Military buyers in 4 charts and the tradeoffs of VA loans 🪖🏠📊

Topic Deep Dive

TABLE OF CONTENTS

Introduction

---------------

Recent data from the National Association of Realtors shows military-connected households (active-duty service members or veterans) made up a stable 19% of home buyers in 2025, consistent over the past decade.

Veterans were overwhelmingly repeat buyers, while active-duty service members were more likely to be first-time buyers; due mostly to a skew in age.

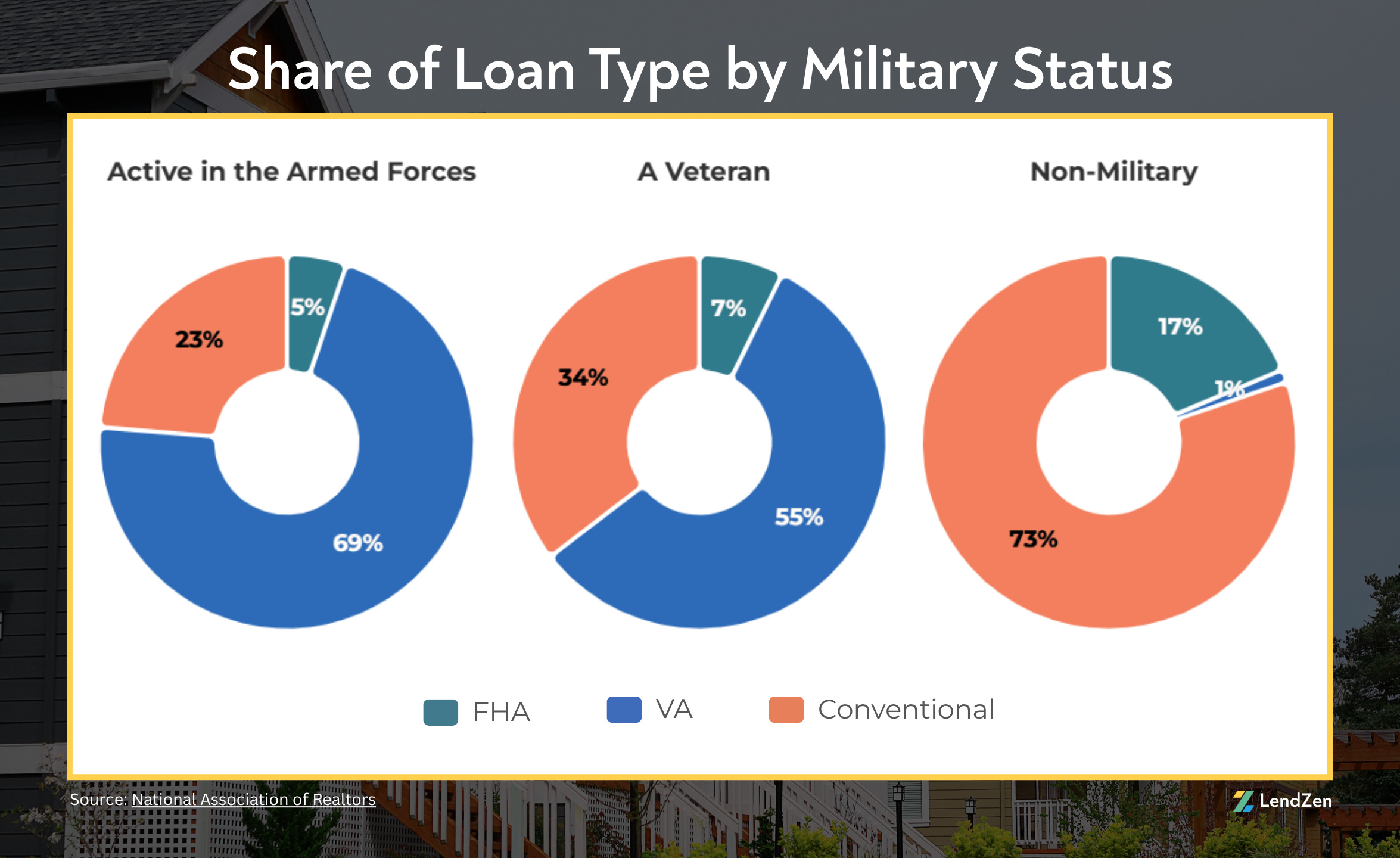

VA loans remain the biggest story, used by 69% of active-duty buyers and 55% of veteran buyers.

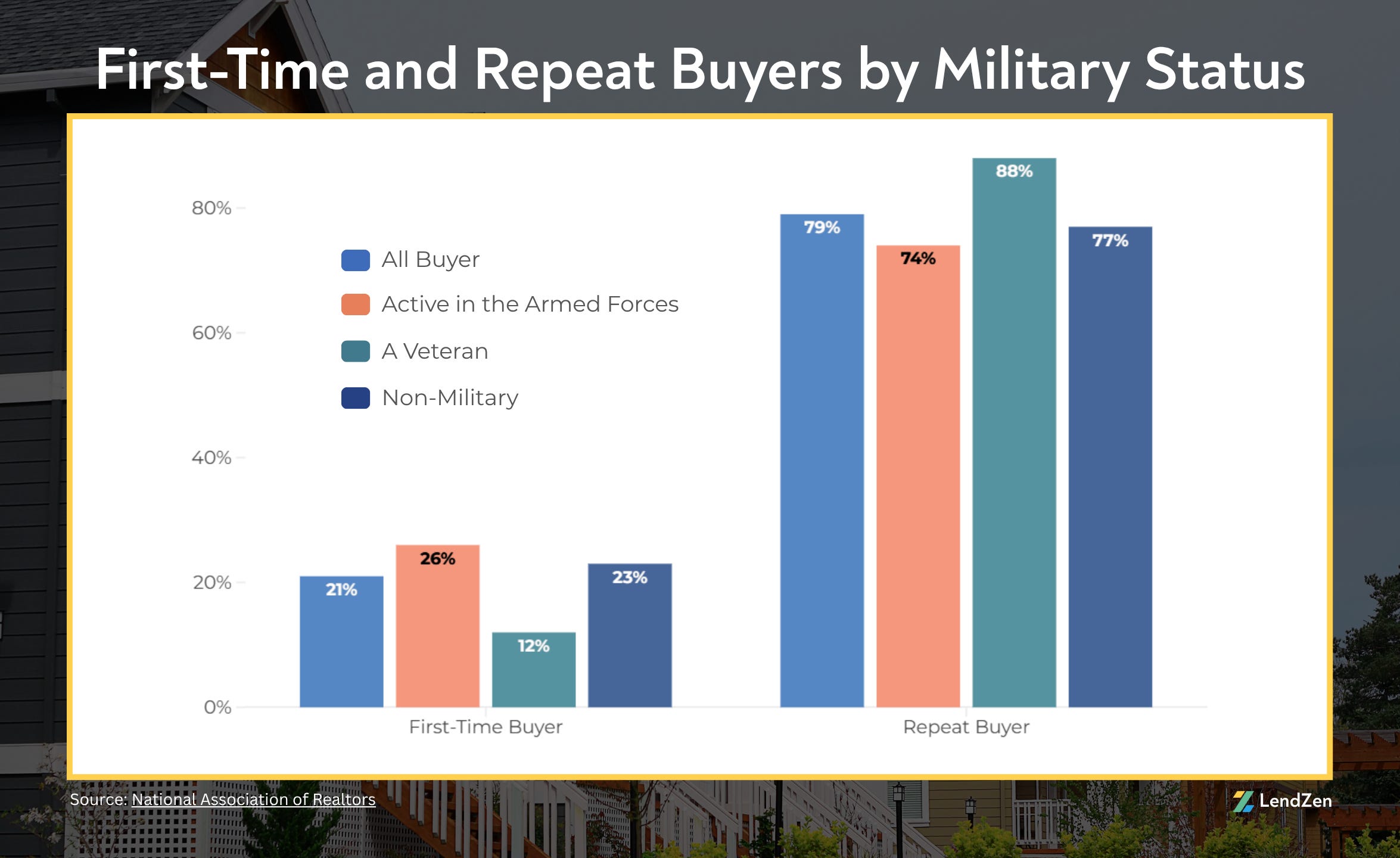

First-time vs. Repeat Buyers

--------------------------------

Active-duty buyers are more likely to be first-time purchasers (26%) than the overall market (21%), while veterans lead the market for repeat buyers (88%).

My takeaway:

The first-time purchaser strength of active-duty buyers is a powerful example of how 100% financing and cost-of-living allowances (COLA) can give military households an edge in a housing market often out of reach for most younger would-be homebuyers who lack the VA loans purchasing power.

In fact, among those who purchased a home in 2025, more than one-third of active-duty service members (36%) and over one-quarter of veteran buyers (28%) financed their home with no down payment.

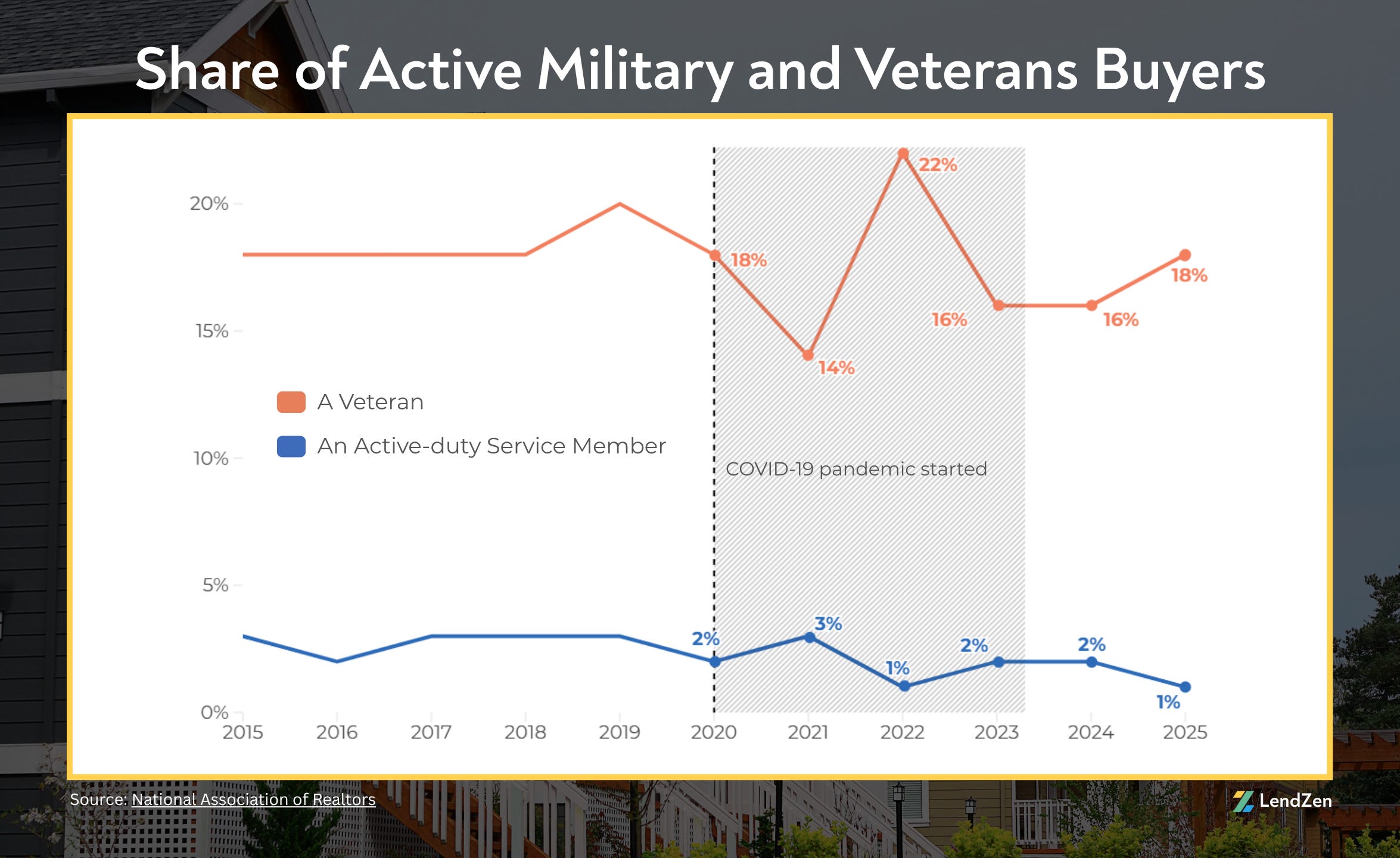

Active-duty vs. Veterans

----------------------------

Active-duty buyers are a small but steady share of the overall buyer population (1-3%), while veterans represent 14-22% of buyers, with recent figures around 18%.

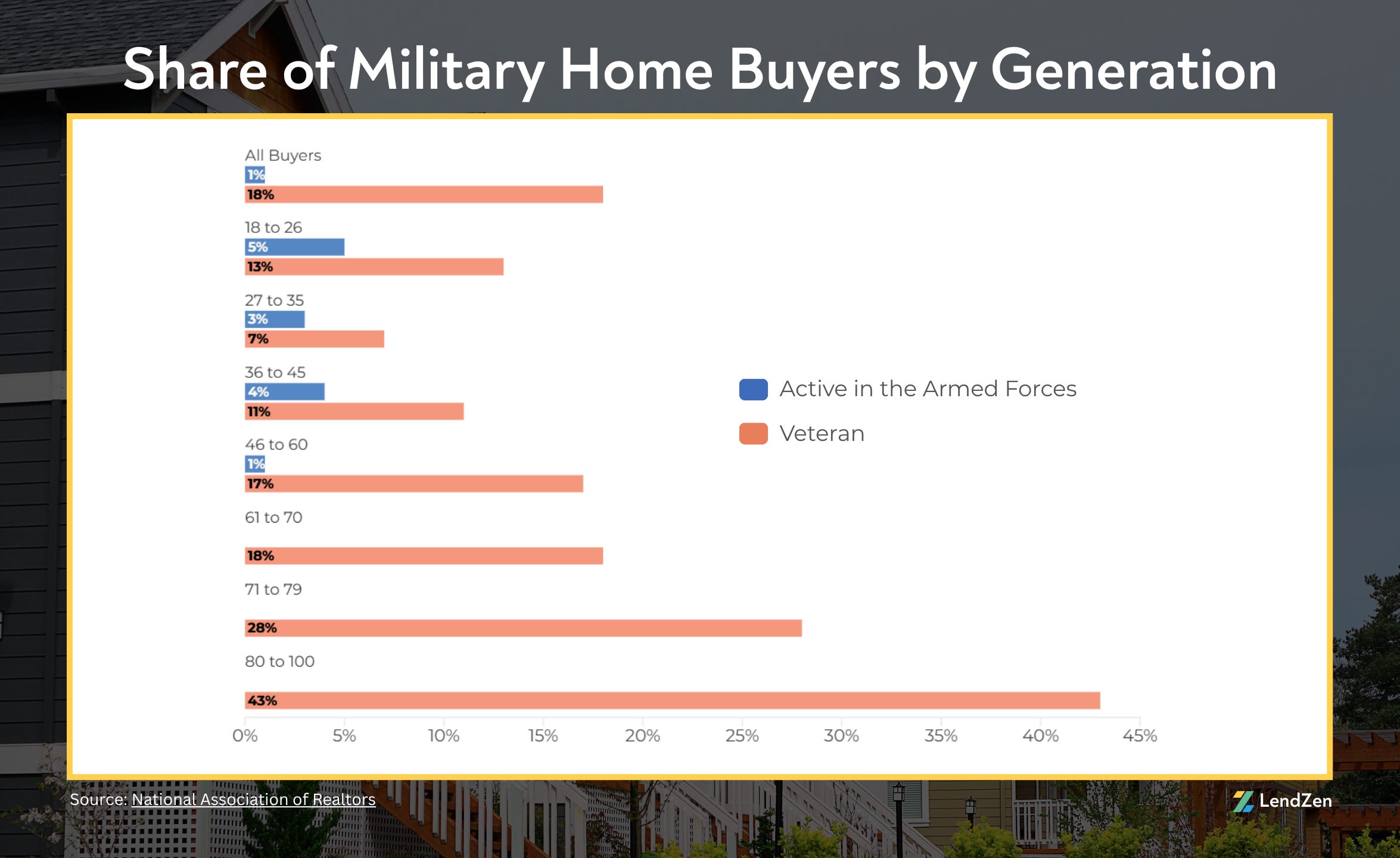

Meanwhile, the Veteran cohort was dominated by older generation buyers (28% for ages 71-79, 43% for 80-100).

My takeaway:

The total number of veterans is much greater than active-duty members, hence why they are a much larger percentage of buyers. However, the consistency of both buyer types overtime shows the key role military households have played in the housing market over the last decade.

Loan Types

-------------

VA loans are leaned on heavily by military buyers; used by 69% of active-duty and 55% of veterans.

My takeaway:

The majority of military buyers using the VA loan is not surprising given zero down options and AUS driven loan approvals that allow much higher DTI ratios compared to conventional loans.

What is surprising though, is how many choose not to use the VA loan.

For military households who have the capacity (down payment) to use other financing options, it can often work out better long-term.

Housing and COLA incentives are a financial advantage many active-duty underutilize, and while the benefits of the VA loan are clear, its shortcomings are often overlooked.

For example…

Absent a service-connected disability, higher LTV loans come with 2.15 – 3.30% upfront mortgage insurance (VA funding fee).

This puts homebuyers who use 100% financing options in a negative equity position immediately after they close (103%).

Active-duty service members relocate (PCS) frequently, and home sellers typically pay agent commissions (4-6%). This puts the military homeowner underwater 9% or more if the home is in a flat or declining market.

Another factor rarely shared with military households, is the servicemember’s loan benefit entitlement used will be permanently tied to the property.

Refinancing from a VA loan to a conventional DOES NOT release entitlement, only the sale of the property does.

The exception is a “single use” restoration of entitlement that must be approved by VA; this can only be used once.

Lastly, leveraging home equity to buy additional properties has limitations with the VA loan.

Unless the service member occupies the property as their primary residence they cannot use the VA cash out loan.

Conventional loans or even non-conforming options (DSCR) aren’t limited by occupancy, giving homebuyers more flexibility if the long-term goal is to build a portfolio of cash flowing assets.

The frequent buying at 100% with 3% funding fees, and selling with another 6% agent fees, strips out most short-term gains and eliminates the long-term accumulation of equity necessary to build lasting wealth.

When considering the smaller percentile of military households in the overall homeownership population, their role in both first-time purchases and repeat purchases cannot be understated, as clearly shown by the data and charts above.

Although the VA loan has very clear advantages it’s not a panacea, and the downsides outlined above should also be considered.

Thanks for reading…

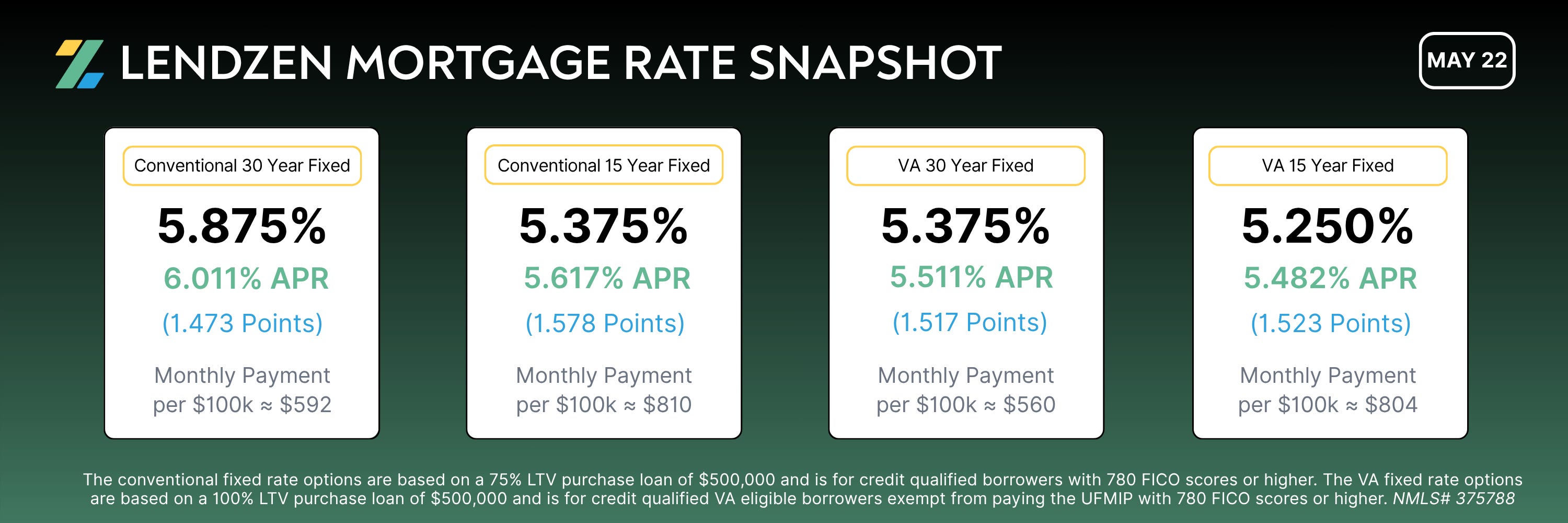

If you want to shop real-time mortgage rates and get instant qualification results without providing any contact information visit LendZen.com

The below snapshot is just a glimpse of today’s rates, but the pricing you see is exactly what you get - there are no additional lender fees or origination charges.

When you customize a rate quote on LendZen you get anonymous access to ALL AVAILABLE RATES that match your specific criteria.

Mortgage rates change daily, but on LendZen.com you can save a scenario and revisit your options anytime with one-click.

You can also request an official Loan Estimate for any loan you create.

Experience hassle-free mortgage shopping now at LendZen.com

LendZen Inc. is an equal opportunity mortgage lender, NMLS 375788