Mortgage Rate Data Deluge 🏠📉🔒 (DEC 15)

Here is a deluge of mortgage rate data to start your week!

Included in this week’s deluge are the following sections:

MARKET RECAP ⏪

------------------

Despite the anticipation and high hopes for a Fed rate cut fueled bond rally, nothing meaningful materialized.

Although the knee-jerk reaction on Wednesday was positive, with some spill-over into Thursday, the net-gain when combined with Friday’s slightly lower bond prices and the soft start to week, left things mostly unchanged (to worse).

SILVER SHINES ✨

-----------------

Silver shines while Bitcoin continues to slide, down 30% from the all-time highs.

What are markets telling us ... are both acting as the canary in the coal mine?

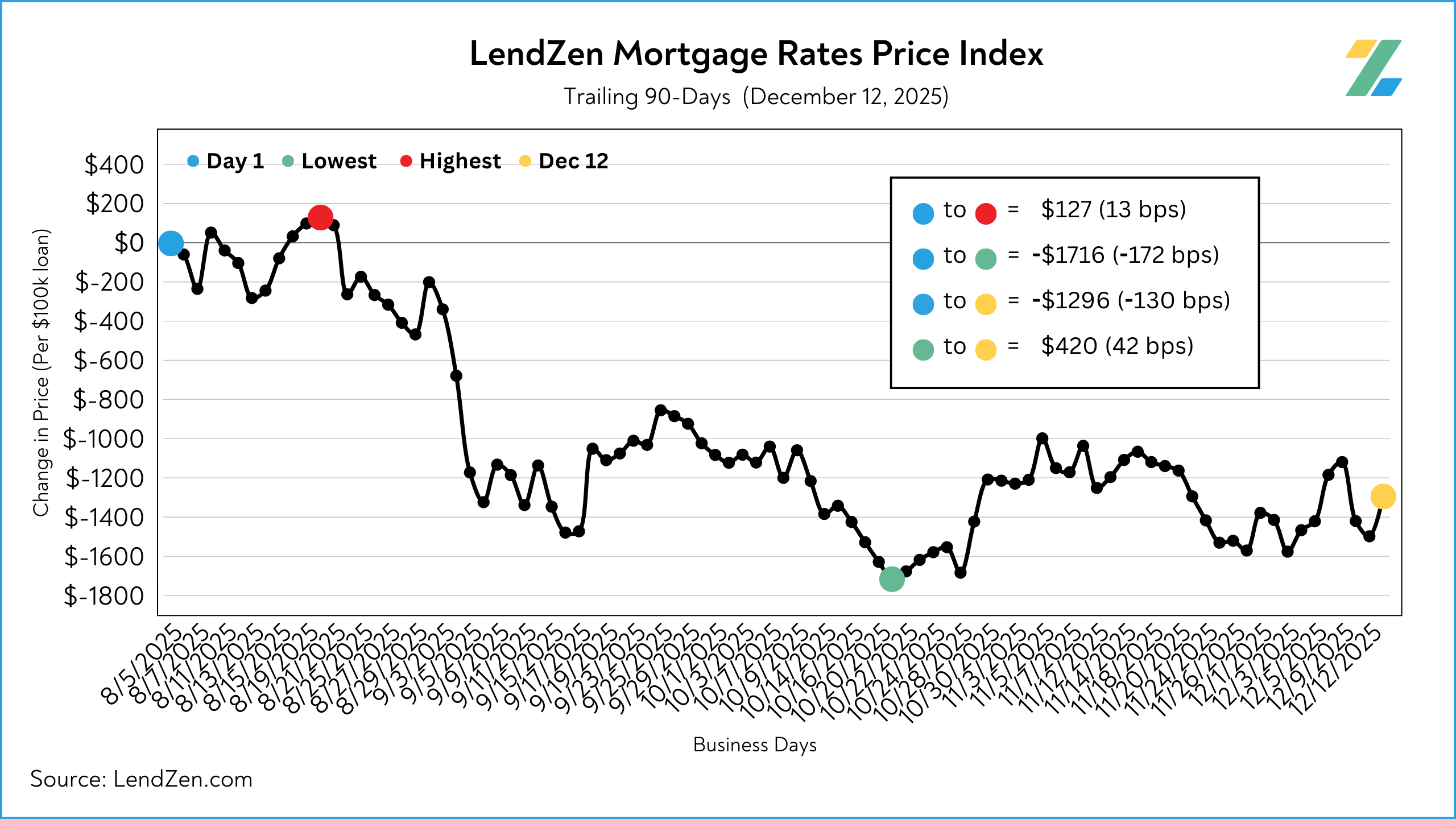

RATE PRICE INDEX 📉

----------------------

Mortgage rates DO NOT rise or fall.

The full range of rates is always available, and instead the price of each rate changes based on the trading of individual mortgage bonds.

The LendZen Index calculates a daily change in the price of mortgage rates by tracking a spectrum of mortgage-backed securities (MBS).

This provides borrowers with a more specific measurement of how the cost to obtain a mortgage is changing, regardless of the lender, rate, or credit score.

-----------

12/12/2025

-----------

24-Hour: +20 bps ($202 per $100K)

5-Day: -11 bps (-$111)

10-Day: +8 bps ($83)

30-Day: -9 bps (-$88)

60-Day: +18 bps ($177)

Although mortgage rate prices found a new low for the year on October 21, not much has been achieved since the big August NFP bond rally with bonds and mortgage rates in a choppy sideways pattern.

However, since peaking on January 16, mortgage rate PRICES have declined by over 300 basis points.

That means the cost of getting a $500k mortgage (at any rate) is $15,000 cheaper today than at the start of the year.

In terms of positive change, this makes 2025 the best year for mortgage rates since 2020.

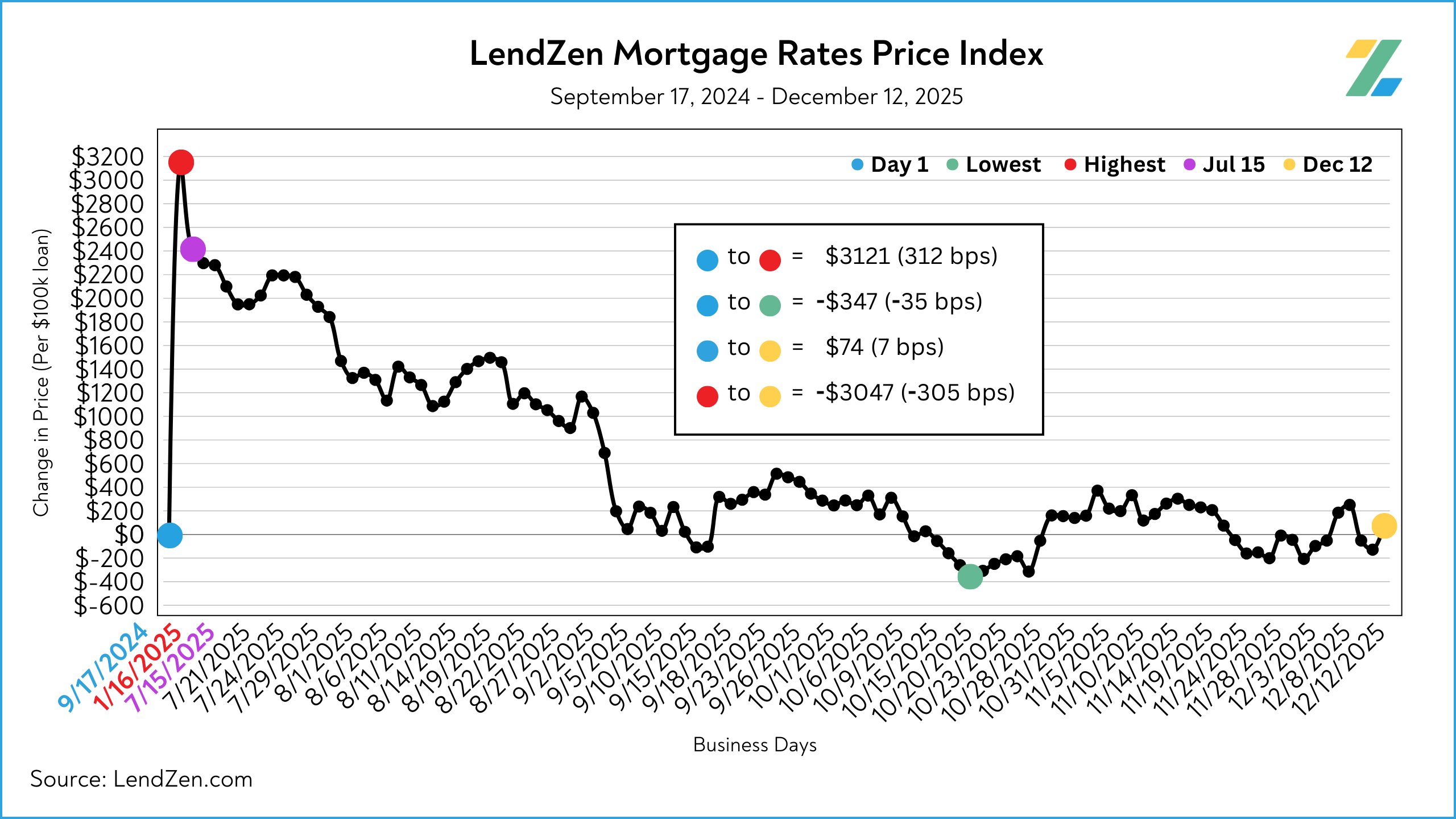

The LendZen Index monitors the change in price across a broad set of rates and mortgage bond coupons, whereas the Mortgage Rate Price Tracker is more “rate and loan program” specific.

Both are an example of how mortgage rates do not rise or fall, but instead it is their price that changes.

Since the LendZen Index has a variety of time series, the MRPT focuses on the current month’s activity.

You can explore the full results from December Week 2 on this Substack post.

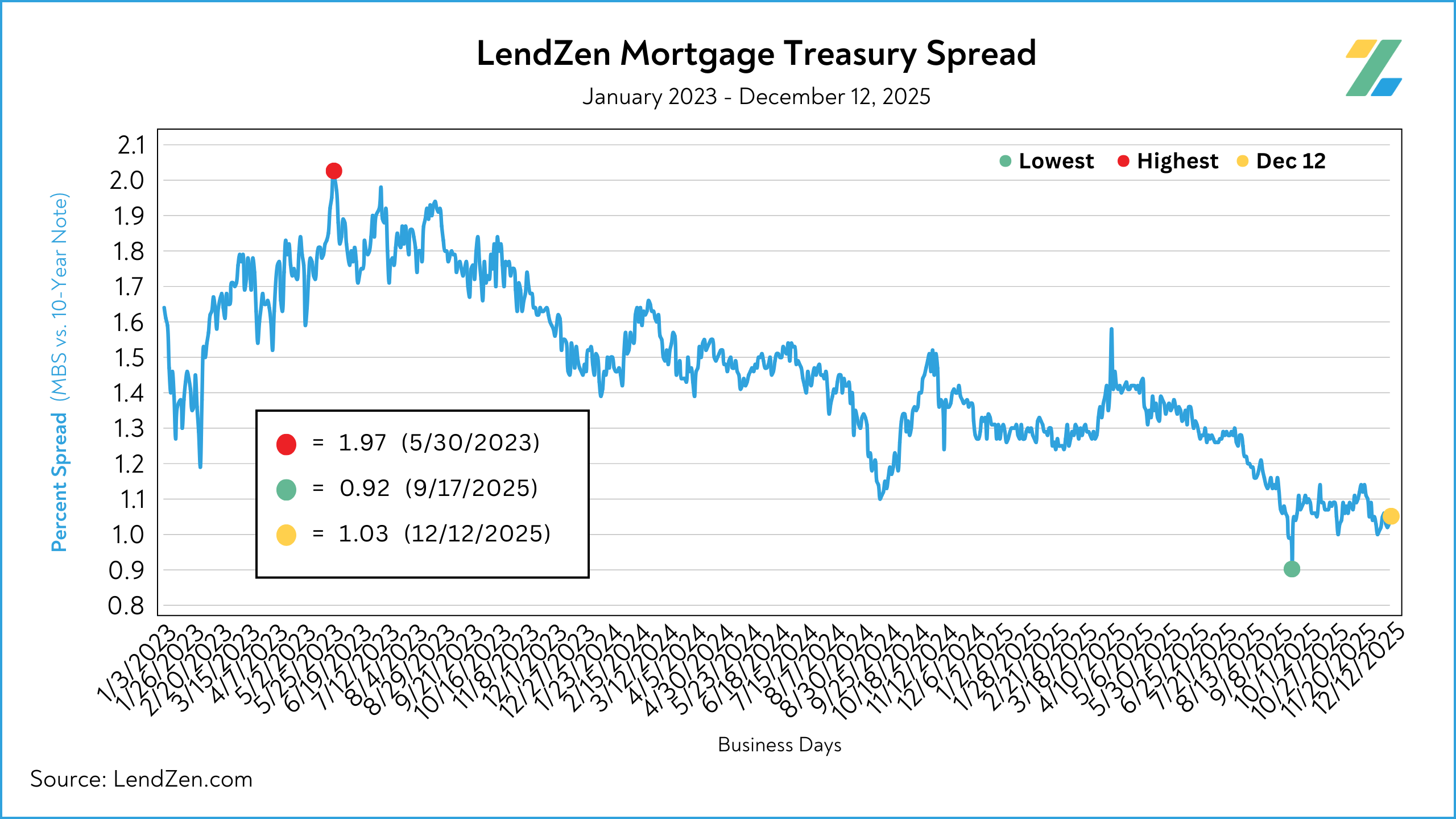

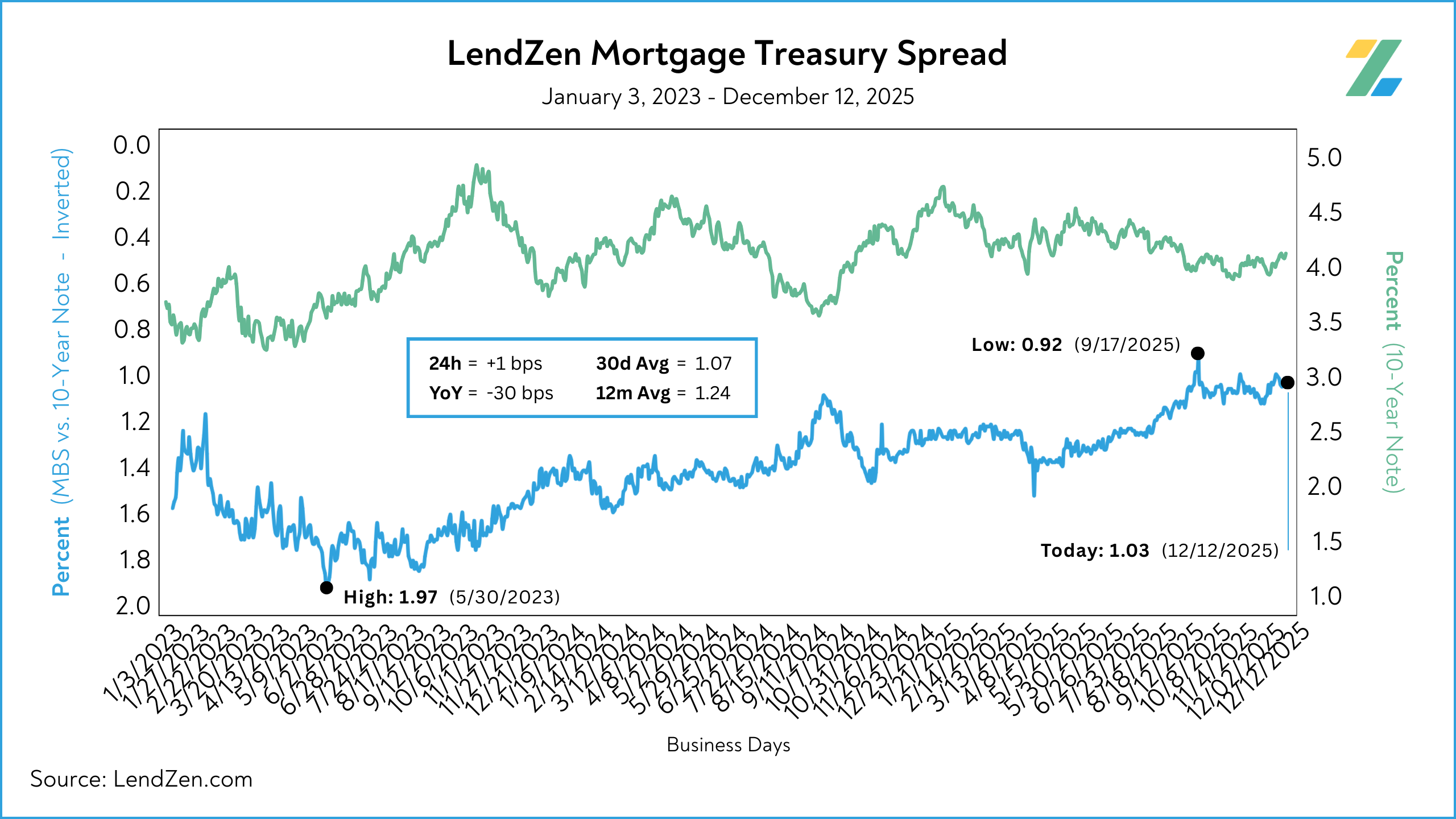

MORTGAGE SPREADS 🧈

-------------------------

Published daily with the LendZen Index is the LendZen Mortgage-Treasury Spread.

The LMTS uses actual bond yields to create a historically consistent, and reliable, data set.

Learn more about the importance of accurately calculating spreads on this Substack post.

The spread between mortgage bonds and the U.S. 10-Year tightened 2-bps during the week.

Dec 08: 1.05

Dec 12: 1.03

5d: -2 bps

30d Avg: 1.07

12m Avg: 1.24

YoY: -30 bps

With a decline of over 30 bps since last year, spreads have been the real story behind mortgage rates now versus 2024.

Get the full scoop in this recent Substack post.

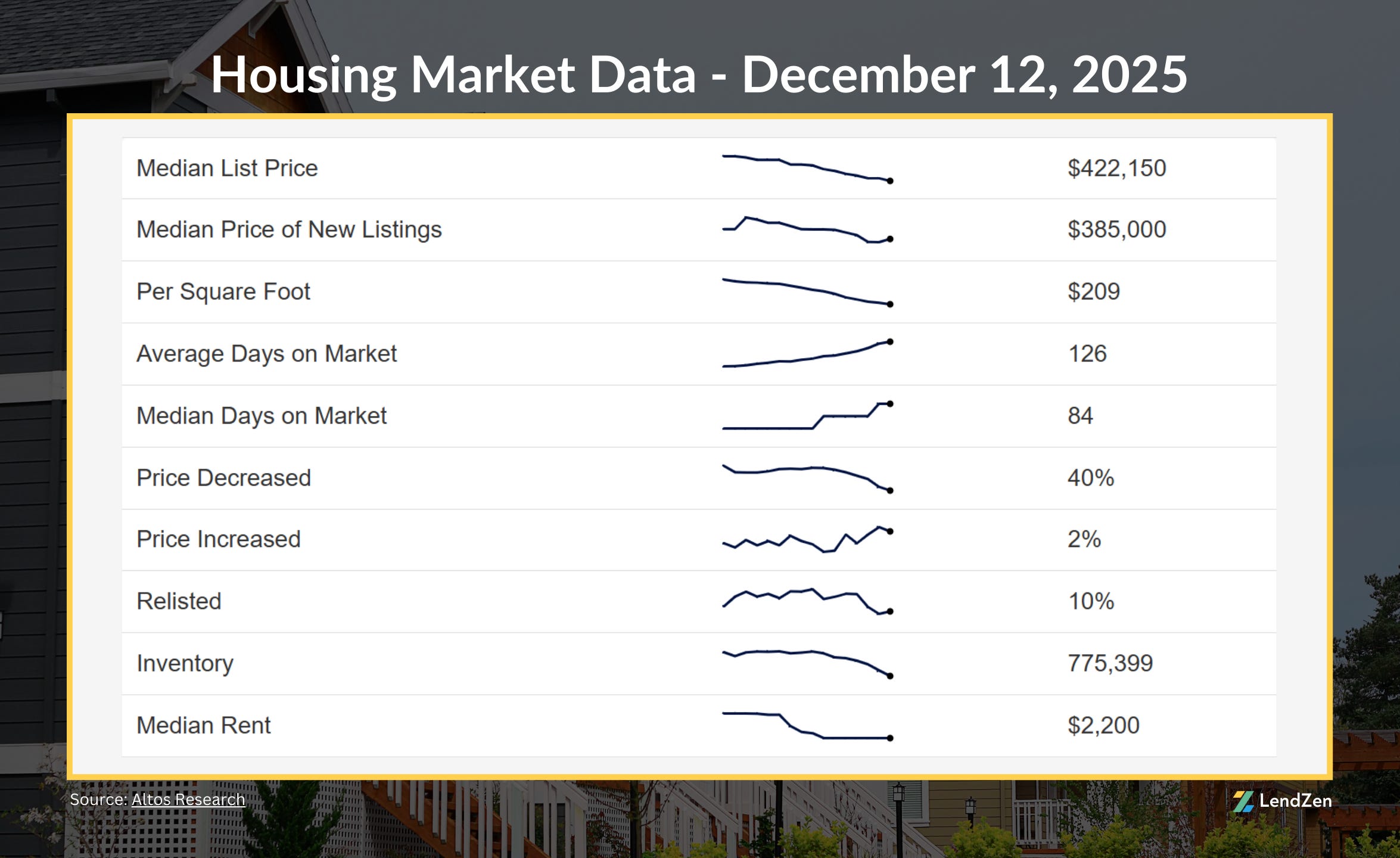

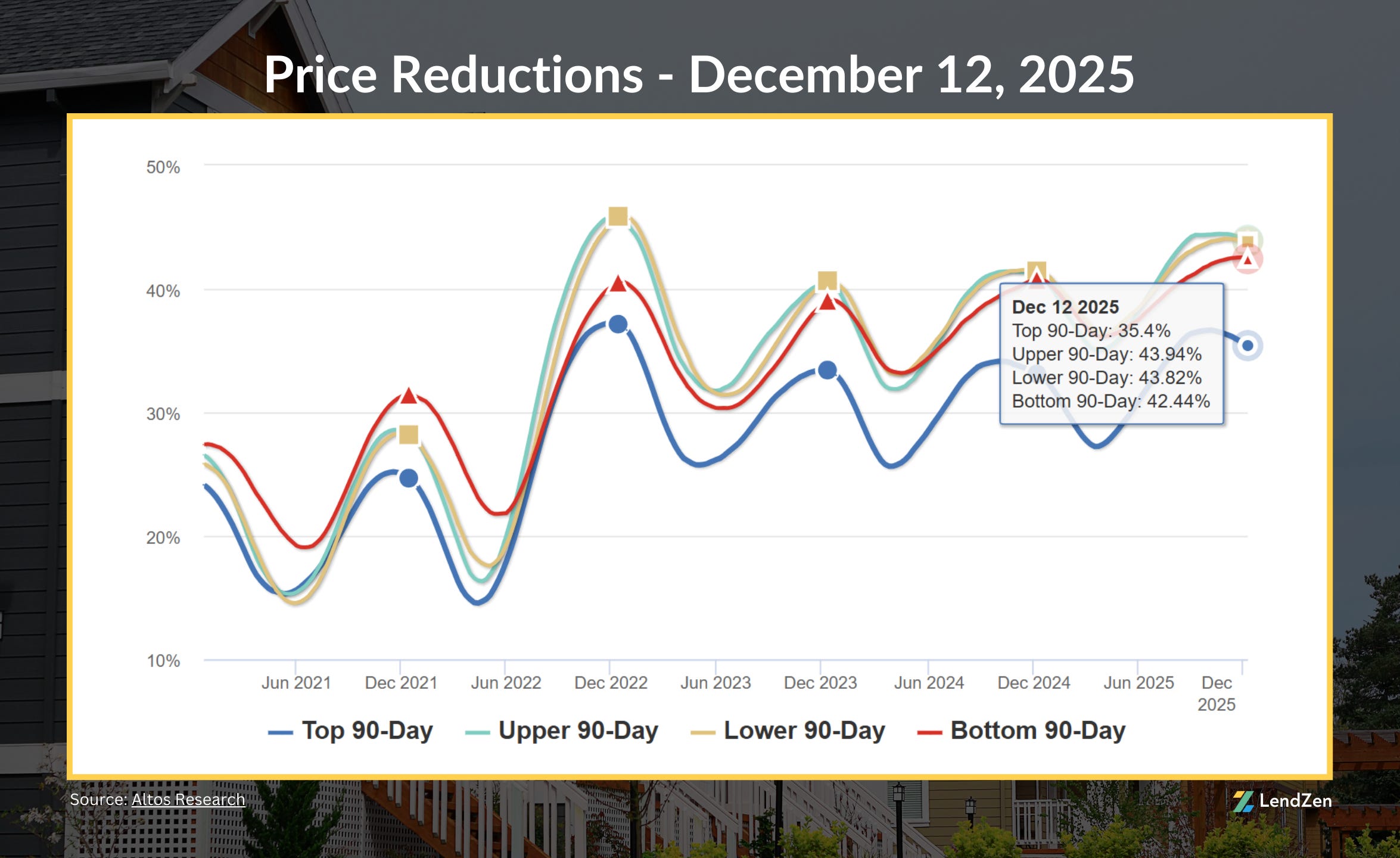

HOUSING DATA 🏠

------------------

Here are the latest housing market stats, with trends from the last 90 days.

The U.S. median list price is $422,150, down two-thirds of a percent (0.67%) from last week.

Price reductions remain steady with a 90-day national average of 40%, with the number of reductions in the higher price tiers declining slightly.

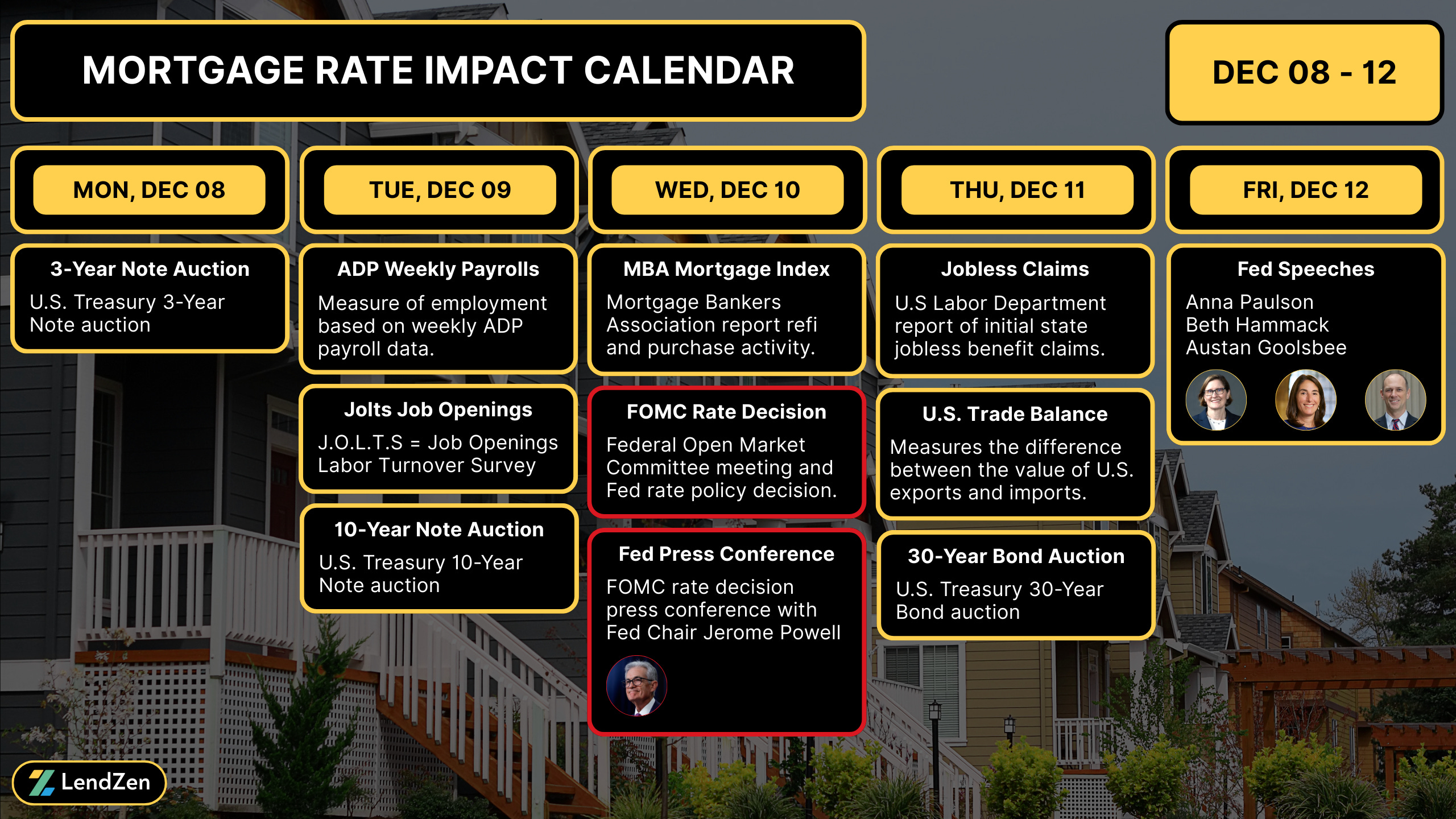

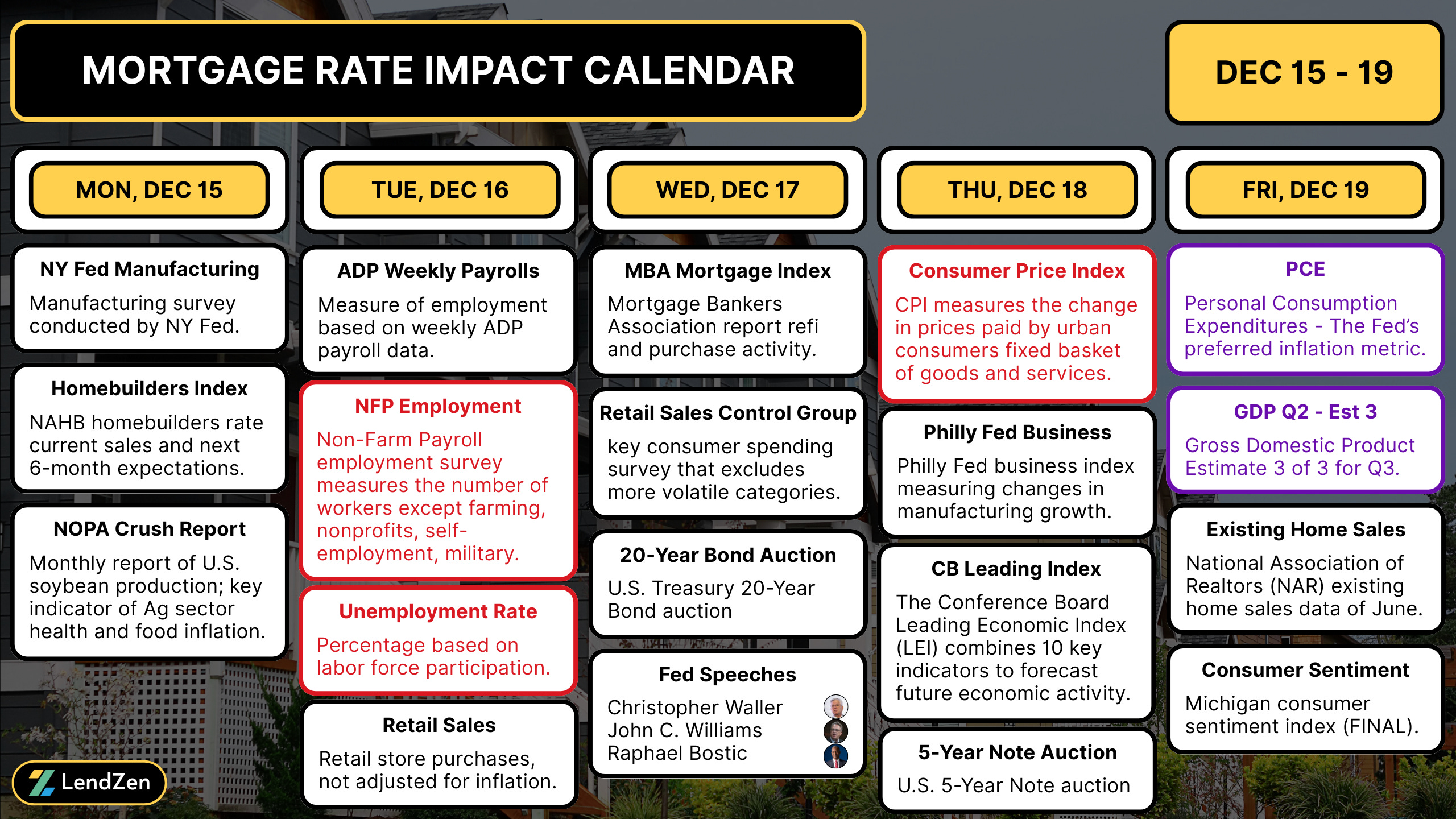

WEEK AHEAD 📅

----------------

The December Non-Farm Payroll report (November data) was originally due last week but was rescheduled to this Tuesday.

NFP is followed by the Consumer Price Index (CPI) on Thursday, creating a double whammy of employment and inflation data in the same week.

Read more in yesterday’s Week Ahead.

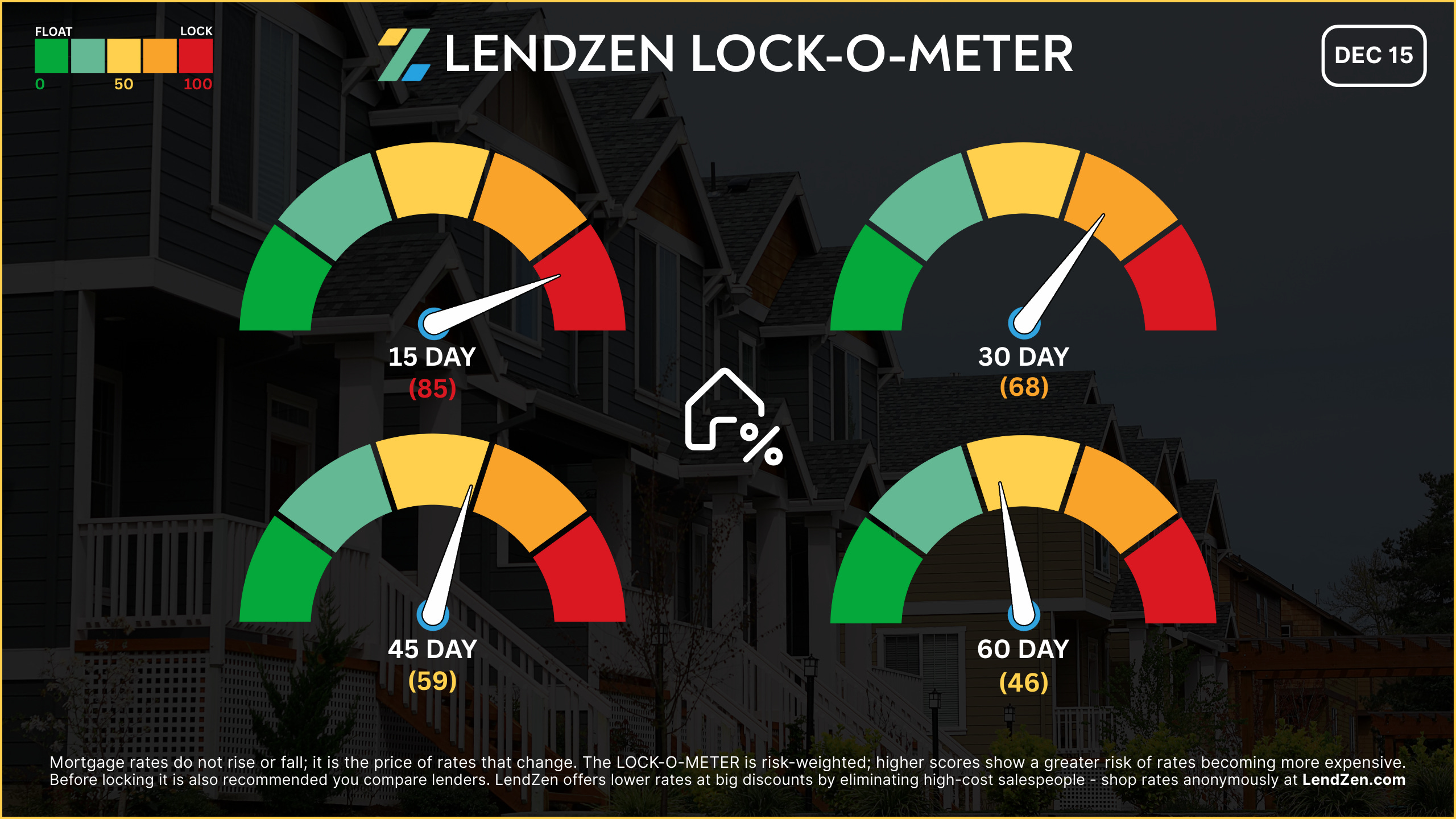

RATE LOCK GUIDE 🔒

---------------------

The LendZen LOCK-O-METER provides borrowers with a risk-weighted score based on how various macroeconomic events, including market data, central bank announcements, and geopolitics, each historically impacts the price of bonds.

higher risk scores = lean towards locking

------------------

Closing Window

------------------

[ 15 Days ] -- 85 🔴

NFP and CPI are packed into the same week, with results that could rapidly reprice rate sheets over a 48-hour window.

[ 30 Days ] -- 68 🟠

With the end of the year looming there is not much that can save you if this week’s data is a death blow to bonds.

[ 45 Days ] -- 59 🟡

If the inflation and labor market pictures remain bond-friendly, we could see a move back toward October lows as we start 2026. It is a wait-and-see situation until this week provides more directional clarity.

[ 60 Days ] -- 46 🟡

Disinflation hopes are persisting despite recent noisy data, and murky forward guidance from the Fed. Revisit the 45-day and 60-day recommendations next week after the current double whammy week is over.

If you are already in a strong position locking generally makes the most sense, especially for shorter windows, since the focus should be on making a savvy rate choice based on your longer-term rate outlook.

I expand on this “long game” approach in this Substack post.

Thanks for reading.

If you want to shop real-time mortgage rates and get instant qualification results without providing any contact information visit LendZen.com

LendZen provides a fully automated mortgage shopping experience that gives you anonymous access to all mortgage rates with full transparency of costs upfront as bond prices change.

LendZen Inc. is an equal opportunity mortgage lender, NMLS 375788.