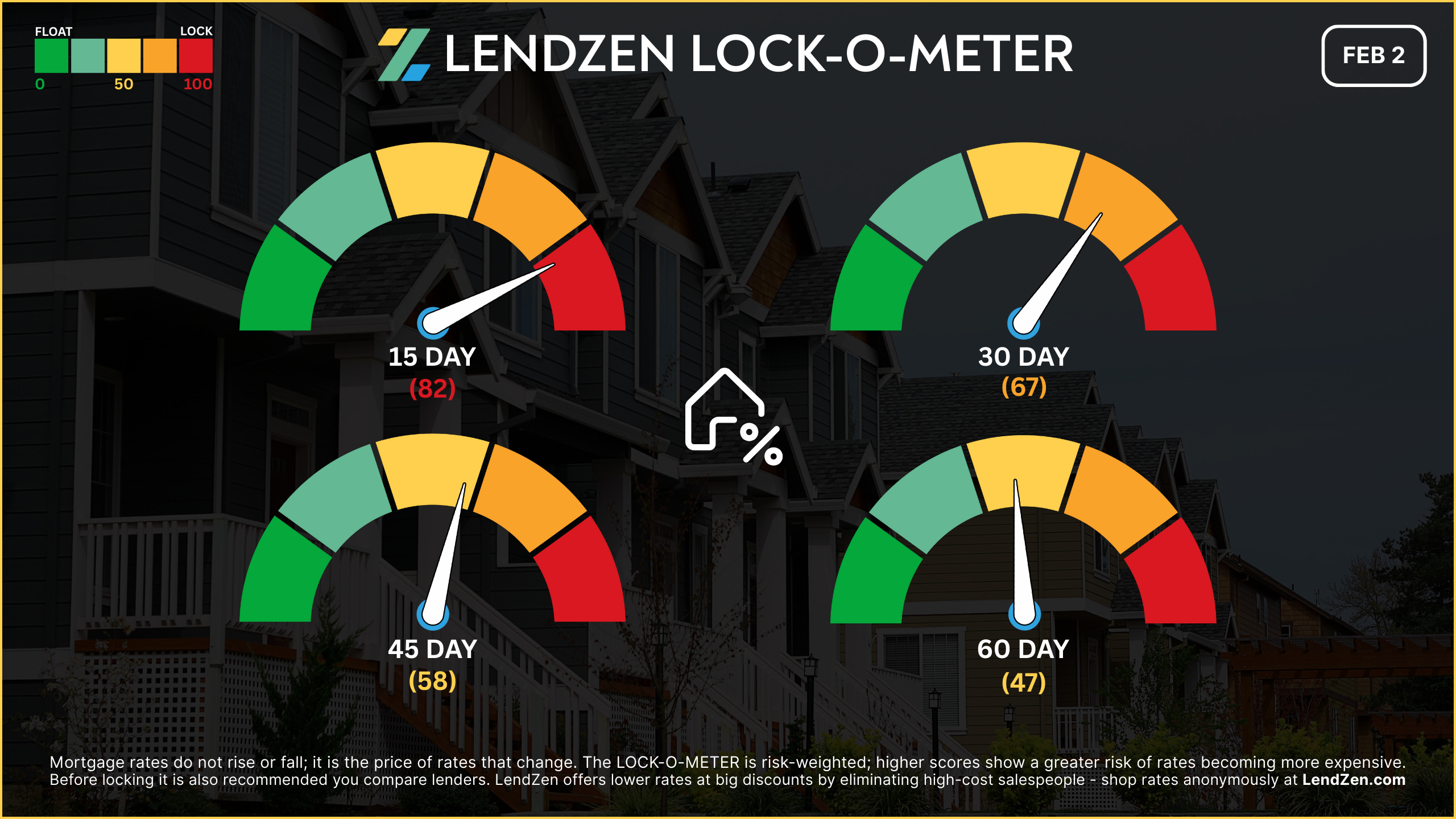

RATE LOCK GUIDE 🔒

---------------------

The LendZen LOCK-O-METER provides borrowers with a risk-weighted score based on how various macroeconomic events, including market data, central bank announcements, and geopolitics, each historically impacts the price of bonds.

higher risk scores = lean towards locking

------------------

Closing Window

------------------

[ 15 Days ] -- 82 🔴

Bonds are coming off a flat week and sitting near multi-year best mortgage pricing, but we’re heading into the heaviest employment/data cluster of the month (ISM, JOLTS, ADP, NFP). Plus, fresh tensions in Iran and a surprise Fed-chair nominee. That’s a lot of ways for mortgage rate prices to get more expensive in a hurry, with limited room left for recovery.

[ 30 Days ] -- 67 🟠

Over the next month, markets will digest this week’s employment deluge while continuing to reprice what the Fed path looks like under a potential Chairman Warsh. The LendZen Index shows mortgage pricing is significantly cheaper than 150 days ago, but recent volatility points towards locking for price sensitive borrowers.

[ 45 Days ] -- 58 🟡

Most (if any) employment data shock and Fed-chair headlines should be absorbed. The other “Big 3” events (CPI/PCE, FOMC) sit further out on the horizon. There’s still calendar event risk, but geopolitics is the wild card to watch.

[ 60 Days ] -- 47 🟡

The risk/reward tilts towards floating as the overall macro backdrop remains bond friendly.

If you are already in a strong position locking generally makes the most sense, especially for shorter windows, since the focus should be on making a savvy rate choice based on your longer-term rate outlook.

I expand on this “long game” approach in this Substack post.

Thanks for reading.

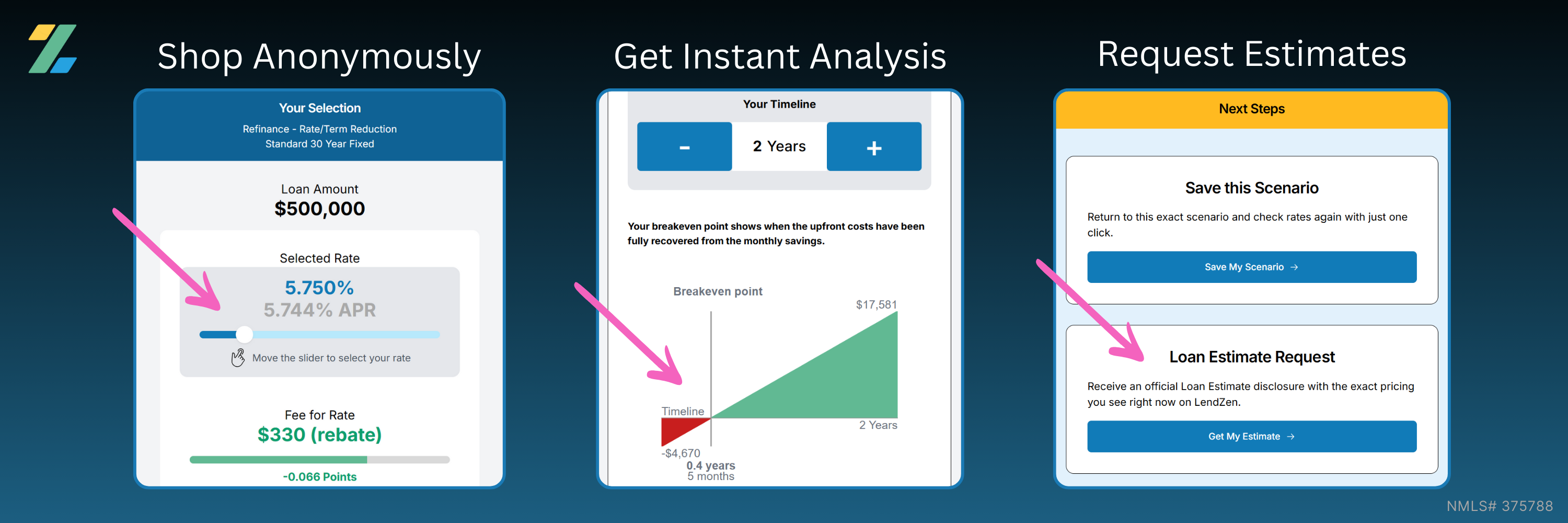

If you want to shop real-time mortgage rates and get instant qualification results without providing any contact information visit LendZen.com

LendZen provides a fully automated mortgage shopping experience that gives you anonymous access to all mortgage rates with full transparency of costs upfront as bond prices change.

You can also request an official Loan Estimate for the exact loan you created and save your scenario to revisit your rate options daily with one-click.

LendZen Inc. is an equal opportunity mortgage lender, NMLS 375788.